Andrew Latham

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

articles from Andrew

287 posts

Good News for Taxpayers: 2026 IRS Tax Brackets and Deductions Bring Lower Bills for Millions

Published 10/10/2025 by Andrew Latham

The IRS has issued its most sweeping tax-law updates in years — even as it furloughs nearly half its workforce amid a federal shutdown.

Who Pays the Property Taxes on HEI Agreements?

Published 10/02/2025 by Andrew Latham

In a home equity investment (HEI) or shared equity agreement, the homeowner—not the investor—is responsible for paying property taxes, insurance, and maintenance. These agreements provide cash without monthly payments, but the homeowner must maintain the home and stay current on tax obligations. Here’s what you need to know.

Why Your Next Workplace Perk Might Be an Emergency Savings Account (and How It Could Boost Your 401k)

Published 10/02/2025 by Andrew Latham

Imagine a job where your employer not only encourages you to save for a rainy day but also gives your retirement fund a little boost at the same time. Sounds like a financial unicorn, right? Well, this new trend is making waves in the workplace benefits world, and it’s more than just a gimmick—though there’s a bit of that too. Let’s dive into how it works and who’s offering it.

The Feds Shut Down. You Should Too. (Here’s How a Personal Budget Freeze Helps You)

Published 10/01/2025 by Andrew Latham

While a government shutdown often signals political dysfunction and economic risk, a personal budget shutdown can have the opposite effect. By temporarily cutting nonessential spending, you can clarify your financial priorities, reduce waste, and reset your budget.

How the New Tax Law Could Cut Your Federal Tax Bill to $0 (Yes, Really)

Published 09/29/2025 by Andrew Latham

Under the new 2025 tax law (Public Law 119‑21), several deductions and credits—such as for tips, overtime, seniors, and an enhanced child tax credit—could theoretically reduce the federal income tax liability of many middle‑income Americans to zero. This article explains what changed, who benefits, and realistic scenarios where a “$0 tax bill” is possible (but not guaranteed).

Home Equity Loans for Debt Consolidation: Pros, Cons, and When It Makes Sense

Published 09/26/2025 by Andrew Latham

A home equity loan can be a powerful way to simplify your debt and lower interest costs by tapping into your home’s value. You’ll get one predictable monthly payment and potentially save thousands over time. However, your home secures the loan, so it’s important to weigh the benefits and risks before moving forward.

The Market Myth That Won’t Die: What the Benner Cycle Really Tells Us

Published 08/26/2025 by Andrew Latham

A mysterious cycle first charted in 1875 claimed to forecast market panics, peaks, and troughs—but don’t be fooled. The Benner Cycle, with its repeating patterns and lunar theories, is more folklore than financial tool. Still, it’s a compelling reminder that markets move in phases, and as a wise investor, you stay calm when others panic—and cautious when others are riding highs.

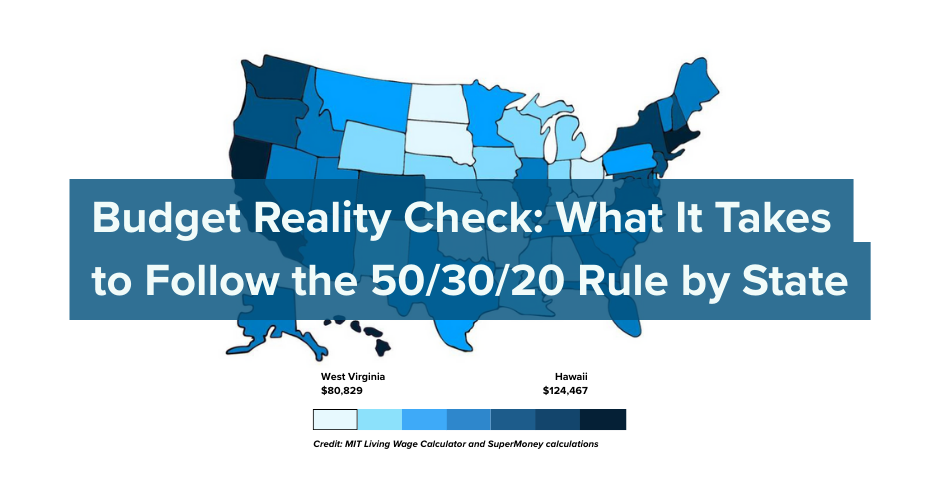

Want to Follow 50/30/20? In Many States, It Takes a Six-Figure Salary

Published 08/24/2025 by Andrew Latham

The 50/30/20 budget rule—50% needs, 30% wants, 20% savings or paying off debt—is a widely used guideline among financial planners. However, based on MIT’s Living Wage Calculator, following this model is aspirational for many households. In fact, in 15 states you need a six-figure income just to follow the rule as a single adult, and families of four with two working parents require at least $186K in every state.

Student Loan Delinquencies Explode to 10.2% as Years of Hidden Missed Payments Hit Credit Scores

Published 08/12/2025 by Andrew Latham

Student-loan delinquencies have surged to 10.2 % of all balances in Q2 2025 as previously unreported missed payments reappear on credit reports following the pandemic reporting pause. This spike is fueling record default risk, crushing credit scores, and threatening economic stability, while borrowers struggle to navigate repayment and default relief.

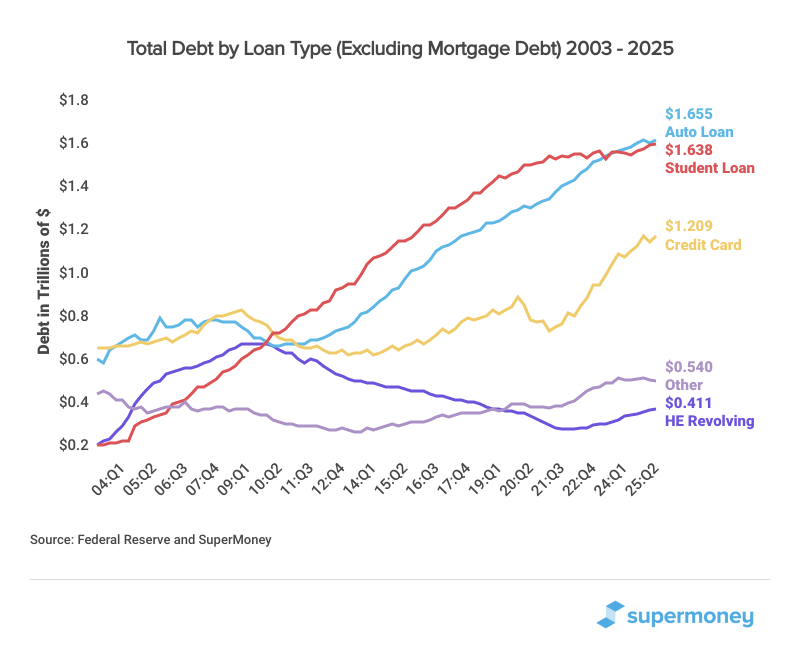

U.S. Household Debt Hits Record $18.39 Trillion – How to Protect Your Finances From Rising Credit Card Balances

Published 08/12/2025 by Andrew Latham

In the second quarter of 2025, Americans’ total household debt climbed by $185 billion, bringing the total to a record $18.39 trillion. Here’s where the biggest increases happened: