HELOCs End-of-Draw Period: Beginning of a Mortgage Crisis?

Last updated 10/29/2025 by

Andrew Latham

Edited by

Ante Mazalin

If you thought the housing bubble was behind us, think again. A new home loan financial storm is brewing and most of us are clueless about it. This article looks into home equity lines of credit and how they could trigger the next financial crisis.

Back in July 2014, the Federal Reserve, the Office of the Comptroller, FDIC, the National Credit Union Administration, and the Conference of State Bank Supervisors sent out an interagency warning (source). The concern was that the monthly payments for home equity lines of credit (HELOCs) were going to rise sharply for millions of borrowers between 2014 and 2017. The warning didn’t get much coverage back in 2014 and it’s not making many headlines today either. But that doesn’t mean the Federal Reserve was wrong.

One of the reasons this issue is not getting much attention is its complexity. Even consumers who have a HELOC don’t always understand the terms of their loan.

Compare Home Equity Lines of Credit

Compare rates from multiple HELOC lenders. Discover your lowest eligible rate.

What on earth is a HELOC?

A home equity line of credit (HELOC) is a loan that is secured by a residential property and set up as a line of credit instead of a fixed amount.

Unlike typical loans, borrowers don’t have to withdraw all the money at once with a HELOC. The advantage is borrowers only have to pay interest on money they use, but the balance is always available if necessary. In that sense, they work like a credit card.

Another difference between a conventional loan and a HELOC is that the loan principal does not have to be paid until the end-of-draw period. Draw periods typically last 10 years. During the draw-out period, borrowers only have to pay the interest on the balance. The low minimum payments make it seem easy and cheap to borrow money. However, once the draw period ends, the principal on the loan is due. Depending on the terms of the loan, borrowers must either pay the balance immediately or repay it over the remaining loan term. In any case, the increase in monthly payments can be a shock to a family’s budget. Typically, monthly payments increase by 300% to 400%.

Why are HELOCs a problem now?

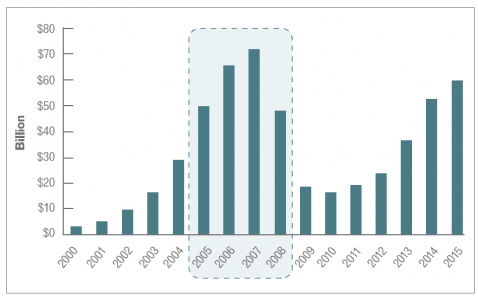

Remember the good old days between 2005 and 2008 when all homeowners felt rich. It was just before the housing collapse and it looked like home prices could only go up.

The rise in home prices encouraged many homeowners to get a line of credit and use their home as collateral. Now the drawing out period is ending on many HELOCs, banks are hitting homeowners with payments that are three to four times larger than what they have been paying for years.

HELOC balances by year. Source: Experian

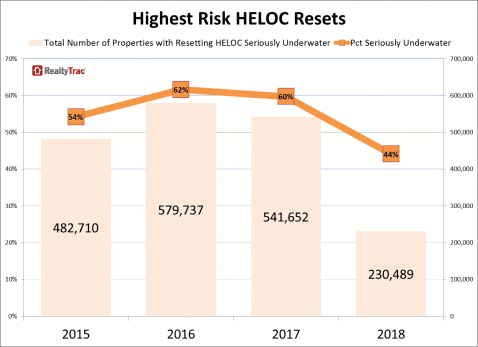

62% of properties with a HELOC are underwater

Higher monthly payments are not the biggest problem households with a HELOC face. In most cases, the equity on property that secures the home equity loan no longer exists. Or worse, it has negative equity.

Here’s the thing. There are 3.3 million HELOCs with an estimated balance of $158 billion that were originated between 2005 and 2008, according to a 2015 report by RealtyTrac. The same report estimates that, in 2016, 2 million of the HELOCs where the draw out period ended (62% of the total) are secured by residential properties that are underwater.

Let me say that again. Sixty two percent of the HELOCs that will start to charge borrowers higher payments this year are upside down. These are homes with a loan to value ratio of 125% or more.the loan. Next year, doesn’t look much better. According to RealtyTrac’s estimates, 60% of the HELOCs where the borrowers have to start making principal payments on will be underwater (source).

Source: RealtyTrac

What do households do when they find out they have to pay three times as much on a line of credit secured by an underwater home? In 2014, after only four months of larger payments, borrowers who got a HELOC in 2004 (10 years earlier) were delinquent on $1.8 billion in HELOCs. But here’s the scary part. In 2014, only 40% of the homes were underwater. How many will default in 2016 and 2017 with underwater ratios of 62% and 60%? Just as it happened during the subprime meltdown, the main risk is the change in payments when borrowers go from interest-only payments to fully paying for a loan they can no longer afford.

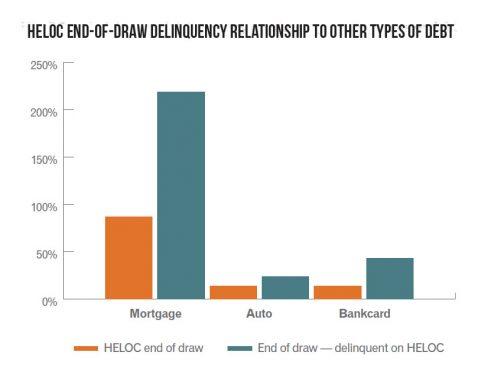

Another concern is that problems with HELOCs don’t occur in a vacuum. They have a domino effect on other types of debt, particularly mortgages. According to a 2015 study by Experian (source) consumers who reach the end-of-draw period on their HELOCs are more likely to default on car payments, credit card debt, and conventional mortgages.

Source: Experian

How did this happen in the first place?

In the good old days of “streamlined underwriting,” 100 percent combined loan-to-values were the norm. If you had a pulse and the slightest equity, you qualified for 100 percent combined loan-to-value loans. Lenders gave out mortgages and home equity loans to anyone who asked for one. In many occasions, borrowers didn’t even have to provide basic documentation to confirm their source of income (source).

Often, lenders marketed HELOCs as a way to pay down the balance of the mortgage and avoid the private mortgage insurance. Never mind the HELOCs were leveraged on the same property. Not surprisingly, deregulation and access to cheap credit caused millions of homeowners to view their homes as ATMs and overextend themselves. Borrowers treated homes as bottomless piggy banks until, well, the bottom of the mortgage industry fell out.

What can HELOC borrowers do?

If you are one of the millions of borrowers facing a HELOC payment shock, don’t panic. There are several options available.

- Those who have good credit but not enough equity in their home, can probably extend the terms of the HELOC or negotiate some other kind of payment flexibility with their lenders.

- If you have good credit and plenty of equity, you may be able to refinance your loan. You could even get better rates than your existing HELOC by purchasing a new mortgage with your current lender or another mortgage company.

- Your options are limited if you have poor or fair credit and no equity. In such cases, your only option may be to mitigate the effect of the higher monthly payments by tightening your belt and sticking to a budget.

If your budget cannot stretch any further, your only option may be to minimize the damage to your credit.

Considering a mortgage refinance? Click here for a complete guide on mortgage refinancing.

Compare HELOC Strategies

- HELOC vs Personal Loan — Find out which financing option fits your needs best.

- HELOC for Emergency Expenses or Medical Bills — Learn how to use home equity safely during a crisis.

- HELOC for Renovations or Repairs — Turn equity into upgrades that add value to your home.

- Refinancing a HELOC — Reduce rate risk and create predictable payments.

- Best HELOC Alternatives — Review other equity-based and unsecured funding options.

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

Share this post:

Table of Contents