Debt Stress Is Rising: Americans Expect Missed Payments at Decade Highs

Last updated 01/08/2026 by

Andrew Latham

Summary:

Americans are increasingly worried about their ability to keep up with debt payments. New data from the New York Fed shows that expectations of missing minimum payments are near the high end of the past decade, outside of pandemic spikes. Research from the Federal Reserve, CFPB, and academic economists suggests that financial uncertainty increases the risk of missed payments—while greater clarity and budgeting can help reduce stress and delinquency risk.

More Americans are bracing for trouble paying their bills. According to the New York Fed’s Survey of Consumer Expectations, households now expect a higher risk of missing debt payments than at almost any point over the past decade, outside of the extraordinary disruption caused by the pandemic.

This data doesn’t measure missed payments themselves. Instead, it captures something that often comes first: rising financial stress and uncertainty.

End Your Credit Card Debt Problems

Get a free consultation from a leading credit card debt expert.

It's quick, easy and won’t cost you anything.

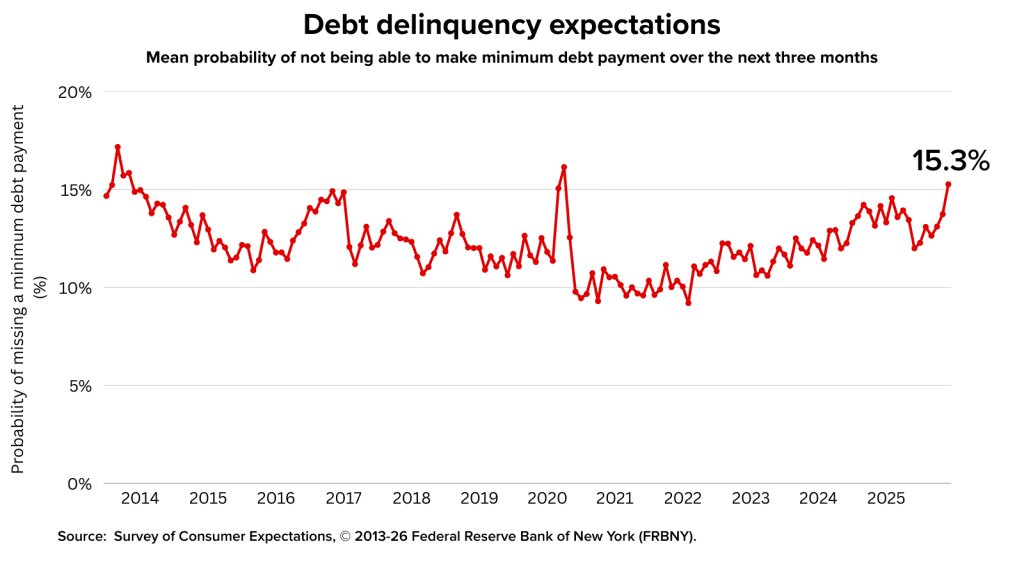

Debt delinquency expectations are near decade highs

In December 2025, consumers reported an average 15.3% probability of being unable to make a minimum debt payment over the next three months, according to the New York Fed. Outside of pandemic-era spikes, that figure sits near the upper end of readings going back more than ten years.

Historically, increases in delinquency expectations have often preceded rises in actual missed payments. When households anticipate difficulty, it typically reflects tighter budgets, higher balances, and limited financial flexibility—conditions that tend to show up in credit data with a lag.

In short, consumers are signaling stress before it becomes visible on credit reports.

Rising expectations mirror broader financial strain

The rise in delinquency expectations aligns with other indicators of household pressure. According to PNC Bank, 67% of U.S. workers now live paycheck to paycheck, leaving little room to absorb unexpected expenses or higher interest costs. At the same time, credit data shows that subprime borrowing has returned to pre-pandemic levels, while more than one in four Americans now fall into the non-prime category.

Together, these trends suggest that while credit conditions have normalized since the pandemic, financial stress has not eased. Instead, many households appear to be operating closer to the edge.

Why expectations and uncertainty matter for payment behavior

Behavioral economics research shows that financial uncertainty plays a measurable role in outcomes. Studies from the National Bureau of Economic Research find that when financial information is less salient—or when consumers feel uncertain about their situation—they are more likely to delay decisions, disengage from planning, and underreact to growing balances, even when income and debt levels remain unchanged.

Research summarized by the Consumer Financial Protection Bureau similarly shows that consumers reporting lower financial well-being and higher stress are significantly more likely to miss payments and struggle with day-to-day money management. Stress and uncertainty don’t just reflect financial problems; they can actively make them worse by reducing follow-through.

At the same time, evidence suggests the opposite is also true: increasing clarity can improve behavior.

How clarity and budgeting can reduce delinquency risk

A well-known Federal Reserve Bank of Boston field experiment found that simple reminders and increased attention to debt obligations led low-score consumers to reduce balances and improve payment behavior, resulting in average credit score increases of more than 20 points. Notably, these improvements occurred without new credit, refinancing, or financial education.

Other Federal Reserve research shows that consumers who actively monitor balances and upcoming bills tend to carry lower revolving debt and incur fewer fees. The common thread across these studies is not higher income, but greater visibility and reduced uncertainty.

Budgeting works in a similar way. By helping households see where money is going and what obligations are ahead, budgets reduce surprises and allow consumers to adjust earlier—before a missed payment occurs. While budgeting can’t eliminate financial hardship, it can reduce the likelihood that stress turns into delinquency.

What the data is signaling now

The New York Fed’s delinquency expectations data suggests that many Americans feel less confident about their ability to keep up with debt payments in the months ahead. That concern is rising even before widespread increases in actual delinquencies appear in credit reports.

As financial pressure builds, preparation and clarity matter more. Tools that help households understand their financial position, plan for upcoming bills, and reduce uncertainty—such as budgeting and spending-tracking tools—can play an important role in preventing small setbacks from becoming lasting credit damage.

A practical next step for households under pressure

With more than one in four Americans now classified as non-prime and 67% of U.S. workers living paycheck to paycheck, many households have little room for mistakes. In that environment, staying current often comes down to visibility and consistency—knowing what bills are coming, where money is going, and how much flexibility remains before problems arise.

Tools designed around these behaviors can help reduce stress and prevent small issues from turning into lasting credit damage. SuperMoney’s app is built to help users track spending, plan ahead for bills, and stay organized, supporting the everyday habits that research shows are most closely tied to staying current and protecting credit.

Key takeaways

- Debt delinquency expectations are near decade highs outside pandemic spikes.

- In December 2025, consumers reported a 15.3% average chance of missing a minimum payment.

- Rising expectations often signal financial stress before delinquencies appear.

- Research shows that clarity, reminders, and budgeting can reduce delinquency risk.

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

Share this post:

Table of Contents