What is a Mortgage Note?

Last updated 03/21/2024 by

Camilla Smoot

Summary:

A mortgage note is a legal document that lays out the terms and conditions of a home loan between the lender and the borrower. It states who the lender and borrower are, what the repayment plan is, and what will happen if the payments stop.

Buying a home is an exciting and stressful time for anyone. There is a lot of work to be done before buying a home, such as researching lenders and brokers. After finally finding the place of your dreams, you will receive a lot of important paperwork. All this can be overwhelming, so it’s important to understand the significance of each document.

One of these important legal documents is a mortgage note. Not everyone knows what a mortgage note is. This article will help you understand what mortgage notes are and how they impact you and your new home.

Compare Mortgage Lenders

Compare rates from multiple lenders. Discover your lowest eligible rate.

What is a mortgage note?

Mortgage notes, also known as promissory notes, are legal documents that state how the borrower will repay the loan. It also agrees to use the home as collateral if the monthly mortgage payments are not met. It is designed to provide mortgage lenders with security that the money they are loaning will be paid back. You will receive a mortgage note after closing your mortgage.

The monthly payment amount, principal and interest payments, and interest rate will be listed in the mortgage statement. This is a separate and different document from a mortgage promissory note. Your mortgage broker can help you go over your mortgage note and mortgage statement.

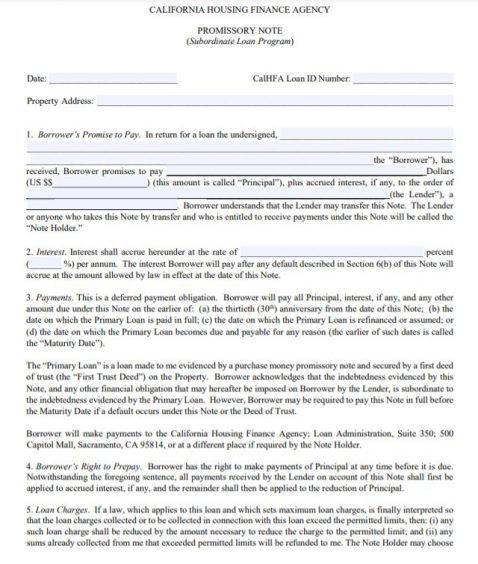

What does a mortgage note look like?

A mortgage note is a legal document usually titled as “note”, “mortgage note”, or “borrower’s note.” There will be blank spaces that you and the lender sign or fill out. The document lays out due dates for payments, length of time for repayment, where to send payment, and consequences if the loan is not paid or the promissory note is broken.

The mortgage notes state:

- How much money was borrowed

- The amount of the down payment

- The interest rate, and whether it’s a fixed interest rate or adjustable interest rate.

- Who the borrower and mortgage lender are

- A repayment plan

- How often payments are required (a bimonthly or monthly payment)

- What will happen if monthly payments stop

Your mortgage note will be with your closing documents, so be sure to keep an eye out for it when going through them.

Who holds the original mortgage note?

The lender, or lending institute, holds the original mortgage note. The borrower receives an original copy of the promissory note once the loan has been paid off. Borrows receive a copy of the mortgage note with their closing documents.

What if the borrower defaults or prepays?

A mortgage default is when the borrower misses payments. A prepay is when the borrower makes early payments in addition to their monthly mortgage payments.

If the borrower defaults, the foreclosure process could be started by the real estate investors. This is called a judicial foreclosure.

Some lenders charge a penalty on prepayments to compensate for the loss of interest payments. If your lender does charge prepayment penalty fees, take in into consideration when calculating the cost-benefit analysis of paying off your mortgage early.

What if the borrower pays off the mortgage in full?

Once the home loan is paid in full, the borrower is now the property owner. They will receive the original mortgage note when the loan is paid off.

Different types of mortgage notes

The most common types of home loans include a secured loan, private loan, and institutional loan. The mortgage notes used for each of these mortgage types may vary slightly, but the basics are the same. It is a legal document that states the terms of the loan between the lender and the borrower. Other financing vehicles that use a property as security, such as shared equity mortgages, home equity lines of credit, and home equity loans, also use similar documents to a mortgage note.

Secured loan

A secured loan is when the property being loaned is used as collateral. A promissory note for a secure loan might include a longer payment term and a lower interest rate. A secure loan provides the lender with less of financial risk.

Private loan

A private loan is when the lender owns the property they are lending. Mortgage notes for a private lone tend to be less regulated and the lender can draft it to their own liking.

Institutional loan

Institutional loans are heavily regulated. A promissory note for an institutional lone must follow standard interest rate and payment terms. They generally allow 15 or 30 years for payment.

How to get a copy of your mortgage note

The borrower will usually receive your mortgage note as part of the closing documents. Once the borrower pays off the home loan completely, the original version of the promissory note will be given to the borrower. If the mortgage note is lost or destroyed, another copy can be received by requesting it from your mortgage servicer, searching under your county’s records, or contacting the registry of deeds.

Selling a mortgage note

Lenders are the note holder and can sell the mortgage note at any time. However, they are legally required to inform the borrower that the mortgage note is being sold. After a mortgage note is sold, the only thing that changes for the borrower is whom and where they send their payments to.

A mortgage note is usually sold when the lender either needs a large amount of money immediately or does not want to wait for the monthly payments. Once it is sold, the former lender is no longer the note holder or has any obligations to the borrower.

Frequently asked questions about mortgage notes

What is the purpose of a mortgage note?

After negotiating a loan, you will receive a mortgage note (also referred to as a promissory note or mortgage promissory note). A mortgage note lays out the conditions of the loan between the lender and the borrower. It will state when payments are due, the interest rate, what will happen if payments stop, and more. Property is usually foreclosed by real estate investors if payments are not made on time.

You will receive a copy of the mortgage note with your closing documents. The lender will hold onto a copy of the original. Once your home loan is paid off in full, you are the new owner of the property and will receive the original copy of the mortgage note.

Where do I find my mortgage note?

You will receive your mortgage note with your closing documents. If you lose or destroy your promissory note, you can obtain another copy by contacting the registry of deeds or searching under the county’s records. You can also go to your mortgage servicer and request it.

What happens when you buy a mortgage note?

When you buy a mortgage note, you are buying the debt that still needs to be paid. You are not buying the real estate property that the mortgage note talks about. You are buying the debt and secured interest in the real estate.

How much does a mortgage note cost?

When an investor buys a mortgage note, they are not buying the property. Instead, they are buying the debt and secured interest in the property. The cost of a mortgage note depends on the payment history, age of the note, and the loan-to-value ratio of the property. According to American Note Capital, most notes range from $20K to $50K, but it all depends on the underlying property and mortgage.

Key takeaways

- A mortgage note is a legal document that states the terms of the mortgage loan between the lender and the borrower.

- Mortgage notes are sometimes referred to as a promissory note or a mortgage promissory note.

- A promissory note details what will happen if the monthly payments are not made.

- A mortgage note can be sold by the lender anytime after informing the borrower of their decision.

Camilla has a background in journalism and business communications. She specializes in writing complex information in understandable ways. She has written on a variety of topics including money, science, personal finance, politics, and more. Her work has been published in the HuffPost, KSL.com, Deseret News, and more.

Table of Contents