SuperMoney’s Auto Loan Offer Engine Will Change the Way You Buy A Car

ML

Last updated 03/14/2024 by

Miron LulicAfter debuting its personal loan offer engine at Finovate in April 2017, SuperMoney unveiled today an automotive focused loan offer engine where its lending partners compete in real-time with customized auto loan offers.

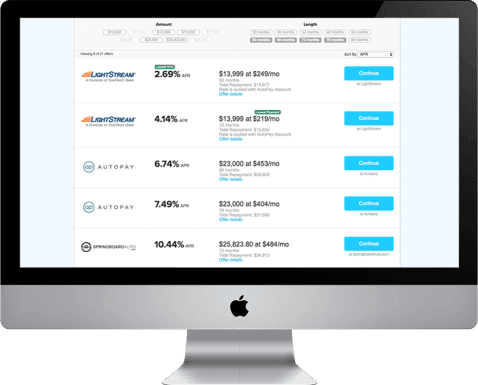

The new auto loan offer engine allows borrowers to submit a single, easy, online application and receive multiple auto loan offers back. The tool makes apples to apples comparisons easy when shopping for the best auto financing rates, fees, and terms.

“The traditional auto financing experience is antiquated – like purchasing an airline ticket 20 years ago,” says SuperMoney CEO Miron Lulic. “These days buying an airline ticket is fast and easy. We’ve brought that same great comparison shopping experience to the auto loan industry.”

The traditional auto financing experience is antiquated – like purchasing an airline ticket 20 years ago.” Miron Lulic, SuperMoney CEO

Whether shopping for an auto purchase financing or existing loan refinancing, SuperMoney’s auto loan offer engine is a no-brainer. Comparing options on SuperMoney won’t hurt the applicant’s credit score because SuperMoney’s lending partners perform a soft credit pull as part of the prequalification process.

Get Competing Auto Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

Only 31.6% of car buyers negotiate the interest rate on their loan

Haggling is mostly a lost art in the United States. However, it’s alive and kicking in the auto industry. Just not when it comes to financing costs.

A recent survey by the Federal Reserve reported that 76.1% of car buyers negotiated the purchase price with the seller, but only 31.6% negotiated the interest rate on their loan. It gets worse. 27.1% of car buyers considered the monthly payment on their auto loan as the most important factor, but only 6.1% considered the interest rate on the loan as the most important factor (source).

However, paying a high interest rate can cost you many times more than what you’re likely to shave off the purchase price of your vehicle, regardless of your negotiating skills.

To illustrate, a $35k auto loan with a 3% APR, will cost you $37,734 over the life of a 60-month loan. The same loan with a 7% APR, will cost you $41,583, that’s a $3,849 difference.

Dealers know most borrowers focus on the wrong things

Car buyers have never had access to so much information. The manufacturer’s suggested retail price (MSRP) is just a google search away. Online tools like Kelly Blue Book, make it just as easy to negotiate the price of used cars. The result? Smaller profit margins for dealerships.

Comparing financing costs is not as easy.

There are two main reasons car buyers overpay in financing costs.

A lack of transparency on available rates and

Not understanding the actual cost of auto financing.

SuperMoney solves both of these problems through its transparent auto loan offer engine.

Dealerships can hide interest hikes behind longer terms precisely because they know most borrowers focus on the monthly payment amount, not the overall cost.

To illustrate, a $35k auto loan with a 5% APR and a 36-month term will have a total cost of $37,763. The same loan with a 72-month term costs $40,584.

Increasing the term of your loan will lower your monthly payments, but it will cost you.

SuperMoney’s auto loan offer engine levels the playing field

Don’t pay more than you need to in financing costs. You can now avoid overpriced auto financing by comparing the rates and terms of leading auto lenders.

Our lending partners only require a soft pull on your credit report, so there is no damage to your credit score.

The tool allows you to compare offers by total cost, monthly payment, APR, and more. You also get a detailed description of hidden fees, such as origination fees and prepayment penalties.

Would you like to know what other buyers think about a given lender before you sign a loan agreement? Click on the lender’s profile and read candid reviews written by other borrowers.

SuperMoney’s auto loan offer engine is free to use and won’t hurt your credit, so there is no downside to checking what rates other lenders are offering. Give it a test drive and let us know what you think.

ML

Miron Lulic is founder and CEO at SuperMoney, a service that helps millions of people transparently compare financial services such as loans, investments, and more.

Share this post: