How Marriage and Credit Scores Are Related

Summary:

Marriage doesn’t directly impact your credit score, meaning you’re unlikely to see a change as soon as you tie the knot. However, even though you and your partner won’t share a credit report or score, there are some ways that marriage can affect your credit, both for good and bad.

It’s no surprise that marriage can have some major financial implications. You’re often combining your finances with another person and are taking on shared expenses and (hopefully) shared financial goals.

But how does marriage affect your credit score? In this article, we’ll explain what happens to your credit score when you get married, the ways that marriage can affect your credit score, and how to navigate some of the challenges that can arise from the relationship between marriage and your credit score.

Compare Credit Repair Services

Compare multiple vetted providers. Discover your best option.

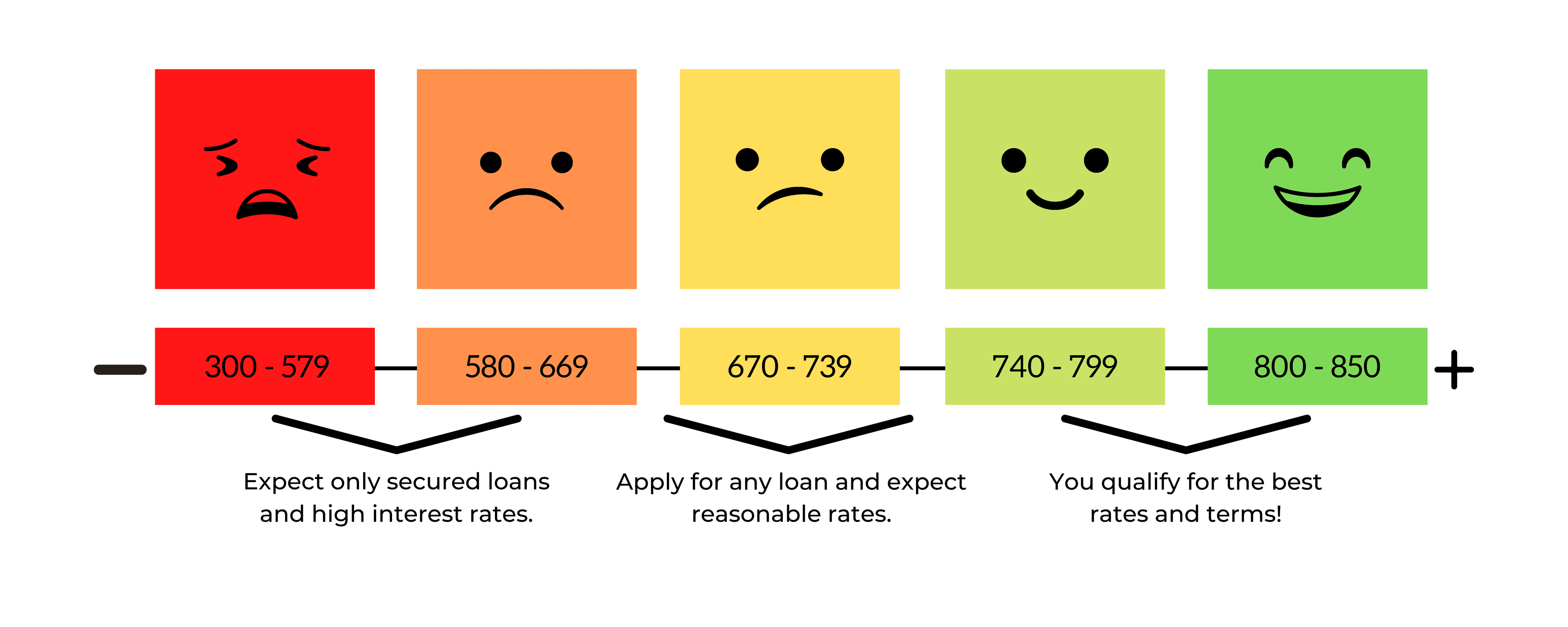

How credit scores work

Before we dive into the relationship between marriage and credit scores, we should first discuss just how credit scores work. Your credit score is essentially a grade from the three major credit bureaus — Equifax, Experian, and TransUnion — that rates how well you use credit.

Your credit score is based on a variety of factors. This includes your debt payment history, the amount of available credit you use, the length of your credit history, the types of credit on your credit report, and any new inquiries on your report.

Your credit score then determines how easily you can qualify for new debt and the interest rates you might be eligible for. Additionally, it can affect your ability to rent an apartment, sign up for an insurance policy, or even get a job.

What happens to your credit score when you get married

There are plenty of myths out there about the effect marriage can have on your credit report. Some people claim there’s a direct impact on your credit score when you get married, while others even believe you and your spouse get a joint credit score when you get married.

In reality, marriage itself has no direct impact on your credit score. Once you’re legally married, you and your spouse will retain your separate credit reports and credit scores. If you change your last name, your new name will appear on your credit report, but will also not affect your score. Your scores won’t directly affect one another, nor will you get a joint credit report or score.

That being said, just because getting married doesn’t directly affect your credit score doesn’t mean there are no impacts whatsoever. If you worry about the potential impacts marriage could have on you or your spouse’s credit score, consider using a credit monitoring service.

Marrying someone with bad credit

One of the biggest concerns some people have is marrying someone with bad credit. It’s easy to understand why this is the case — if you’ve worked hard to build a good credit score, you don’t want it negatively affected simply because of your spouse’s poor credit.

As we mentioned, your partner’s credit score doesn’t directly affect yours. So if you have a credit score of 800 and the person you’re marrying has a score of 500, you’ll both maintain those respective scores after you tie the knot.

That being said, there could be some negative implications of marrying someone with poor credit, especially when it comes to applying for loans and credit together. In most cases, lenders use the lowest of the two credit scores when determining the interest rate you’re eligible for. So if your spouse has a score that’s considerably lower than yours, you may struggle to get a good interest rate on a joint account.

Another implication of marrying someone with poor credit is you may have to cosign for them to qualify for debt. For example, if your spouse wants to buy a car and doesn’t qualify for a loan based on their credit score, you may have to cosign the loan for them to be approved. As a result, this new loan will appear on your credit report.

Pro Tip

Cosigning someone else’s debt comes with major financial implications. If they fail to make their debt payments, your credit score will be harmed and you’ll be on the hook for their debt. Proceed with caution before cosigning debt for anyone, even your spouse.

Shared debt and credit scores

We’ve talked a bit about the relationship between shared debt and credit scores, but let’s dive into that topic a bit more. When you apply for new debt as a couple, lenders often use the lowest of the two credit scores to determine the interest rate. However, if one borrower has a good credit score, the other’s less-than-desirable credit may not affect your ability to qualify for a loan at all.

Once you’ve opened a new joint debt account, it will appear on both of your credit scores as a new account. The payment history and usage will also appear on both credit reports.

If you are planning to finance a purchase it can make sense to get a joint loan as coborrowers. That way the spouse with the lowest credit can benefit from the boost of paying off a loan they might not have qualified for on their own. Here are some lenders that offer joint personal loans.

Impact of joint accounts

It’s important to note that while the same information will appear on both credit reports, it may not have an identical impact on both because there are likely other differences in your credit histories.

In general, someone with a higher credit score will notice a larger impact for negative marks on their credit report, but a smaller impact for paying their bills on time or having another account with low credit utilization. On the other hand, someone who has a poor credit score may experience a larger boost in their credit if they make consistent payments and keep a low balance on their new debt together.

Remember that when you open a joint credit account with someone else, you’re both equally responsible for the payments. If you have a missed payment or delinquent account, it will affect both of your credit scores.

Also, remember that you don’t have to apply for debt together. You can open a credit card or take out a loan in only your name, and so can your spouse. And while the payments may be made from a joint account — if you have one — only the person whose name is on the account will see their credit score impacted.

Looking for the best personal loans tailored for married couples? Discover how joint loans can boost your borrowing power and help you achieve shared financial goals. Learn more in our comprehensive guide: Best Personal Loans for Married Couples.

Increasing your credit scores as a couple

When you get married, you and your spouse become a team. And you can use that to your advantage in many ways, including as it relates to your credit scores. There are several things that married couples can do to help each other boost their credit scores.

One way married couples can do this is by adding one another as authorized users on their credit cards. When you’re added as an authorized user to someone else’s credit card, you get credit for the payment history and credit utilization. If one spouse has a solid credit history and the other person’s is rather thin, this can provide a major credit score boost to the person with a limited credit file.

Pro Tip

When you add someone as an authorized user on your credit card, they often get a copy of the card to use. If your spouse has a history of irresponsible credit use and you choose to add them as an authorized user on your card, consider not giving them access to the card.

FAQs

What happens to your credit score when you get married?

There are no changes to your credit score solely from getting married. However, the way you handle debt in your marriage could certainly affect both of your credit scores.

Does my credit score affect my wife’s?

No, your credit score doesn’t directly affect your wife’s. The only way you could impact your wife’s credit score is in the way you use credit that she’s listed as an account holder for.

Do credit scores merge when you get married?

No, contrary to popular belief, your credit scores don’t merge when you get married.

How are credit scores calculated for married couples?

Credit scores for married individuals are calculated the same way they are for everyone else. Because there’s no such thing as joint credit histories, it’s only the information on your personal credit report that affects your credit score.

Key Takeaways

- Credit scores are a grade from the major credit bureaus that reflects how responsibly you use credit and pay off debt.

- Marriage doesn’t directly impact your credit score, and your credit scores don’t merge with your spouse’s credit score when you get married.

- Marriage can still affect your credit score in other ways, especially if you and your spouse apply for joint credit accounts.

- Sharing joint accounts with someone who is irresponsible with credit can harm your credit score. That being said, you and your spouse can also help to boost each other’s credit scores.

Erin Gobler is a Wisconsin-based personal finance writer with experience writing about mortgages, investing, taxes, personal loans, and insurance. Her work has been published in major outlets, such as SuperMoney, Fox Business, and Time.com.

Share this post:

Table of Contents