How the Fed’s Latest Rate Cut Affects You: Who Wins, Who Loses, and What to Do Next

Last updated 12/19/2024 by

Andrew Latham

Edited by

Miron Lulic

Summary:

The Federal Reserve recently reduced interest rates by 25 basis points, offering potential savings for borrowers but presenting challenges for savers and retirees. This article explores the winners and losers of the Fed’s latest rate cut and provides actionable advice to help you adapt your financial strategy and make the most of the economic environment.

The Federal Reserve has cut interest rates by 25 basis points (0.25%)—a move aimed at boosting economic activity as inflation moderates and growth slows. While the Fed’s goal is to stimulate spending and investment, the impact depends on where you stand financially. Borrowers, for instance, could see lower payments on loans, but savers might experience shrinking returns on their deposits.

Let’s explore the winners and losers of this decision and how you can fine-tune your finances to take advantage of—or mitigate—the effects of lower rates.

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

How the Fed rate cut works

The Federal Reserve uses the federal funds rate to guide economic activity by influencing borrowing and saving costs. When the Fed reduces this rate, borrowing becomes less expensive, but savers and retirees may earn less on their deposits and fixed-income investments.

Here’s how a Fed rate cut typically works:

Borrowers: Lower rates decrease the cost of variable-rate loans, such as credit cards, adjustable-rate mortgages (ARMs), and home equity lines of credit (HELOCs).

Savers: Savings accounts, certificates of deposit (CDs), and money market accounts typically see lower yields, reducing returns on deposits.

This latest 25 bps cut reduces the federal funds rate to 4.25%–4.50%, adding to the series of adjustments since the tightening cycle began in 2022.

Savers: Savings accounts, certificates of deposit (CDs), and money market accounts typically see lower yields, reducing returns on deposits.

This latest 25 bps cut reduces the federal funds rate to 4.25%–4.50%, adding to the series of adjustments since the tightening cycle began in 2022.

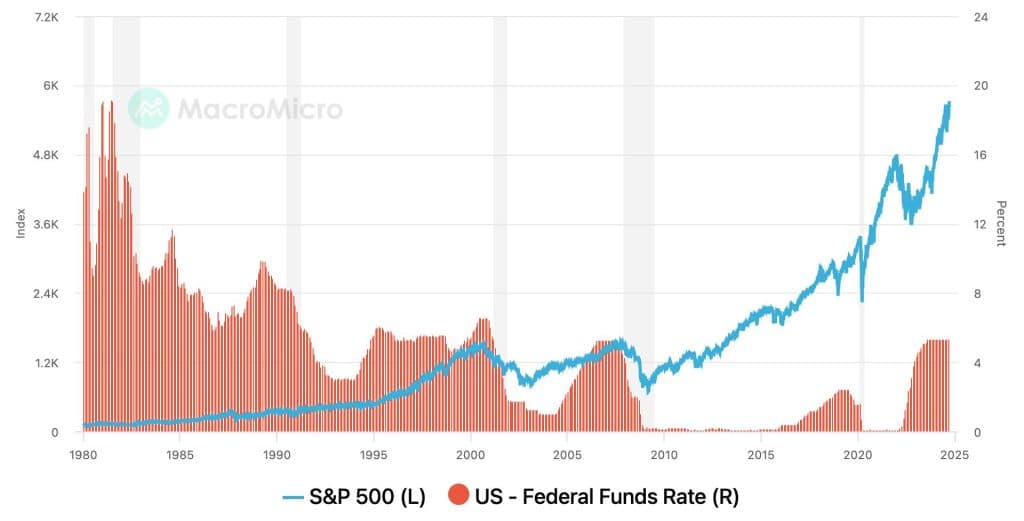

As shown in the graph above, the federal funds rate influences other key benchmarks like the prime rate, 30-year fixed mortgage rate (FRM), and auto loan rates. While some rates adjust quickly to Fed actions (like the prime rate), others, such as fixed mortgage rates, depend on broader market factors like bond yields.

Who benefits from the Fed’s rate cut?

The winners of the latest rate cut include borrowers with variable-rate loans, credit card users, and stock market investors. Let’s break it down:

Credit card users

If you have a variable-rate credit card, the interest rate may decrease slightly in response to the Fed’s decision. Since credit card APRs often follow the federal funds rate, the 0.25% cut might mean small savings on interest charges.

For example, if you have a balance of $5,000 on a card with a 20% APR, a 0.25% reduction could save you around $12.50 annually. While modest, every bit helps—especially if you consolidate debt or transfer your balance to a card with a 0% APR introductory offer.

Borrowers with variable-rate loans

Borrowers with loans tied to the Fed’s rate—such as ARMs or HELOCs—are likely to see lower payments. These loans typically adjust their rates in line with Fed policy, so a 25 bps cut could result in tangible savings.

For example, if you owe $250,000 on a HELOC at 7%, this 0.25% cut could reduce your annual interest by $625—or around $52 per month. Over time, these savings add up, especially for borrowers with significant outstanding balances.

Stock market investors

The stock market often reacts positively to lower rates. Cheaper borrowing costs improve corporate profitability, while lower bond yields make stocks more appealing to investors seeking higher returns.

Historically, the S&P 500 has performed well during periods of falling interest rates, with sectors like technology, retail, and automotive leading the charge.

Who loses with the Fed’s rate cut?

The losers from this rate cut include savers, retirees, and banks, all of whom face challenges as interest rates decline.

Savers

Savings accounts and CDs are likely to offer reduced returns as banks adjust to the lower federal funds rate. For instance, a high-yield savings account that recently offered 5% interest might drop to 4.75%.

If you’re relying on deposit accounts for income, consider locking in rates with long-term CDs or exploring alternative investments like Treasury bonds or dividend-paying stocks.

Retirees

Retirees depending on fixed-income products like bonds or CDs may see reduced yields, shrinking their income streams. Lower rates can also hurt annuities or other income-focused investments tied to interest rates.

To mitigate this impact, retirees might explore options such as REITs, preferred stocks, or income-generating ETFs. Diversifying your portfolio can help maintain steady cash flow in a low-rate environment.

Banks

Lower rates often compress bank profit margins. As lending rates drop, banks earn less on loans, while reduced deposit rates may drive customers toward higher-yield investments. This double hit can reduce profitability for banks, particularly those with significant exposure to variable-rate loans.

What to do now

Here’s how to navigate the current rate environment:

Credit Card Users: Focus on paying down balances, consolidate with low-interest loans or 0% APR balance transfer cards.

Borrowers: Take advantage of lower rates by refinancing or consolidating loans.

Savers: Consider higher-yield alternatives like Treasury bonds, dividend stocks, or long-term CDs.

Retirees: Reassess your portfolio to include diverse income-generating investments.

By staying proactive, you can minimize the downsides of the Fed’s rate cut while capitalizing on its benefits.

Borrowers: Take advantage of lower rates by refinancing or consolidating loans.

Savers: Consider higher-yield alternatives like Treasury bonds, dividend stocks, or long-term CDs.

Retirees: Reassess your portfolio to include diverse income-generating investments.

By staying proactive, you can minimize the downsides of the Fed’s rate cut while capitalizing on its benefits.

Frequently asked questions

How do Fed rate cuts impact mortgage rates?

Adjustable-rate mortgages (ARMs) usually adjust in response to Fed rate cuts. However, fixed-rate mortgages are more influenced by long-term bond yields and market demand.

Will credit card interest rates drop after the Fed rate cut?

Variable-rate credit cards often see APR reductions after a Fed rate cut. However, savings may be minimal unless you carry a large balance.

What can savers do to offset lower savings rates?

To offset lower savings yields, consider investing in Treasury bonds, dividend-paying stocks, or **high-yield CDs** to maintain returns.

Key takeaways

- The Fed’s 25 bps rate cut reduces borrowing costs for credit card users and borrowers with variable-rate loans.

- Savers and retirees face lower returns from deposit accounts and fixed-income investments.

- Stock market investors stand to benefit from improved corporate profitability and rising equities.

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

Share this post:

Table of Contents