How to Find Home Insurance that Covers Water Damage

JW

Last updated 03/19/2024 by

Jessica WalrackWater damage and freezing accounted for the largest share of homeowners insurance losses from 2014 to 2016, according to the Insurance Information Institute (III).

The good news is, homeowners and renters insurance policies typically cover water damage. However, the question you need to ask is, “What kind of water damage will be covered?” That’s where things get a little bit tricky.

As a general rule, if the event is “sudden and accidental” and caused by a covered peril, then it will be covered. Let’s take a closer look at what those requirements mean and how to find the right homeowners or renters insurance company for you.

Compare Home Insurance Providers

Compare multiple vetted providers. Discover your best option.

What qualifies as a “sudden and accidental” event?

Something that is “sudden and accidental” happens without prior notice, so is not the result of damage over time.

For example, if the pretty new supply hose on your washing machine suddenly bursts and floods a room in your home, that would be sudden and accidental.

However, if you had noticed the leak and failed to repair it, that claim would not qualify for coverage.

Insurance companies expect homeowners and renters to take care of their homes and only cover occurrences that are not the fault of the homeowner or renter.

Which perils are commonly covered?

According to the III, here are the most commonly covered perils in homeowners and renters insurance policies:

- Windstorm

- Explosion

- Fire

- Theft

- Lightning

- Hail

- Riot

- Civil commotion

- Falling object

- The weight of sleet, snow, or ice

- Damage caused by an aircraft or vehicle

- Smoke

- Vandalism

- Malicious mischief

- Artificially generated electrical current (except for a loss to a transistor, tube, or similar electronic component)

- Volcanic eruption

- Accidental overflow or discharge of water or steam from within:

- a plumbing system

- a heating system

- an air conditioning system

- an automatic fire-protective sprinkler system

- a household appliance

- Sudden and accidental bulging, cracking, tearing apart, or burning of:

- a heating system (steam or hot water)

- an automatic fire-protective system

- an air conditioning unit

- Freezing of:

- an automatic, fire-protective sprinkler system

- a household appliance

- a plumbing system

- a heating system

- an air conditioning system

If sudden and accidental water damage happens as a result of a covered peril in your policy, it is likely to be covered.

Water damage that is not covered by home insurance

What situations are usually not covered by water damage?

Floods and other perils

Standard homeowners insurance policies do not cover flooding that originates outside your house. However, you can purchase flood insurance separately.

Additionally, earthquakes, wars, landslides, nuclear accidents, mudslides, and sinkholes are usually not covered.

Water backup

When water backs up from a sewer or drain and enters your home, the damages are not typically covered. You will need a separate policy or endorsement to cover this event.

Unresolved maintenance issues

If damages occur as the result of a previously existing maintenance issue that was not taken care of, they will not be covered.

Replacing or repairing the source of water damage

Policies typically cover the costs to repair your home and belongings from a covered water damage event but do not cover the source of the damage.

For example, if your washing machine pipe burst, the cost to replace or repair the pipe won’t be covered. However, if your floor were ruined by the incident, the cost to repair it would be covered.

Water damage insurance claim tips

Worried your claim will be denied? Here are some tips to keep in mind:

Read the fine print of your policy

Before choosing a policy, read the fine print to find out what perils are covered and what exclusions exist. By taking the time to understand the details before you sign up, you will reduce the likelihood of your claim getting denied in the future.

Ensure your claim qualifies

Before calling to file a claim, ensure the situation qualifies. Is the damage the result of a covered peril? Was it preventable or does it qualify as “sudden and accidental”? Save yourself time and stress by first analyzing the situation yourself.

Don’t use the word “flood”

A quick way to start out on the wrong foot is to tell your insurer you have flooding. While you may have water flowing in your house that is covered, it’s better to choose words besides “flood” to describe it – unless, of course, you have flood insurance and want to use it.

Get evidence

When you see a mess, your first instinct may be to clean it up, but ensure you have enough evidence to prove your claim. If you do decide to clean anything up, take pictures and videos first.

