APR vs. APY: What’s the Difference?

Summary:

Annual percentage rate (APR) and annual percentage yield (APY) both sound similar, but they are actually quite different. APR is the annual cost of a loan to a borrower. It is the rate usually advertised when people shop around for a loan or line of credit. APY, on the other hand, is the real rate of return earned on an investment, taking into account the effect of compounding. It is the rate featured when a financial institution wants you to invest your money as a lender or deposit it in an interest-earning deposit account.

Despite the similar names, the annual percentage rate and annual percentage yield have some key differences. Though both APR and APY are involved in interest calculations, APY takes into account the compounding of interest within a year while APR does not. This could make a substantial difference in determining how much money you owe or earn.

In this article, we define what APR and APY mean, how they differ, and how you can calculate each.

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

What is APR?

The initials APR stand for annual percentage rate, which is used when calculating how much interest is paid. The interest rate plus other charges and fees, such as mortgage insurance, closing costs, discount points, and loan origination fees, are expressed as a yearly percentage. The APR calculation assumes there is no compounding within the same year.

The number of periods differs depending on whether the interest is calculated at a daily rate (365) or a monthly rate (12). You could arrive at the periodic rate by dividing the APR by the number of periods.

IMPORTANT! Some lenders can get tricky when providing an APR quote for your loan. This is because the APR advertised on a personal or mortgage loan may not be the same as the interest you actually pay if it doesn’t take into account compounding. The effective APR — the APR you actually pay — is greater the more frequently the lender compounds the interest. To illustrate, a loan with a 22.9% APR that compounds daily will have an effective APR of around 25.7%.

Pro Tip

When comparing mortgage or personal loan offers, look for the lowest APR.

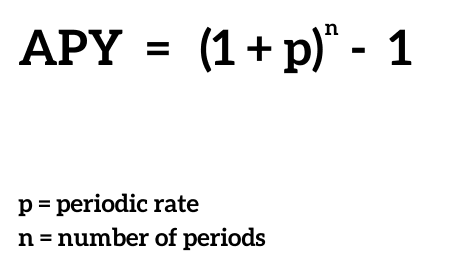

What is APY?

APY stands for annual percentage yield. This rate factors in compounding within a year, which is interest earned on interest. It’s important to learn how often interest earned is added back into the principal because a new calculation is done every time that occurs.

For example, if interest compounds monthly, this calculation repeats 12 times a year. On the other hand, if interest compounds daily, interest is paid on principal plus interest 365 times a year.

Pro Tip

When comparing interest rates on savings accounts, look for a higher APY.

How often does interest compound?

This is an important question, especially for those borrowing money. How often interest compounds depends on your lender, as interest can compound daily, monthly, annually, and even quarterly or semi-annually. For example, most loans (including personal loans and mortgages) compound monthly. However, most credit card issuers compound interest daily.

This frequency changes for those lending money. For instance, a certificate of deposit may compound interest daily, monthly, or semi-annually but a savings account will compound daily. When lending money to a financial institution, read the fine print carefully and make sure you’re getting the return on your investment that you were promised.

Example interest calculation: APR vs. APY

Let’s say you have $10,000 you don’t need for one year. You are considering two places to put your money.

One pays an advertised APR of 5%, mailing you a check for earned interest every month. How much will you get? $500 a year is about $41.67 a month.

The second institution pays an advertised APR of 5% but they compound the interest monthly. The first month you started with $10,000. At the start of the second month, you earn interest on $10,041.67. This continues until the end of the sixth month. At the end of the period, you have about $10,252.62. The APY is approximately 5.12%. Those little differences can add up in your favor.

The table below further demonstrates the long-term effects of APR vs. APY (data from American Express).

| Years Invested | APR (Simple Interest) | APY (Annual Compounding) | APY (Daily Compounding) |

|---|---|---|---|

| End of Year 1 | $10,500.00 | $10,500.00 | $10,512.67 |

| End of Year 2 | $11,000.00 | $11,025.00 | $11,051.63 |

| End of Year 3 | $11,500.00 | $11,576.25 | $11,618.22 |

How does the APR affect borrowers?

As a borrower, lower interest rates are always better. When you borrow money and make monthly payments on your loan or credit card, most lenders ask for a minimum payment. However, this minimum may not cover the full amount of interest added to your balance. Whatever you don’t pay during the previous billing period is included in the calculation for the next period.

Think about it this way. Let’s say you have a personal credit card with an outstanding balance of $500 and an APR of 19%.

Example 1:

At the end of the month, you pay off the balance in full. The credit card issuer hasn’t charged you any interest. So far, so good.

Example 2:

Now imagine you could only pay $50 on your balance. Assuming you don’t add to the balance with any new purchases, your next bill would include not only the remaining $400 balance but also whatever interest was added to your balance. In this case, a 19% APR equates to a monthly rate of 1.58%, which means an additional $7.11 would be added to your balance.

While this doesn’t seem like much now, compounded interest can add up quickly if you only make the minimum payments.

How does the APY affect investors?

As you probably know, compounded interest works in your favor when you’re on the receiving end. Because of this, many financial institutions are quick to promote their APY rather than their APR to anyone looking to lend money (which is essentially what you’re doing when opening a savings account or certificate of deposit). This is because APY takes compounded interest into consideration, whereas APR does not.

When you’re the one lending money, look for the highest APY.

FAQs

Why are APR and APY different?

The annual percentage rate (APR) is the interest rate of a loan plus any fees you’ll have to pay expressed as an annualized rate. APR assumes annual compounding, so it’s not totally accurate if the interest on the loan compounds within the year. APY, on the other hand, does take into account interest compounding within a year (e.g. daily or monthly compounding) and is used to let investors know how much money their money will yield over the year.

Can APY be equal to APR?

APY grows by the number of compounding periods. If the loan were paid off at the end of one compounding period, the APY and APR would be equal.

Why is APY so low?

There isn’t a one-size-fits-all answer to this question. Sometimes APYs are high. However, if you have been looking at the APY of savings or CD accounts, you may wonder why their APYs are so low when the APR on loans by the same bank or credit union are much higher. The business model for banks is to take in deposits, pay a small interest rate, and then loan the money to borrowers. In this scenario, APYs are low because financial institutions make money on the difference or spread between the APY of deposit accounts and the APR of loans.

Why do banks use APR instead of APY?

Typically, APR is used when communicating to borrowers and APY when dealing with investors. However, since the APR of a loan is usually a lower number than its APY, promoting the APR makes the interest rate look more attractive.

Key Takeaways

- The main difference between APR vs. APY is that the APR of a loan doesn’t usually take into account interest compounding within a year. So the APR and the amount of interest you actually pay (aka the effective APR) may be different when interest compounds daily, weekly, or monthly.

- A regular APR assumes annual compounding. So, if a loan compounds annually, its APR and APY will usually be the same.

- APR is used when communicating to borrowers and APY when dealing with investors. However, since the APR of a loan is usually a lower number than its APY, promoting the APR does make the interest rate look more attractive.

- When comparing loans, look for the lowest APR.

- When comparing investments, go with the highest APY. Check to see how often your interest will compound.

Bryce Sanders is president of Perceptive Business Solutions Inc. He provides HNW client acquisition training for the financial services industry. His book, “Captivating the Wealthy Investor” is available on Amazon. Bryce spent twenty years with a major financial services firm as a successful financial advisor. He has been published in 40+ metro market editions of American City Business Journals, Accountingweb, NAIFA’s Advisor Today, The Register, LifeHealthPro, Round the Table, the Financial Times site Financial Advisor IQ and Horsesmouth.com.

Share this post:

AddTable of Contents