Business Identity Theft: The Complete Guide

Last updated 04/09/2024 by

Jessica Walrack

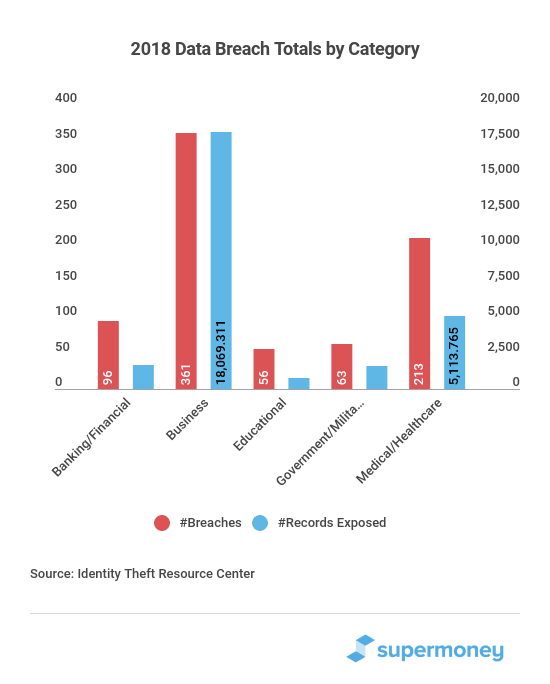

Business identity theft is a significant threat to companies as it can result in staggering losses. In 2018, the number of records exposed rose to 446.5 million (source). The Federal Trade Commission processed 1.4 million fraud reports in 2018, which caused $1.48 billion in losses. Identity theft accounted for a quarter of all reports. According to the latest data from the IRS, 10,000 of business identity theft were logged in 2016 alone, which caused $268 million in damages.

This type of theft is also called commercial or corporate theft, and just like personal identity theft occurs when a thief fraudulently uses a business’s identity. Unfortunately, businesses don’t have the same kind of protection from identity theft that consumers do. Banks often won’t reimburse money lost due to fraud, leaving companies to pick up the tab.

If you want to protect your company’s hard-earned profits, you’ll have to take steps to prevent business identity theft and fraud. Protect yourself from scammers by learning about the common types of business identity theft and how to avoid them.

Compare Credit Report Services

Compare multiple vetted providers. Discover your best option.

Business identity theft definition

Business identity theft occurs when criminals impersonate businesses to exploit them in some way. Thieves use several tactics to accomplish this– from physical address mirroring to illegally changing business registration information. By assuming a company’s identity, thieves can take out loans, rack up credit card debt, and even file fraudulent tax returns. Companies of all sizes from LLCs to corporations are at risk of this type of identity theft– although it often poses the most significant threat to small businesses.

Business identity theft is often confused with information security breaches, which involve the loss or theft of sensitive or personal information belonging to consumers or businesses. Data breaches can sometimes lead to business identity theft, but not always. A data breach doesn’t become a case of business identity theft until a criminal uses the information to impersonate and steal from the company.

Business identity theft is also confused with employee theft, a separate crime in which an employee or former employee steals company assets.

To help you better understand what business identity theft is, here are some examples of the different forms it takes.

Examples of business identity theft

Criminals use many different identity theft schemes to try to assume the identities of businesses. Here are some strategies you should know to protect your business.

Fraudulent business filings or registrations

In most states, it’s easy to change business registration information. Just by paying a filing fee and filling out some paperwork, a criminal may be able to make themselves a director of your company or change your address.

Appearing to be a director of the company could give the criminal access to your company’s bank accounts, loans, and lines of credit. It may also provide them with the authority to open new accounts, make purchases, and illegally sell company assets.

Changing your address gives the criminal control of your mail, so you may not receive notices that would alert you to the fraudulent activity, leaving you totally in the dark.

Cyber-crime and business banking fraud

Criminals may try to gain access to your company’s bank account through phishing scams. Typically, they’ll send you a fake email that appears to be from your financial institution. A link inside the email will send you to a website that prompts you to log into your bank account. If you do, your login information will be compromised.

Hackers can also gain access to your company’s bank accounts and other sensitive financial information by infecting your computer with malware.

Once hackers have your login info, they can use your account to send wire transfers, withdraw money, commit check fraud, and more. Business bank accounts don’t usually come with zero-fraud liability policies, so your bank may not reimburse the stolen money.

Stolen business employer identification numbers (EINs) and tax fraud

Business EINs are similar to Social Security Numbers. They’re required for businesses to open new bank accounts, apply for business loans, file tax returns, and more.

But unfortunately, they aren’t given the same level of protection as Social Security Numbers. You can easily find EINs on business credit reports and look them up in databases.

Because they’re so accessible, scammers often steal EINs and use them to open fraudulent accounts and file bogus tax returns. They often claim to receive an income from your company to get a tax refund. This can get your business in trouble with the IRS and leave you with a big tax bill unless you can prove that fraud has occurred.

Physical address mirroring

In this scam, thieves look for businesses that reside in multi-tenant office buildings. It’s a relatively simple process. Scammers learn enough about the company to open lines of credit or to fool suppliers. Then they lease office space in the same building and start ordering high-value goods. Creditors and suppliers usually miss or ignore the different suite numbers, allowing the scammer to get away with it. By the time a company starts getting calls asking for payment, the fraudsters are long gone with the goods.

Misuse of business owner identities, tech, or services

Business identity thieves often try to gain the personal and business information of company executives and use their authority to commit fraud. They’ll open faulty accounts, make purchases, sell company assets, and more. To make their scam look more legitimate, they’ll often spoof one of the executive’s telephone numbers (using VoIP) when they interact with creditors.

These are just a few of the most common types of business identity theft. There are many more, as criminals continue to create new ways to try and outsmart the latest prevention tactics.

Why should a business be concerned with preventing identity crimes?

Businesses can suffer enormous consequences from identity theft, including income losses and prolonged tax disputes.

Losing income could affect a business owner’s ability to pay employees and vendors. To keep the doors open, they may have to cut costs and lay off employees. However, it may not be enough if they fall behind on loan or vendor payments, damaging their business credit and reputation.

If business identity thieves use your business information to file bogus tax returns, you’ll also get into trouble with the IRS. You’ll have to endure an investigation and prove that the tax returns were fraudulent to avoid a big tax bill. This can be a long and grueling process that takes you away from your business.

Identity theft is even more devastating for small businesses. Fraud can result in huge income losses that small companies can’t afford. This can cause them to shut down, leaving their owners in bad financial shape.

Small companies are a frequent target for identity theft because criminals know they don’t have large security budgets. So it’s even more important for them to take preventative measures against fraud.

How to prevent identity theft in a business

Speaking of preventative measures, here are steps you can take to protect your business from identity theft schemes.

- Shred paperwork containing sensitive data if you have paperwork with information that could compromise your business identity, shred it. However, make sure you use a confetti shredder instead of a strip shredded so criminals can’t piece the paperwork together.

- Regularly order a copy of your business’ commercial credit report.

- Sign up for electronic notifications through your banks and creditors.

- Have a set of procedures to follow if a business credit card is lost or stolen.

- Report any suspicious activity immediately to your bank or creditor.

- Use stronger passwords, scan your computer for viruses, and perform regular software updates that can protect you from cybercrime threats.

- Consider investing in new security solutions like firewalls and antivirus software

- Put systems in place to restrict access to sensitive company information. Only grant access to employees who need it to do their jobs.

These tips can help you keep your business information private and notify you early if your identity is stolen.

What to do if you suspect your business identity has been compromised

If someone steals your business identity, follow these steps:

- Contact the police and file a police report

- Contact all of your banks and credit card issuers as well as anyone else your business may have credit with.

- Speak to the fraud department in credit reporting agencies and place a fraud alert on your accounts.

The sooner you can catch the thief, the better.

Protect your company with identity theft business solutions

Business identity theft is surprisingly easy for scammers to get away with, and can have devastating consequences for businesses. But you don’t have to be a sitting duck.

Credit reporting agencies, including Experian, will monitor your business credit report (for a fee) and notify you in the case of suspected fraudulent activity. This can help you get an early hint of any foul play so you can stop it before it gets too far. Taking steps to prevent business identity theft is essential to keeping your business alive and running smoothly. Don’t wait until it’s too late!

Jessica Walrack is a personal finance writer at SuperMoney, The Simple Dollar, Interest.com, Commonbond, Bankrate, NextAdvisor, Guardian, Personalloans.org and many others. She specializes in taking personal finance topics like loans, credit cards, and budgeting, and making them accessible and fun.

Share this post:

AddTable of Contents