Make your claim promptly

You should make your claim as soon as you realize covered damage has occurred. The longer you wait, the worse it can get, and you want to make sure the settlement is enough to cover the damages.

These tips can help you to get your claim approved. Now let’s take a look at some common questions related to water damage.

Frequently asked questions related to water damage

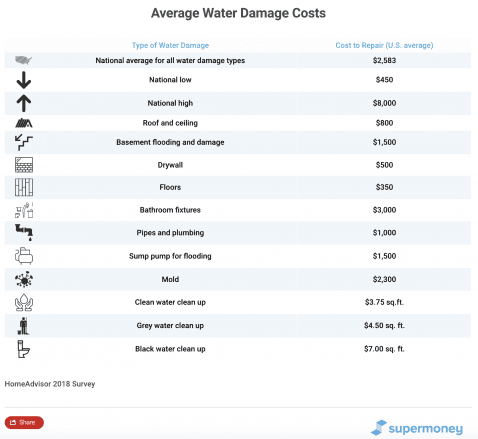

How much does it cost to repair water damage without insurance?

Here’s a look at the national average costs to repair water damage in the U.S.

Do most home insurance policies cover mold?

Home insurance will cover mold if it is caused by a covered peril and is sudden and accidental. If the insurer thinks that the mold was preventable, it will not be covered.

For example, if a new water hose on your washing machine bursts while you are away for the weekend and mold forms during that time, it would likely be covered.

However, if mold forms in your attic due to leaky shingles on a 40-year old roof, that will fall on the fault of the owner for not keeping up with roof maintenance.

Note, all of the states (except AK, AR, NY, NC, and VA) adopted an ISO mold limitation for homeowners insurance coverage. It allows insurers to exclude mold coverage unless it is the result of a covered peril.

Do most homeowners insurance cover broken water pipes?

Most homeowner’s insurance policies cover the damages caused by a broken water pipe if the break was sudden and accidental. If there is evidence it was leaking before bursting, the claim will be denied.

Are slab leaks covered by homeowners insurance?

Damages caused by slab leaks are sometimes covered by homeowners insurance policies, but it’s always wise to double check with your insurer.

If they are covered, the damages must be a result of a covered peril, and they can’t be due to normal wear-and-tear or neglect. Coverage will usually cover the cost of removing and replacing the slab but not the plumbing system.

Is water leak damage covered by home insurance?

Yes, water leaks that are sudden and accidental are usually covered.

Does homeowners insurance cover water damage from a leaking roof?

It depends on the cause of the leak. If it is caused by a covered peril and was sudden and accidental, it will be covered. If it is due to wear-and-tear, it usually will be your responsibility.

Does homeowners insurance cover water damage from leaking windows?

Homeowners insurance can cover leaking windows if they are leaking due to an unexpected event that is covered. Old or malfunctioning windows will fall under the wear-and-tear exclusion.

Does State Farm homeowners insurance cover water damage?

Yes, State Farm does offer coverage for water damage in certain scenarios as part of its homeowner’s insurance policy.

How to find the best home insurance company that covers water damage

Now that you have a deeper understanding of how water damage claims and home insurance policies work, how do you find the best home insurance provider?

Start by comparing coverage options, perils, exclusions, limits, deductibles, discounts, and customer service. For concerns about water damage, find out all the ins and out of the policy to find the one that best fits your need.

While there are many insurance providers to choose from, you can compare them side-by-side on SuperMoney’s Home Insurance Review page and read in-depth reviews if you want to learn more.

Renting your home? No problem. Click here to review renters insurance companies.

JW

Jessica Walrack is a personal finance writer at SuperMoney, The Simple Dollar, Interest.com, Commonbond, Bankrate, NextAdvisor, Guardian, Personalloans.org and many others. She specializes in taking personal finance topics like loans, credit cards, and budgeting, and making them accessible and fun.

Share this post: