Home Equity Surges In Q2 2024: Key Takeaways For U.S. Homeowners

Last updated 11/14/2024 by

Andrew Latham

Edited by

Miron Lulic

Summary:

U.S. homeowners gained an average of $25,000 in home equity in Q2 2024, with nearly half of all mortgaged properties now “equity-rich.” Rising property values continue to boost household wealth, giving homeowners additional financial security and options.

As property values surge across the country, U.S. homeowners are gaining significant new wealth—an average increase of $25,000 in home equity over the past year. Nearly half of all mortgaged properties are now considered “equity-rich,” giving many Americans a level of financial security and opportunity they may not have anticipated.

In this article, we’ll unpack what these equity gains mean for homeowners, diving into the latest data and exploring practical ways to leverage your home’s rising value. Whether you’re eyeing home improvements, consolidating debt, or simply curious about your home’s potential, this guide covers the top options to consider.

Compare Home Equity Lines of Credit

Compare rates from multiple HELOC lenders. Discover your lowest eligible rate.

Major trends in U.S. home equity growth for Q2 2024

Recent reports from the Federal Reserve, ATTOM,and CoreLogic reveal significant growth in home equity across the U.S., driven by robust real estate markets in many regions. Here are the key insights.

9.8% increase in home equity

In Q2 2024, U.S. homeowners experienced a notable 9.8% increase in home equity compared to Q2 2023, according to recent data from the Federal Reserve.

This sharp uptick underscores the impact of rising home values on household wealth, providing many with a larger financial cushion and more options for leveraging their home’s value. Let’s take a closer look at what this means for homeowners and how it aligns with broader market trends.The average household gained $25,000 in home equity

According to CoreLogic, U.S. homeowners with mortgages saw their equity increase by an average of $25,000 from Q2 2023 to Q2 2024. This increase in equity reflects the impact of strong home price appreciation across the country, as well as low housing inventory in many areas. Rising property values have created substantial wealth for homeowners, giving them increased financial security and options for leveraging their home’s value if needed.

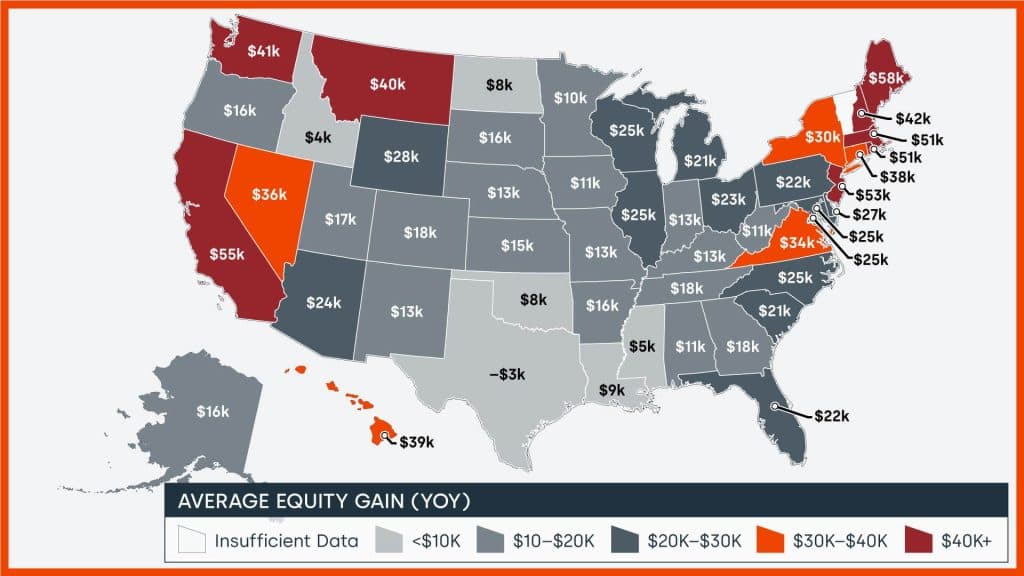

Home equity gains are not spread evenly

While home equity has risen across the country, gains are not evenly distributed. On the West Coast, California ($55K), Washington ($41K), and Hawaii ($39K), led in equity growth, with many homeowners in these states gaining over $50,000 in equity in just a year. High property values and strong demand, particularly in urban centers, have contributed to rapid home appreciation in these areas.

In the Northeast, states such as Maine ($58K), Rhode Island ($51K), and Massachusetts ($51K) also saw significant home equity growth, driven by similar factors like high property demand, limited housing supply, and robust local economies.

On the other hand, certain regions in the Midwest and South saw more modest increases in home equity, reflecting slower property value appreciation and economic factors unique to these areas.

49% of homes with a mortgage are “equity-rich”

ATTOM’s report shows that nearly half (49%) of all mortgaged homes in the U.S. were classified as “equity-rich” in Q2 2024. A property is considered equity-rich when the homeowner has at least 50% equity in their home. This marks a substantial increase compared to previous years and reflects a broader trend of wealth accumulation among homeowners. In many regions, particularly in the Northeast and the West Coast, over 60% of homes are now equity-rich.

Record-low underwater properties

Only 2.8% of mortgaged U.S. homes were “seriously underwater” in Q2 2024, according to ATTOM. A home is “seriously underwater” when the mortgage balance exceeds the property’s market value by at least 25%. This is the lowest percentage in years and signals that fewer homeowners are at risk of financial hardship due to negative equity. Declining underwater rates are largely due to rising home prices, which have helped lift property values and strengthen homeowners’ financial positions.

Trends in home equity financing

Since the beginning of 2022, total debt in home equity loans and HELOCs has been steadily increasing. This trend reflects rising home values and homeowners’ interest in leveraging their growing equity. As shown in the chart below, total home equity loans and HELOCs hit historic highs in the mid-2000s, then sharply declined following the 2008 financial crisis. However, they are on the rise again as more homeowners see value in tapping into their growing home equity.

The latest data from the Federal Reserve shows that the total balance of home equity loans has increased by 22% since Q1 2022 to Q2 2024 (from $436.7 billion to $533.9 billion). HELOC balances on the other hand rose by 16% in the same period (from $325.6 billion in Q1 2022 to $378.5 billion in Q2 2024). This increase highlights a renewed interest in home equity financing as property values continue to climb.

Home equity financing options

The increase in home equity provides many homeowners with new financial options, but it’s important to weigh these carefully. Using home equity can be a helpful tool for funding large expenses or consolidating high-interest debt. However, it also comes with risks. Here are the most widely used types of home equity financing.

- HELOC: A flexible line of credit you can draw from as needed, but interest rates can vary, potentially increasing costs.

- Home equity loan: Provides a lump sum with fixed payments, but you’ll be locked into a new monthly obligation.

- Home equity agreement (HEA): Offers cash upfront without monthly payments, though you’ll share a portion of your home’s future value.

- Cash-out refinance: Replaces your mortgage with a larger one, giving you cash but possibly increasing your interest rate.

- The Federal Reserve reports a 22% increase in home equity loan balances and a 16% rise in HELOC balances from Q1 2022 to Q2 2024, reflecting renewed interest in home equity financing as property values rise.

Are you curious how much each option costs and would like a detailed analysis of the pros and cons of each option? Read this article for a primer on the costs of home equity financing options.

Key takeaways

- U.S. homeowners gained an average of $25,000 in home equity in Q2 2024, driven by rising property values.

- U.S. homeowners’ home equity in Q2 2024 increased by 9.8% when compared to the same period in 2023.

- Nearly 50% of all mortgaged properties are now “equity-rich,” with homeowners holding at least 50% equity in their homes.

- The number of “seriously underwater” properties is at a record low of 2.8%, reflecting a healthy housing market.

- Options to tap into increased equity include HELOCs, home equity loans, home equity agreements, and cash-out refinancing.

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

Share this post:

Table of Contents