3 Tips on How To Get Out Of An Annuity

BC

Summary:

You can get out of an annuity a few different ways, though not all of these ways are free of penalties or fees. This includes withdrawing your funds during the free look period, replacing your annuity, or simply withdrawing your money and accepting a penalty. If you surrender an annuity early, you’re likely to end up with a surrender charge from your insurance company. This is before you factor in any taxes you become responsible for or additional tax penalties assessed by the IRS, which can be up to 10%.

Investing and planning for your future and retirement is hard. We don’t always make the right choices. Deciding whether or not to get an annuity, and then choosing between a fixed or variable annuity (not to mention an immediate vs. deferred annuity) requires a lot of thought and, ideally, expertise.

If you’ve turned on a television in the last decade, you’ve likely seen one of the many JG Wentworth commercials where city bus riders operatically bemoan the plight of having an annuity but needing cash now. There are many reasons you may need to withdraw money from your annuity, and, clearly, people make mistakes. That’s okay.

We know just how hard financial planning can be. So, if you find yourself stuck with a bad annuity, or you’re simply feeling like your investments could be doing more work for you, stick around for some tips you can use to escape your annuity contract. Ideally, you can do this without dealing with a hefty surrender charge.

Compare Investment Advisors

Compare the services, fees, and features of the leading investment advisors. Find the best firm for your portfolio.

What type of annuity do you have?

Before we get into the weeds on how to escape unwanted annuity contracts, we should first make sure that we know what type of annuity we’re dealing with. There are several ways to classify annuities:

- Growth type or risk

- Payout timeline

- Payout duration

Let’s take a look at each of these classifications in more detail so you know exactly the kind of annuity you have.

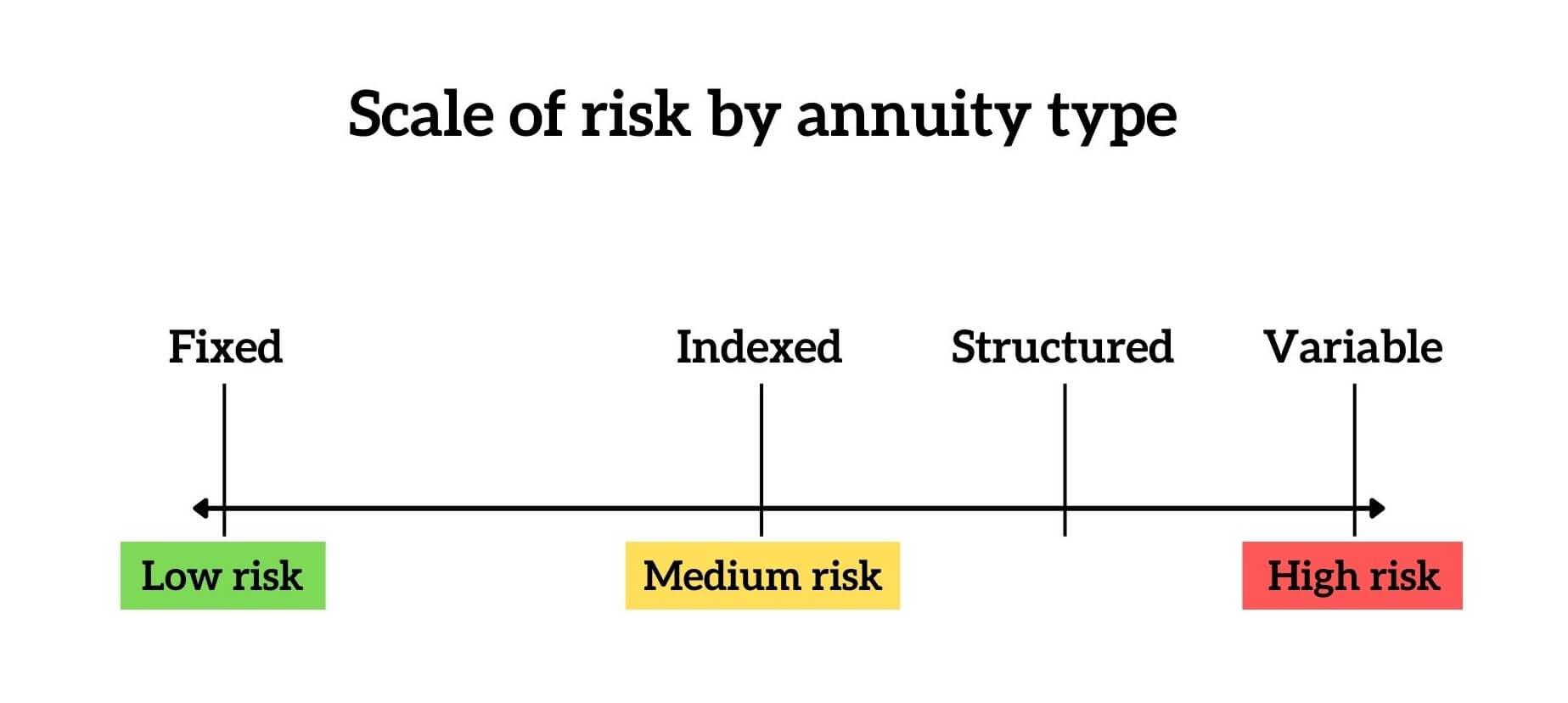

By growth type (a.k.a. risk)

Fixed annuities

A fixed annuity contract is one in which the interest rate is set and will not change over the course of the annuity. This is the safest type of annuity because it offers a guaranteed income stream. However, they also offer the least potential for growth. The reason an insurance company is willing to offer you a fixed, consistent rate is that they’re confident they’re not going to go bankrupt on it.

Fixed-rate annuities are great if the market is unstable because you know that no matter what happens your income or return will remain steady. However, if you purchased a fixed annuity and the market soars, you may end up feeling like you’re losing out on opportunity (because, in a real sense, you are).

Indexed annuities

Rather than setting a fixed rate at the outset of your annuity, fixed indexed annuities — also known as equity-indexed annuities or structured annuities — tie your growth rate to that of a particular market index (e.g. the S&P 500). These annuities protect against some losses if the market tanks, but they also cap your gains if the market is thriving.

These are a nice middle ground in terms of overall risk. You have the potential to earn more and are protected from the worst in the event of a market crash. However, in times of rapid market growth, you may feel like you’re losing out on the gains you could be making.

Structured annuities

A relatively new option inside the annuity universe is a structured annuity (sometimes called a structure variable annuity, or structured index annuity). It’s a blend of a variable annuity and a fixed index annuity.

Structured annuities generally give the investor a choice of duration of the crediting period (usually one, three, or six years) and a choice of indexes (you can normally allocate to multiple indexes). They also come with a performance cap and downside protection through buffers and floors (or guards). This can provide more upside potential than a fixed indexed annuity and more downside protection than a variable annuity.

Variable annuities

A variable annuity is the most volatile of the lot, but it also offers you the most potential for cashing out big. Your gains in a variable annuity are tied to a sub-account that operates much in the same way as mutual funds. So, if the account performs well, you’ll get paid more, but if it loses money, your payments drop as well.

Variable annuities usually don’t offer much in the way of protection if the market crashes. This means if you purchased a variable annuity and you’re watching the balance shrink as markets tumble, you may very well be looking for a way to recoup what money you have left and reinvest it somewhere a little safer.

By payout timeline

- Immediate annuities. Also known as income annuities, immediate annuities begin payments anytime within a year of your purchase. These tend to be funded by retirement accounts, and are a common way for people to retire while still maintaining consistent monthly income.

- Deferred annuities. If you don’t need payments immediately, a deferred income annuity allows your investment to continue growing until a specific point in the future. You may purchase a deferred annuity while still working, or upon retirement, if you know you won’t need the additional income for some time.

By payment duration

- Lifetime annuities. These are annuities that pay you a fixed amount monthly for as long as you live. As you might expect, the longer you’re expected to live, the lower the payments will be.

- Fixed-period annuities. These annuities pay you a set amount for a fixed period of time, typically 20 or 30 years. In this way, your health or presumed longevity will not impact the amount you receive.

How much does it cost to surrender an annuity?

This depends on the annuity contract in which you find yourself. Most annuities have a surrender period that lasts a number of years after you purchase the annuity, during which you will incur surrender charges if you sell or replace your annuity.

Annuity contracts are complicated, but the law requires that you be made aware of the surrender period and fees associated with breaking it before you sign a contract. Make sure you feel comfortable with the details of your annuity contract before you purchase it.

The cost of deciding to cash out your annuity early may also change depending on which state you live in, as each has a different tax code. The IRS assesses a 10% penalty in addition to the increase in taxable income when you receive your lump sum.

Pro Tip

If you’re not sure whether getting an annuity is the right move for you, check out our helpful guide to deciding between a lump sum and an annuity here.

Escaping your annuity contract

Whatever the reason for why you want to get out of your annuity, you will always be able to do so. Unfortunately, the contract you sign will likely have provisions that assess fees if you break it.

There are a few circumstances, however, that will allow you to surrender your annuity without losing a chunk of your money. If you’re wondering how to get out of an annuity without incurring a hefty surrender charge, here are a few options.

Take advantage of your free look period

Ideally, you do your homework before purchasing an annuity, which probably means consulting with a certified financial planner or financial advisor. If, however, despite your best efforts, you find yourself with annuity buyer’s remorse, you might just be in luck.

Most annuities come with a free look period, which allows you to cancel your annuity contract within a certain time period (usually 10 to 30 days) with no penalties.

Related reading: Not convinced that seeking professional help for retirement planning is the right move? Allow us to make the case for why it matters.

Replace your annuity with another one

If you find that your existing annuity just isn’t giving you the investment performance you thought it would, it’s possible for you to transfer from one insurance company to another. In fact, an insurance company may even offer incentives to get you to switch to their services. One annuity contract is certainly not like all others, so it may be worth investigating if you could be earning more somewhere else.

Be wary, however, as you may be assessed surrender fees, which could outweigh any benefits the company may have advertised. What’s more, depending on where you live, you may end up being taxed on the money you transfer from one annuity to another. As always, the best practice is to speak with your certified financial planner or financial advisor before making the decision to replace your annuity.

If, however, you’re feeling independent, here are some thoughts to consider before making the choice to swap annuities:

- Will your new annuity offer you a better interest rate than the old one?

- Is there more or less risk associated with your new annuity?

- Will your new annuity cost you more (i.e. are there more charges or expenses associated with maintaining the account)?

- Are the surrender charges more or less for your new annuity? How long does it take for them to decrease or go away completely?

- Does your new annuity have a guaranteed interest rate? Is it better or worse than the one you already have?

You can also bring these questions to an investment advisor, who may offer better insight on your current investment and alternative options.

Take your money and run

If your free look period is over and replacing your annuity contract isn’t the right move for you, you can always simply cash out. Keep in mind, however, that doing so can result in a surrender charge from your original financial institution.

You may also be assessed taxes on the cash you receive when you cancel your annuity. Many annuities are tax-deferred, which means the money isn’t taxed when you invest it. Alas, there’s nothing that is free, and this isn’t a sneaky way to get out of paying Uncle Sam his due.

When you receive a lump sum from canceling an annuity, that income gets counted for tax purposes. This is before you get into any penalties that may be assessed from canceling an annuity early. The IRS assesses a penalty of 10% of the amount withdrawn if you withdraw from your annuity before you turn 59.5.

Because of all the fees associated with cashing out early, it’s rarely the “best” choice to make when considering your life-long financial situation. Of course, some situations require you to make difficult choices. Just like when purchasing stocks, or any investing for that matter, you should consult a professional before making these choices by yourself.

Key Takeaways

- You can get your money out of an annuity contract if you want or need to.

- It probably won’t be free to get your money out. If you do so before your surrender period is over, you will incur surrender charges and potentially taxes and penalties.

- If you’re unhappy with the income provided by your annuity, you can cancel it or switch to a new provider. However, both options can result in a surrender charge.

- If you’re seriously considering canceling your annuity contract, discuss the potential benefits and consequences with your financial advisor.

BC

Ben Coleman is a veteran English teacher with a knack for translating complex concepts into bite-sized chunks. Having recently dug himself out of crippling credit card debt, he's passionate about providing excellent financial resources to folks who need them so they don't end up in the same position. Ben writes for SuperMoney from Rochester, NY where he lives with his wife and dogs (Yoshi and Pig).

Share this post: