What is an Outstanding Balance? Meaning & Examples

Summary:

The outstanding balance on your credit card refers to the total amount of debt still unpaid on your credit card. Also known as the current balance, this is one of the most important metrics to keep in mind as you look to improve your credit score.

One of the most important parts of financial responsibility is handling credit card debt. And to do this, you have to read your credit card statement whenever it comes in. Not only does this let you know how much your outstanding balance is, but you may also have a better understanding of your overall financial position.

Your outstanding balance is the amount of money you have yet to pay off on your credit card. Understanding this metric can help you determine how much you owe the credit card company, as well as how to reduce your debt. It could also help you figure out how to improve your credit score.

What is an outstanding balance?

An outstanding balance is the total amount of money still left unpaid on a credit card. It is also known as a current balance and usually includes the following:

- Regular purchases

- Bill payments

- Fees

- Interest charges

- Cash advances

- Balance transfers

Anyone who uses a credit card would most likely incur some level of debt on it. Over time, the expectation is that the card owner pays off that debt to the best of their ability either by making the minimum payment or a larger payment that covers most of the balance. The credit card billing statement shows whatever is left.

As you would expect, the outstanding balance on your credit card changes whenever you use it to pay for something. For example, if you go on a shopping spree and end up spending $200 on your card, it is added to your outstanding balance as soon as the transaction is posted to your account.

What is an average outstanding balance?

The average outstanding credit card balance in 2022 was around $1,613 if you include all credit card accounts, according to the latest Federal Reserve data. However, the average consumer with credit card debt has around $5,590 in outstanding credit card balances, according to the latest Experian report. Put simply, the average outstanding balance refers to the amount of money left unpaid on your credit card debt over a specific period of time. Though the most common period is by month, you can also calculate the daily average outstanding balance. You can compare this average to the average collected balance, which calculates how much you’ve paid towards your card balance during the same amount of time.

To calculate the average outstanding balance, simply add your balance each month of a statement cycle and divide it by the number of months.

Pro Tip

Credit card companies report outstanding balances monthly to credit reporting agencies, usually on a card’s statement date. To keep your credit score in good standing, try to pay your credit card bill before the statement date each month to keep your outstanding balance low.

How an outstanding balance affects your credit score

Your credit score demonstrates your trustworthiness in the financial world. The better your score, the better loan terms and interest rates you may be eligible for. However, having a high outstanding balance can hurt your credit score. This is especially true for people who use a large percentage of their credit limit.

Credit limit and credit utilization ratio

Most credit card issuers have credit card limits. These limits can run over a month or year and help to keep a person’s spending and debt in check. They are also important determinants of financial health.

You can tell the impact of your current balance by calculating your credit utilization ratio. This number shows how much of your credit limit is now in your current balance. In other words, the credit utilization ratio tells you how much of your available credit has been spent and how much you have left.

To understand this, consider the following example:

- You got a credit card from your bank, with a spending limit of $10,000.

- After several transactions, you now have an outstanding balance of $3,000.

- If you make a $400 transaction that hasn’t been reflected yet, your balance is now $3,400. This means that you’ve used up 34% of your available credit, which is your credit utilization ratio.

- So, your available credit is $6,600 ($10,000 – $3,400).

How does your credit utilization ratio affect your credit score?

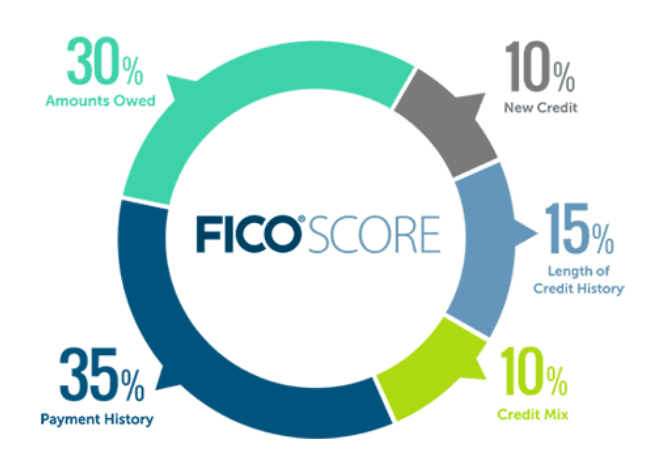

Your credit utilization ratio makes up about 30% of your entire credit score, meaning it can have a heavy impact if your ratio increases quickly. Ideally, you should keep your available balance as high as possible, lowering your ratio, to maintain a healthy credit score.

At the same time, having a high balance also means that you need to make more monthly payments to reduce the ratio. Since you’re expected to pay down the balance on your credit card, it’s in your best interest to keep the debt as low as possible.

Pro Tip

You can also reduce your ratio by opening a new credit card account. Since your new account will give you access to additional credit, your available balance will increase and your ratio will decrease. To find the right credit card for your spending habits, take a look at some of the credit card issuers below.

How to check your outstanding balance on a credit card

Fortunately, financial institutions make it really easy to check your outstanding balance on a credit card. You can check your credit card balances over the phone, online, through an institution’s mobile app, or by setting up regular email or text notifications.

1. By phone

You can call the number on the back of your credit card to get your issuer’s customer service line. You’ll probably have to enter your card number as well as any other identifying number (could be your billing zip code or the last four digits on your social security number) manually to verify your account is actually yours.

Card issuers can easily verify the information you submit as long as you follow the instructions. In some cases, you may have to speak to a representative of the card issuer, but the customer service line may be able to robotically list your balance.

2. Online

If you have an online account set up for your credit card, then you could check your total outstanding balance over the internet as well. All you have to do is:

- Fire up a web browser

- Go to your card issuer’s website and log into your account

- Navigate to your balances, which should list your total outstanding balance.

If you don’t have an online account set up, you could always create one by visiting your card issuer’s website. If you need some help, then you could contact your card issuer’s customer service line.

Pro Tip

Most credit card issuers require you to create a profile when signing up. Remember to select a memorable username and a secure password. Your online account is a window into your finances, so security is very important here.

3. Getting regular account notifications

After setting up an online account with your credit card issuer, you can decide how closely you would like to monitor your account. One of the easiest ways to do this is by opting for regular notifications from your card issuer.

Notifications could come in through emails, push notifications, or text messages whenever there’s new account activity. They could also provide updates about the outstanding balance for better monitoring. Some card issuers offer the option to get updates after each card transaction or after each monthly debt repayment.

4. Use a smartphone app

Just about everyone uses a smartphone these days, and financial institutions know that. Most institutions now have a mobile app you can download, which makes it easy to monitor your credit card and its details. Using these apps, you can check your monthly balance, account number, payment due dates, as well as other important card details.

When you download the app, you should be able to log in using the same details you used to create your account online on the card issuer’s website.

Outstanding balance vs. remaining balance

Whenever you spend money on your card, your outstanding balance increases. However, each month (or several points throughout the month) you should make at least the minimum payment towards your balance. When you eventually start repaying, the portion of your statement balance that is left becomes your remaining balance.

Although outstanding balance and remaining balance are terms used to describe money owed to the card issuer, the latter doesn’t kick in until you actually start paying off the former. Until these payments start, your outstanding balance and your remaining balance are the same.

To understand the difference between both balances, consider this example:

You have a limit of $5,000 on your card and you decide to spend $2,000. When you check your credit card account, you’ll see $2,000 listed as your outstanding balance.

At the end of the month, you decide to pay $700 to settle some of your credit card debt. When you check your credit card balance again, you’ll find that you still owe $1,300 to the card issuer. That figure is your remaining balance.

FAQs

Do I need to pay the outstanding balance?

While you do need to make at least the minimum payment on your outstanding balance, you don’t have to pay off your entire outstanding balance at once. The beauty of modern finance is that you can pay in installments and at your own convenience.

Having said that, remember that your credit utilization ratio plays an important part in your credit score. This means paying your entire outstanding balance could be a way to keep your ratio low and your credit score high.

Why do I have an outstanding balance?

The outstanding balance appears whenever you use your credit card to make payments. It reflects your credit card debt by showing how much you need to pay back at the end of the month or over several monthly payments.

Does outstanding balance mean overdue?

No, it doesn’t mean your payment is past due. Your outstanding balance increases whenever you make a payment using your credit card. However, if you don’t make at least the minimum payment towards your balance before the payment due date, then your bill will be overdue.

Key Takeaways

- The outstanding balance is the amount of debt you have left to pay on your card.

- An outstanding balance helps determine your credit score. A high balance will negatively affect your credit score — especially if you’re using a large percentage of your credit limit.

- You can check your entire outstanding balance in a few different ways, including calling your card issuer and using a smartphone app.

- Until you start paying off your credit card debt, the outstanding balance and remaining balance are the same thing.

Table of Contents