How to Finance a Fixer-Upper

S

Last updated 03/14/2024 by

SuperMoneyMaybe you’ve found your dream home, but it needs some work. Or, there’s a particular neighborhood you want to live in but can only afford homes that need a ton of TLC.

According to the National Association of Home Builders’ Remodeling Market Index (RMI), the demand for home remodels has been at record levels for the past several years and projections call for even more improvement going forward.

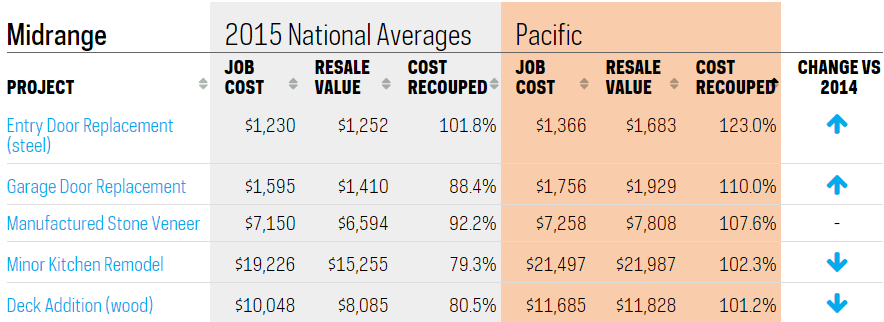

Remodeling your property can be a great investment, if you choose your projects wisely. Here are the top five projects based on the return on investment.

Source: Remodeling Magazine

So, with remodels all the rage, how do you go about financing a fixer-upper? Here is what you need to know about your options for financing, and how to qualify for renovation mortgage.

Get Competing Home Improvement Loan Offers

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

Options for financing a fixer-upper

Be sure to get an unbiased home inspection and detailed list of repair/remodel estimates before looking to finance your fixer-upper. One of the challenges of buying a fixer-upper is finding the cash for the renovations. After making a down payment on a home and paying closing costs, most people don’t have extra funds for renovation projects.

You might be able to finance small projects with credit cards. Another option is a personal loan from a bank or online lender. Either of these choices could work, but they might have higher than average interest rates, and your interest won’t be tax deductible like it is with a mortgage.

The most popular choice for financing a fixer-upper is to use a renovation mortgage, which bundles your home mortgage together with the funds needed to pay for repairs and upgrades.

The basics of a renovation mortgage

Most home buyers need a mortgage to purchase their home. When you buy a fixer-upper, a mortgage company is more critical of your choice because the home might not even meet its minimum standards for a loan.

If you took out a conventional mortgage on your fixer-upper, you’d have to turn around and find additional financing immediately to cover renovations. This could be a second mortgage, personal loan, or another type of financing. Sometimes, the interest rates on these second loans can be high, which makes buying a fixer upper an unwise choice.

Fortunately, there is another option with renovation mortgages through the FHA.

About the FHA 203k loan program

The Federal Housing Administration (FHA) and the U.S. Department of Housing and Urban Development (HUD) have teamed together to make buying and financing fixer-uppers easier with its FHA 203k loan program.

This unique program provides loans through private lenders that combine the primary mortgage on the home with funds for renovations. There is a limit on the amount that you can borrow that is determined by two things.

A certified appraiser must inspect the home and estimate its value after your desired renovations. Your loan is limited to 110% of this final home value. Also, HUD establishes FHA mortgage limits for geographical areas of the country. Your loan can’t exceed that established ceiling.

If your expected renovations are $35,000 or less, a 203k Streamline Loan might be a good option. This is a similar bundled loan that could have either a fixed or adjustable interest rate. Fixed rates remain the same throughout the loan period and adjustable interest rates can go up or down according to market interest rates. The 203k streamline loan isn’t for major remodels or DIY projects, however, and you must live in the property while work is being done.

What you can and can’t do with a 203k loan

A 203k renovation mortgage covers many of the expenses of repairing or upgrading a home. You can replace the roof, HVAC system, plumbing and electrical systems, and even make additions to the home. You can also include painting, kitchen, and bath remodels, and patios in these loans.

A 203k loan also adds in a contingency amount (10-25%) to take care of unforeseen situations. If you plan on living outside the home while renovating, you can even add up to 6 months of mortgage payments to your loan to cover these extra costs. There are some limitations, however.

If there are repairs that improve the energy efficiency or safety of the home, you’ll need to give these upgrades priority over optional items. Energy-efficient or safety upgrades could include asbestos remediation, window replacement, and installing additional insulation.

This type of government-backed renovation mortgage won’t pay for so-called “luxury” improvements to the property. In other words, you can’t add a swimming pool or tennis court in your backyard. You also can’t use a 203k loan to build a commercial space, with some exceptions. You can add commercial space to your home with this loan provided the area doesn’t exceed 25% of a single-story building or 49% of a two-story building.

Qualifying for a renovation mortgage

To qualify for financing a fixer-upper through a 203k your home should either be a detached home (at least one-year-old) or an approved condominium where condo renovations are for the interior only. If you’ve paid cash for your home, you can still apply for a 203k loan if it is within six months of closing.

Eligibility standards are the same as for a regular FHA loan, which means that the minimum credit score is 580 and you need at least 3.5% as a down payment. Also, the lowest amount added for renovations should be $5,000.

For example, if you were buying a home whose purchase price was $200,000 and renovation totaled $40,000, you would need 3.5% of $240,000, or $8,400 as your down payment.

The acceptable debt-to-income ratio will vary by lender; some will take as high as 50% as well as allow cosigners. Debt-to-income ratio is the total amount of your monthly debt divided by your gross monthly income. You can use this debt-to-income ratio calculator to get a better understanding of your financial situation.

Interest rates on a 203k are slightly higher than a conventional mortgage, but the lender is accepting a higher risk in return for lending you money to renovate a home.

How to apply to finance a fixer-upper

If you decide you want a renovation loan to finance your fixer-upper, there are a few additional steps involved in the application process.

You’ll still need to prove your income, employment status, and U.S. citizenship. Beyond that, you also need to show that the home is worthy of fixing up and that the money you’re asking for is justified.

When you apply with an FHA-approved lender, you need to submit a site plan of the home that includes interior drawings. You should include estimates from architects or contractors for the proposed work. An FHA-approved appraisal is done to report on the home’s current condition, including its safety, major systems, and energy-efficiency.

Working with your renovation mortgage

Once your loan is approved with final underwriting sign-off, you can close on your fixer-upper and get to work. There are some stringent requirements on this as well as with a 203k loan.

Your contractor needs to start work on remodeling within 30 days of closing. They must complete all work within 12 months (6 months for a 203k Streamline). There is no such thing as an “FHA-approved contractor.” This means that you can hire anyone you’d like to do the work or do it yourself with a full 203k loan.

An FHA 203k loan gives buyers the ability to purchase a home that is often priced below market value and make needed upgrades for both livability and long-term gains. Interest rates and favorable terms make these loans affordable options for home buyers. Learn more about financing home improvement projects here.

Share this post: