How to Calculate Marginal Cost: Formula and Examples

Summary:

The marginal cost of production describes how much more it costs to produce additional units of goods or services. You can calculate marginal cost by dividing the change in production costs by the change in quantity produced. Among other things, this can help companies to optimize their production levels. A business can usually reach its optimum production level if its marginal costs equal its marginal revenue.

Let’s be honest, keeping track of a business requires a bit of math. On the upside, it’s pretty simple math, and it’s important to help a company decide how to optimize overall operations through more efficient production.

For the purposes of this article, we’ll focus on examples of marginal costs of production in relation to manufacturing. However, the concept is easily applied to other businesses as well, such as those that provide services rather than tangible products. First, let’s explore the concept of economies of scale and how that relates to marginal costs.

Economies of scale

Economies of scale is an economic theory that explains the cost advantages companies can achieve by increasing the production of goods and also lowering costs. Ideally, if you produce more units, you can spread out the total costs of production (fixed costs plus variable costs). This results in fewer manufacturing expenses per product.

For example, a business can often get a better price when they buy more raw materials, which reduces the overall cost of each piece.

Diseconomies of scale

The flip side of this concept is when a firm’s cost per unit increases as it produces more pieces. This is known as diseconomies of scale.

For example, this might happen if a factory reached its maximum production capacity and, in order to produce even one additional unit, they would require a new machine or even a whole new facility. In that case, it would be prohibitively expensive to make more products without incurring production costs that would seriously inhibit profits.

Understanding marginal cost of production can help businesses expand production, reduce per unit production cost, and achieve economies of scale.

What is the marginal cost of production?

As noted, marginal cost refers to the costs a business incurs while more units are produced. More specifically, a company needs to know how costs are impacted by the production of one additional unit. For example, you may need to figure out the total cost to produce one more raincoat on top of the 10,000 that a firm already manufactured.

Variable and fixed costs

To understand marginal costs, you also need to have a grasp on your total production costs, which include both variable and fixed costs.

- Variable. Variable expenses include things like labor and raw materials, which can fluctuate depending on a number of factors. However, these expenses usually increase or decrease along with the number of goods produced or sold.

- Fixed. Fixed expenses do not change based on a business’s volume of output and tend to stay the same over time. Examples of an average fixed cost usually involve overhead like rent, taxes, insurance, utilities, and certain salaries of employees not directly involved in production. For instance, a firm’s accountant’s salary would be a fixed cost because it stays the same regardless of whether 100 or 1,000 units are being produced.

If your business doesn’t have a good handle on both its fixed and variable costs it’s impossible to figure out the marginal costs incurred by increasing production volume.

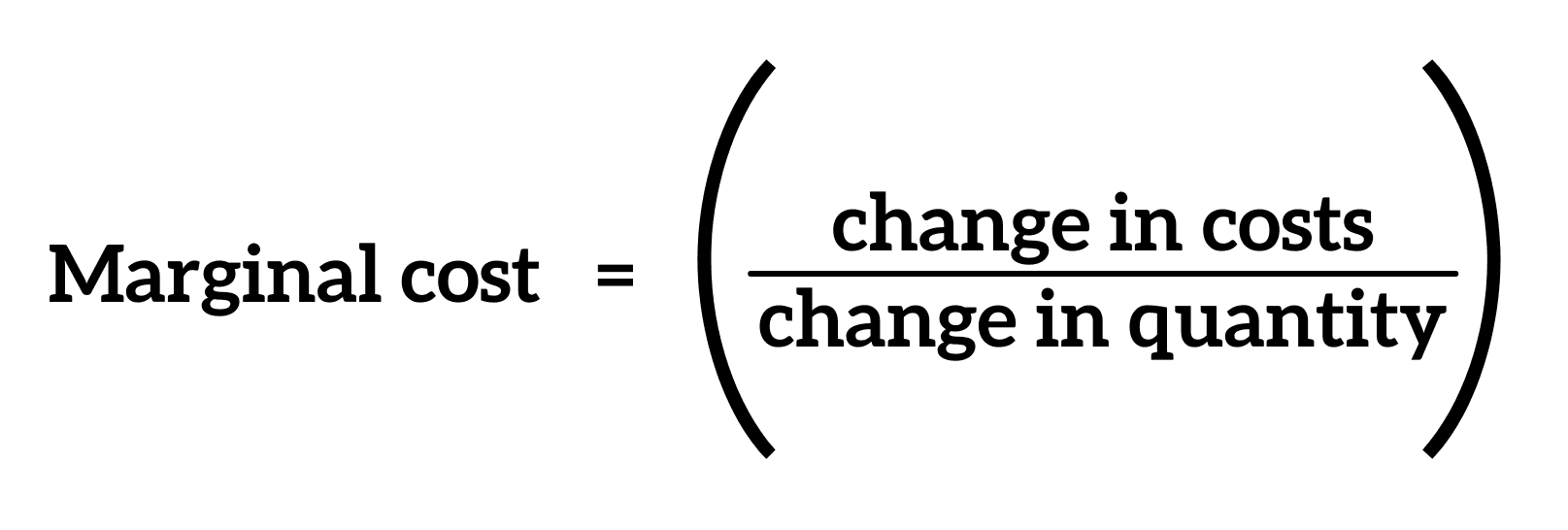

How to calculate marginal cost

When you’re calculating the marginal cost of production, you need to use the marginal cost formula. It’s a simple equation that involves dividing the change in costs by the change in quantity.

To further understand the marginal cost equation, however, let’s first take a closer look at exactly what we mean by a change in costs and a change in quantity.

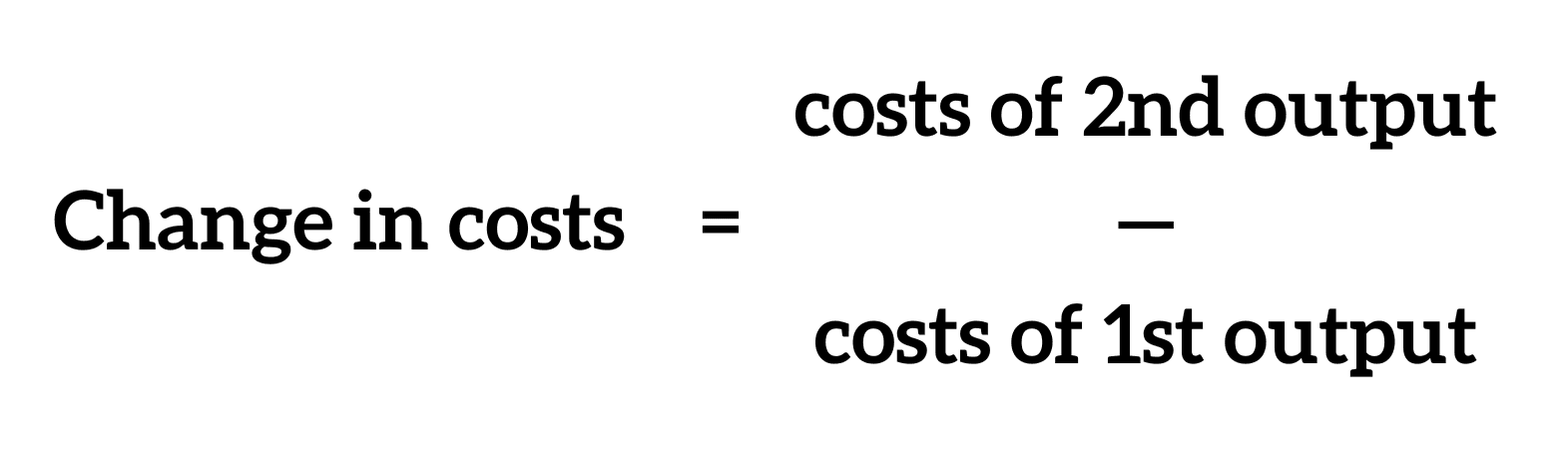

Change in costs

As you make adjustments to the number of units produced — whether you increase or decrease the supply — the cost of production will naturally change as well. As mentioned, variable costs change, so you may be increasing or decreasing spending on labor or materials as you have more or less volume of product.

For example, if you need to hire an extra employee to increase production, that will change your costs to produce additional units. To calculate the change in costs (used in the marginal cost formula) you need to subtract the total production costs of the initial output from the costs needed to produce the second output.

For simplicity’s sake, let’s say the average variable cost is $200 and the average fixed cost is $800 for the first production run, for a total cost of production of $1,000. So, if you produced 100 raincoats in the first production run at a total cost of $1,000, and the second batch of 200 jackets had a total cost of $2,000, your change in cost is $1,000.

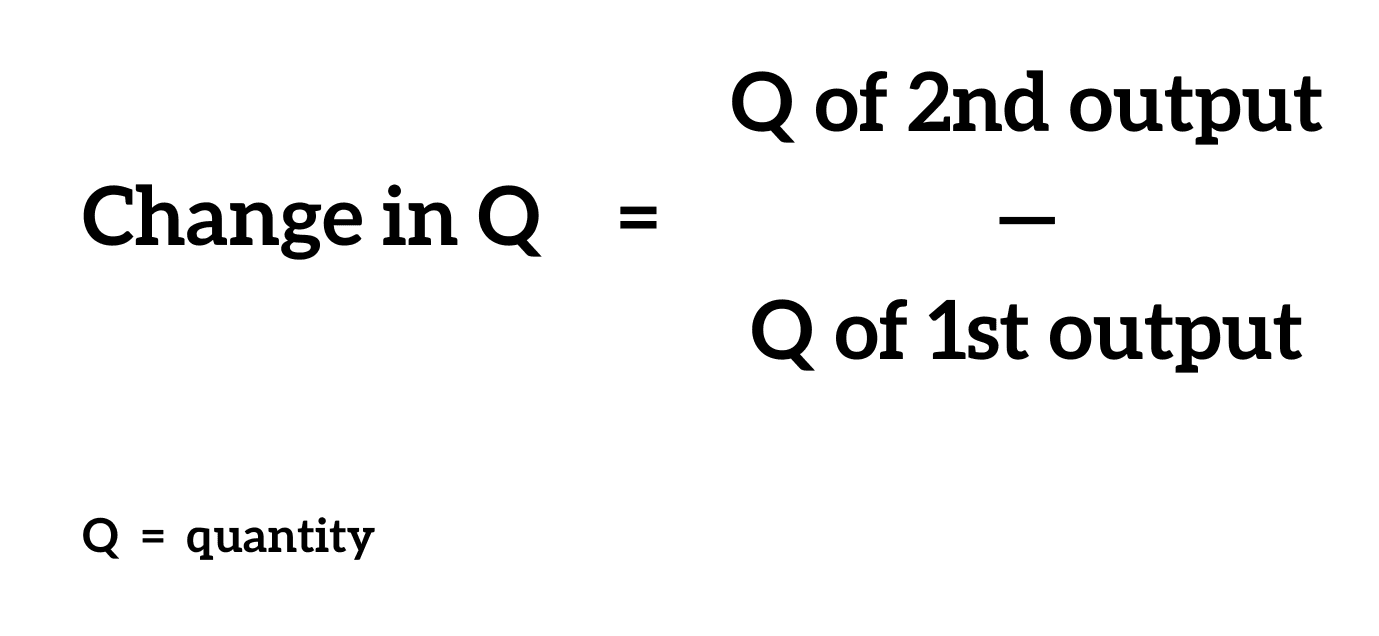

Change in quantity

The number of units produced will naturally increase or decrease at different points during the production process. These differences should be significant enough to then evaluate changes in cost.

To calculate the change in quantity is simple: Take the total amount of units from the first batch produced and subtract it from the next batch.

Following from above, you would deduct 100 units of the first batch from the 200 units from the second batch, which leaves you with a change in the quantity of 100 units.

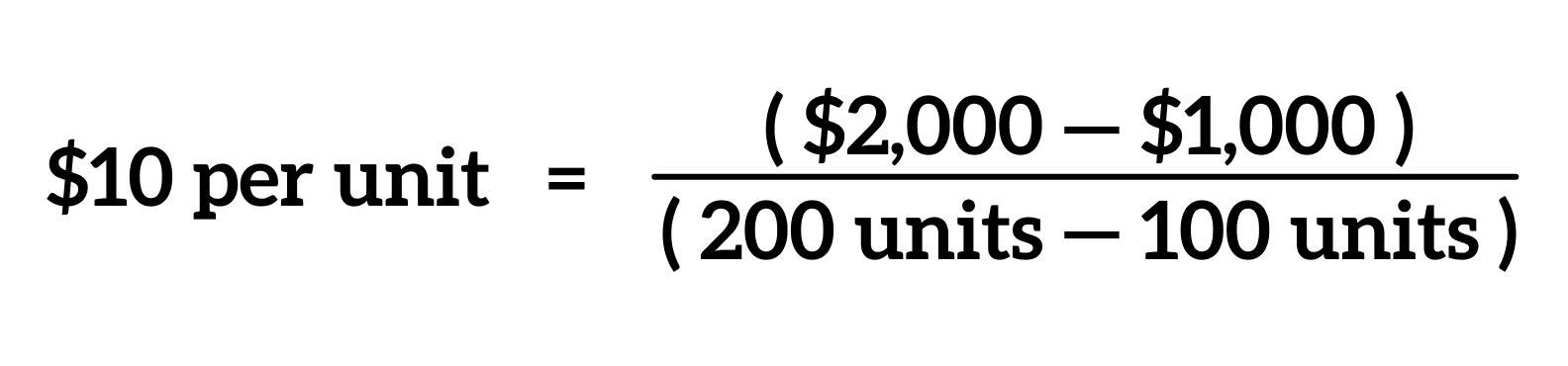

Calculating marginal cost

This takes us back to the marginal cost formula, which says we need to divide the change in costs by the change in quantity. Now our formula will look like this as we fill it in:

This tells us that your marginal cost per additional unit is $10. You can then use this information to decide whether producing additional units is smart for your individual business. If you think increasing production will increase your total revenue but don’t currently have the capital to do so, you may want to consider a business loan.

Importance of marginal cost equation in production

It’s critical for a company to know how to calculate marginal cost so it can decide at what point making more units is no longer profitable. To follow our earlier example, if the price at which a raincoat is being sold (say $20) is more than the marginal cost, which is $10, you’re in good shape. At this point, it’s wise to determine whether producing more raincoats will continue profiting your business or jeopardize it.

On the other hand, if the raincoat only sells for $5, which is less than the marginal cost of $10, you probably don’t want to continue production. Or, alternatively, you might need to raise the price tag per unit if you want to increase your production volume and still remain profitable despite the additional costs.

Other benefits of calculating marginal cost

- Helps to pinpoint when costs of raw materials decrease due to bulk ordering.

- Can help identify areas in which to reduce the overall cost of production.

- Can help a business figure out an ideal production volume at which the overall cost of making a single unit of product is reduced.

- Indicates to a company when it should increase production, decrease production, or when it may need to raise its prices because of losses incurred.

It’s important to keep in mind that if the marginal revenue is higher than the marginal cost, it’s best to increase production. On the other hand, if the marginal cost is higher, you should decrease production.

Therefore, to have the highest profit, a company should aim for the marginal cost to equal the marginal revenue.

Key Takeaways

- Marginal cost represents the incremental costs incurred by making one more unit of product.

- The marginal cost formula is calculated by dividing the change in costs by the change in quantity.

- By figuring out how to calculate marginal cost of production, businesses can figure out how to optimize their volume of production.

- Calculating marginal cost can ultimately help a company to achieve economies of scale in their overall production costs.

- The ideal for optimum production level is for marginal revenue to equal marginal cost.

Share this post:

Table of Contents