How To Find Auto Insurance That Covers Any Driver

Last updated 03/19/2024 by

Marcie Geffner

One of the many complicated facets of auto insurance is who—or what—is covered by an auto insurance policy. Is it the car? The driver? Or both?

The answer isn’t obvious, and the question leads to other questions, like:

- Can you drive someone else’s car if you have insurance, but the other person doesn’t?

- Can someone else who doesn’t have insurance drive your car if you have insurance?

- If someone else drives your car and causes an accident, are you responsible?hi

- If you cause an accident while driving someone else’s car, are you responsible?

The key word to answer all of these questions is “liability,” which refers to who’s financially responsible for losses and damages when an accident occurs.

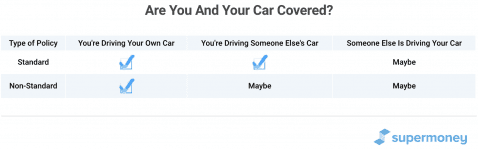

There are two types of auto liability insurance policies: standard and non-standard. Here’s a quick glance at what each policy covers:

To fill in the blanks, however, we have to dive a little deeper.

Compare Auto Insurance Providers

Compare multiple vetted providers. Discover your best option.

Standard auto insurance

“Standard auto insurance is aimed primarily at drivers with a good record who are low-risk drivers,” says Paul H. Cannon, a shareholder and trial attorney who handles motor vehicle injury cases at Simmons and Fletcher, a law firm in Houston, Texas.

Standard auto liability coverage protects both you and your car. That means you’re covered when:

- You drive your own car

- You drive someone else’s car

- Someone else drives your car

When a car is borrowed, the driver must have the owner’s permission and cannot be excluded by name from the owner’s auto insurance policy.

Standard auto insurance is aimed primarily at drivers with a good record who are low-risk drivers”

Auto insurance and negligence

If you have standard auto insurance and someone else borrows your car and causes an accident, you typically wouldn’t be financially responsible because you weren’t the driver.

There are exceptions, however.

For example, if you loaned your car to someone who was intoxicated, had no license, or had a poor driving record, and that person caused an accident, you might be held responsible because you entrusted your car to a reckless driver.

Non-standard auto policies are written for people who are higher risk drivers”

Non-standard auto insurance

“Non-standard auto policies are written for people who are higher risk drivers,” Cannon says.

You’re considered a high-risk driver if your record includes:

- Several accidents

- Multiple traffic tickets

- Any traffic violation causing a fatality

- A DUI or DWI

- Excessive speeding

- Reckless driving

- Illegal street racing

- Driving without a license

You only need one of those items on your record to be deemed a high-risk driver.

Non-standard insurance often excludes anyone who isn’t named on the policy. That means the car isn’t covered if someone else drives it, unless that person is on the policy.

A non-standard policy is often issued when a safe driver and a reckless one live in the same household, and the insurance company wants to exclude the reckless driver if he or she borrows the safe driver’s car.

Some non-standard auto policies are so narrow that they cover only one driver of one car, and that’s it. Allstate and Geico are two top insurers for high-risk drivers.

Other types of auto insurance coverage

Car insurance is regulated by the states, not the federal government. So, state law is an important factor in determining what a specific auto insurance policy does and does not cover.

There are also other types of auto insurance coverage in addition to liability.

If you’re responsible for an accident and your policy’s liability coverage isn’t adequate, these other coverages might protect you from financial loss:

- Comprehensive insurance

- Collision insurance

- Gap insurance

- Personal injury protection (PIP) or medical payments (MedPay)

- Uninsured or underinsured motorist insurance

- Uninsured motorist property damage insurance

These coverages and others can be included in a standard policy along with liability.

All auto insurance policies have coverage limits. If you or your car is involved in an accident and the damages are more than your policy will pay, you could be financially responsible.

Shop around for auto liability insurance

So, how can you find auto insurance that covers any driver?

- Shop for a standard auto insurance policy.

- Make sure your policy includes liability coverage.

- Read your policy, so you understand what’s covered and what’s not.

- Never let someone with a bad driving record borrow your car.

Easily compare auto insurance companies side-by-side to find the one that best meets your needs.

Related reading: Finding and signing up for the right policy isn’t all you have to do to best profit from auto insurance. You should also prepare to handle the claims process correctly if it comes to that. Start learning about this by reading How Long After an Accident Can You File a Claim?.

Marcie Geffner is an award-winning freelance reporter, editor, writer and book critic. Her work has been featured online and in print by The Washington Post, Los Angeles Times, Chicago Sun-Times, Urban Land, Business Start-Ups and Fox Business Network Online, among many other newspapers, magazines, and websites. With a bachelor’s degree in English from UCLA and MBA from Pepperdine University in Malibu, Geffner has impressive credentials in both story-telling and business management. A second-generation native of Los Angeles, Geffner now lives in Ventura, California, a surf city northwest of her hometown.

Share this post:

AddTable of Contents