What is a 5/1 ARM? Pros and Cons Explained

Last updated 05/18/2026 by

Ossiana Tepfenhart

Summary:

A 5/1 ARM is a loan that starts with a low fixed rate, then converts to an adjustable-rate mortgage after five years. Your home loan will change rates every year, based on the current mortgage rate prices on the market. While this could be a great deal for house flippers, long-term homeowners may want to look for alternative options.

Even though mortgages are common in today’s markets, the specifics are still fuzzy to most people. Fixed-rate mortgages are easy enough, but hybrid and adjustable-rate mortgages (ARMs) are a whole other ballgame. ARMs and hybrids can be great options for some homeowners, while others may be in for an unwelcome surprise.

While ARMs aren’t for everyone, they can be a great option for the right borrower. Today, we’ll break down a 5/1 adjustable-rate mortgage, what it is, what the “5/1” means, and why it could make sense for you.

What is a 5/1 hybrid adjustable-rate mortgage?

A 5/1 ARM is an adjustable-rate mortgage that has a fixed rate for the first five years. After these five years, the rate adjusts according to the current market rates. It will then re-adjust annually for the duration of your loan’s term.

A 5/1 hybrid adjustable-rate mortgage is the same thing as a 5/1 ARM.

Compare Home Loans

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

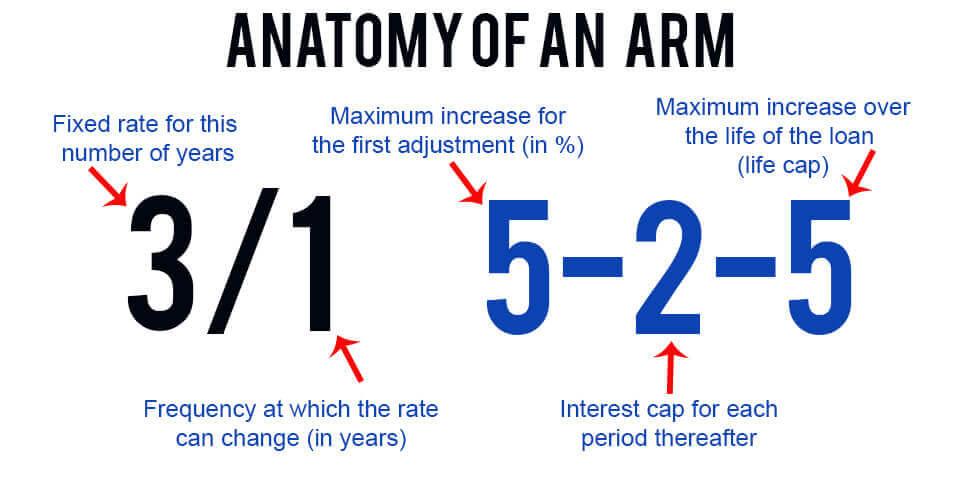

What do the numbers in “5/1 ARM” mean?

You’ll see two numbers accompanying every hybrid adjustable-rate mortgage. It may look a little funny, but these numbers offer valuable insights into your loan terms.

- The first number (the five) identifies how long you have a predetermined fixed rate. This is often called the “teaser rate,” and is typically low. In this case, the “5” means you’ll have a teaser rate for the first five years of the loan.

- The second number explains how frequently the mortgage interest rate adjusts after the initial period. This is when the “adjustable” portion of the mortgage loan term kicks in. Here, we have a “1,” which means that your interest rate will change annually after your fixed interest rate period ends.

Why are 5/1 ARMs referred to as hybrids?

“Hybrid” refers to the combination of interest rates. The first five years act like a traditional fixed-rate loan, complete with a steady monthly payment. From the sixth year forward, however, a 5/1 ARM acts like an adjustable-rate loan instead.

What do I do if interest rates increase dramatically?

Unfortunately, this is the “unwelcome surprise” homebuyers may experience, and it all depends on what you have in your contract. A high interest rate cap (which we discuss below) may cause some panic, but the market may result in a much lower interest rate the following year.

If your ARM doesn’t have a good cap system, then your monthly budget might be tighter than usual. In some rare cases, you might be able to work around loan terms to help make things more affordable. You might also want to get a new loan.

If looking for an ARM already sounds too complicated, don’t worry! At SuperMoney, we do the research for you. Check below to review and compare adjustable-rate mortgages from some of the industry’s top lenders and find your perfect loan.

What should I look for in a 5/1 ARM?

Not all ARMs are the same, even if the ones you’re browsing all have the same “5/1” tag instead of a “7/1” or “10/1” tag. Several factors can impact your finances and offer major interest savings.

Let’s assume for this example, and those following, that you have a 5/1 ARM loan with an introductory interest rate of 2.5% and a 2/2/5 cap (this will make sense in a minute):

Initial cap

The initial cap is the highest amount that a mortgage’s interest rate can rise after the introductory rate expires. In the example cap above, 2/2/5, the initial cap would be the first “2.” This means that after the introductory period ends, your adjusted interest rate can’t exceed 4.5% in the first year.

Depending on what your mortgage lender calculates, this rate may be lower than 4.5%. However, this cap ensures that your rate won’t increase past this number for one year.

Subsequent adjustments caps

Next in the cap offer is your subsequent adjustment cap. This is the second “2” in the example. This means that for every year remaining in your mortgage, your interest rate cannot increase by more than 2% each year.

In this example, your maximum interest rate is already at 6.5%. That doesn’t sound great. However, the good news is ARMs have maximum caps.

Maximum cap

The maximum cap, also known as the “lifetime cap,” is the last number in the three-number cap format. The lifetime cap is the maximum number of percentage points that your interest rate can increase over the entire duration of the loan.

In our example, the maximum cap is “5,” meaning your interest rate cannot exceed 7.5% for the entire loan’s duration. While this is a nice fallback to have, a 7.5% interest rate is incredibly high for mortgages.

This doesn’t mean every mortgage payment will have a 7.5% interest rate. Your rate will fluctuate depending on the market.

Review all terms in a 5/1 ARM

Though caps are one of the most important loan terms to review, several others influence a mortgage’s rate and overall price.

- Minimum Down Payment. Some ARMs will have a lower down payment than others. Be careful, though! Lower down payments often come with higher mortgage rates and monthly payments.

- Introductory Rate. This is your starting interest rate. Using this number, you can estimate what your highest mortgage payment will be throughout the loan’s term.

- Requirements. Like with other mortgage loans, this is still an application process. To get the best rates, you need a good debt-to-income ratio, a decent credit score, and a sizeable down payment to make this loan’s requirements.

Regardless of what loan you get, we always recommend reading up on the loan requirements.

5/1 ARM Example

To better understand how these loans work, let’s look at another example. We’ll use the same example as before (a 5/1 ARM with an introductory rate of 2.5% and a 2/2/5 cap). Let’s say your loan is for $300,000:

You make monthly payments of $948 for five years, which excludes any insurance or tax payments. After the five years are up, your loan rate adjusts. Your lender calculates your new interest rate to be 3.6% based on market studies. Now you’re making monthly payments of $1,091. Okay, not terrible.

The next year, your rate increases again to 5.6%, which brings your monthly payment to $1,377. At its highest, your monthly payment works out to $1,678 under your 5/1 ARM. Yikes.

This doesn’t mean interest rates won’t come down, in which case you’d make a lower monthly mortgage payment. It’s also important to remember that the longer you pay things off, the more of your payment goes to the mortgage principal. This can help speed up your payments.

Let’s compare these numbers to those from a 30-year fixed-rate loan using the same loan amount and an interest rate of 4%. Without insurance and taxes, your monthly payment would come out to $1,145. For the first five years of your 5/1 ARM, you’d save $2,364 per year on your monthly payments.

However, that all changes when your introductory period expires. The first year of the adjustable-rate mortgage costs $2,784 more than the fixed-rate loan for the year.

Pro Tip

Get an ARM without prepayment penalties, and you can use any money you save to make your bills shrink faster.

What are the pros and cons of 5/1 ARM?

Depending on your financial goals, a 5/1 ARM could be the perfect loan for you. However, before making any rash decisions, consider these pros and cons first.

When considering these points, remember that any money you put towards your mortgage principal will help shrink your loan. In some cases, it could lead to a loan curtailment. This is especially true for 10-year ARMs.

If you do not pay money towards the principal in advance, you will probably have higher than average interest payments.

5/1 hybrid ARM vs. Fixed-rate mortgage

Let’s take a closer look at the differences between adjustable- and fixed-rate mortgages.

| 5/1 Hybrid ARM | Fixed-Rate Mortgage |

|---|---|

| Low fixed-rate for first five years, then annual adjustments | One fixed rate for entire loan term |

| Monthly mortgage payments fluctuate with market rates | Same monthly payments throughout term |

| Great for house flippers | Great for long-term homeowners |

Is a 5/1 ARM loan right for you?

Unfortunately, no one answer suits everybody’s situation. Do you plan on spending a decade in the home? Then an ARM likely isn’t for your lifestyle. Are you looking to spend two years flipping the house before moving on? A 5/1 ARM may be the one for you!

The best thing you can do is read up on adjustable-rate mortgages to find out whether that low initial interest rate will provide you the flexibility you crave.

FAQs

What is the difference between a 5/1 and 30-year ARM?

These terms refer to different things in the mortgage world. A 5/1 ARM is a specific kind of mortgage, one that changes from a fixed interest rate to an adjustable one. The “30-year” refers to the total mortgage term length.

While this is a common term length, not all mortgages are 30 years and neither are 5/1 ARMs. Mortgages may last as little as 10 years or as long as 30 years.

What is an FHA 5/1 ARM program?

An FHA 5/1 ARM loan is an ARM backed by the Federal Housing Authority. Most lenders will offer something backed by the FHA. Ask a real estate agent if you are unable to find a good loan officer for your home.

Can you pay off a 5/1 ARM early?

Most mortgage lenders allow borrowers to pay off their loans early, but this isn’t always the case. If your lender doesn’t allow this, you’ll have to pay a prepayment penalty fee. So yes, you can pay off a 5/1 ARM early, but check the terms of your loan before you do.

What is a 5/1 ARM interest-only loan?

An interest-only loan only requires monthly payments on interest rather than payments on the interest and principals. However, in the case of a 5/1 ARM, this is only true for the first five years of your loan. Once this period ends, you’ll start making payments towards both the interest and principal.

What is the difference between a 5/1 and a 7/1 ARM?

The key difference between a 5/1 and 7/1 is the length of time for the initial rate. The 5/1 will have your initial rate for a total of five years, while the 7/1 ARM will switch to adjustable rates after a whopping seven years. That’s not bad!

Key Takeaways

- A 5/1 ARM loan is a hybrid between an adjustable-rate mortgage and a traditional fixed-rate mortgage.

- You keep a low fixed-interest rate for the first five years and then switch to an adjustable-rate for the remainder of the mortgage.

- The variable rate adjusts according to market research.

- This is one of the more popular loan options for people who want to have a little bit of savings at the start of their move-in.

Find your perfect home loan

Has this got you itching to look for a mortgage loan? Look no further! SuperMoney offers in-depth reviews on some of the most popular mortgage lenders. This includes lenders who specialize in ARM loans, too!

You can read and compare rates right here, all without leaving the comfort of your home. Be sure to keep in mind all adjustable-rate mortgages and find the loan that suits your financial lifestyle.

Table of Contents