Millennial Depression: Why Are Millennials Depressed?

Last updated 03/19/2024 by

Andrew Latham

Depression is one of the most harmful and pervasive conditions among Americans. It is on the rise among all age groups, but particularly among teenagers and young adults. This is leading many to ask, why are Millennials so depressed?

The premise of that question is that Millennials are more likely to be depressed than other age groups. In this report, we review what recent studies have to say about Millennials and depression and look at potential causes.

Get Competing Student Loan Refinancing Offers

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

Are Millennials really more depressed than other age groups?

Millennials — people born from 1981 to 1996 — have been the target of more than their fair share of negative stereotypes. “Experts” have labeled them as snowflakes, narcissistic, entitled, immature, overly sensitive, and lazy. If you follow the news, you are practically guaranteed to see a story every week on how Millennials are the root cause of some undesirable cultural shift, the bane of a beloved tradition, or the death of an entire industry. So is the association of Millennials with depression legitimate?

The quick answer is yes — particularly for younger Millennials — but it’s complicated. A lot depends on how you choose to slice and dice age groups. Let’s take a deep dive into the data.

It’s important to emphasize that this does not prove causation. The odds ratio is a measure of correlation, not causation. But it does raise important questions.

It’s important to emphasize that this does not prove causation. The odds ratio is a measure of correlation, not causation. But it does raise important questions.

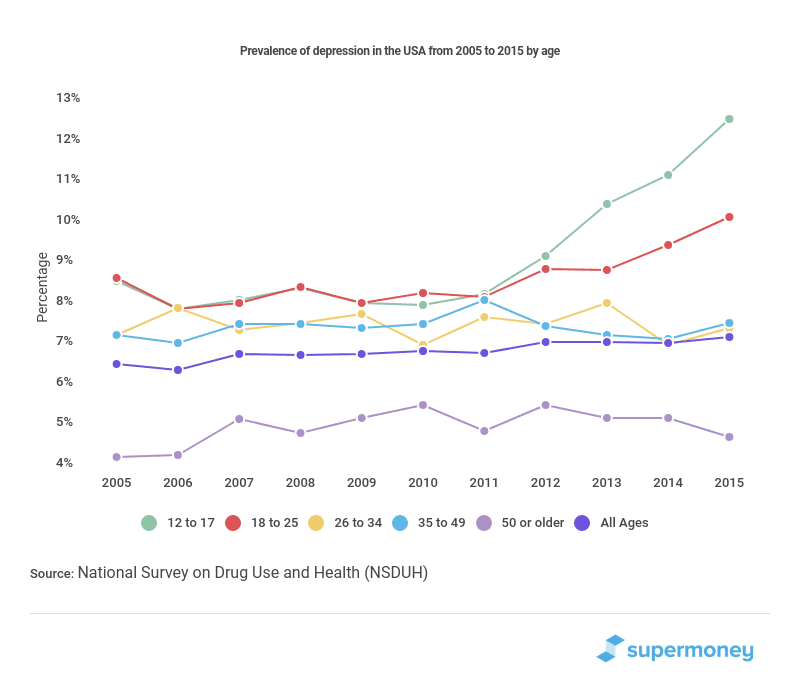

Depression prevalence rates for teenagers and young adults (18-25-year-olds) have grown rapidly in the last decade

The first thing to understand when tackling depression prevalence by age is that depression has been historically higher among teenagers and young adults. So although younger Millennials have higher depression prevalence rates, these drop as they grow older.

To illustrate, consider the data for 2013 in the chart below.

In 2013, Millennials (17 to 33) had significantly higher depression prevalence rates than the average population. In 2015, Millennials had ages ranging from 19 to 35. The rates for teenagers and 18-25-year-olds skyrocketed, but 26-34-year-olds had the same prevalence rates as younger Gen Xers.

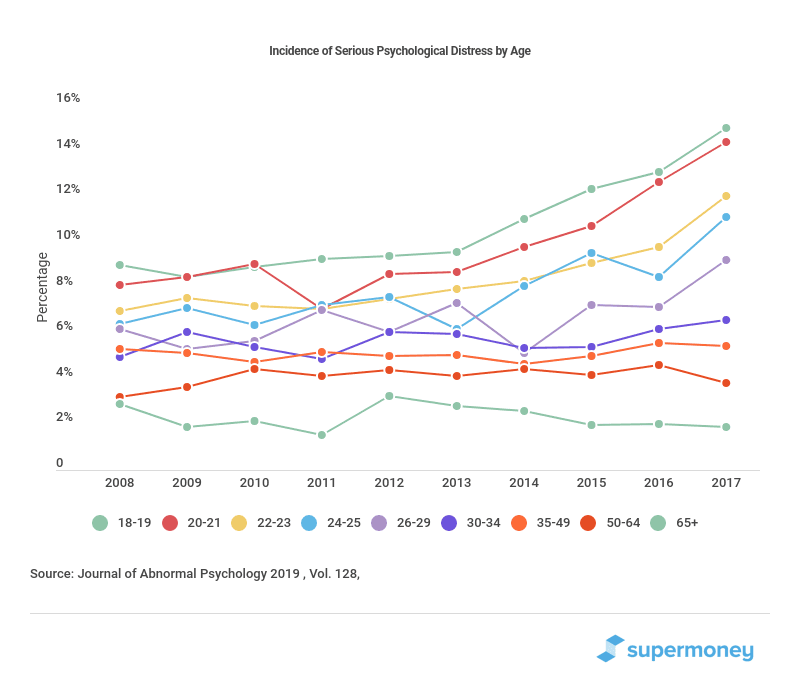

The rate of young adults with mental distress increased by 63% from 2008 to 2017

The percentage of adults reporting mental distress has increased for all age groups but particularly for adults 26 and younger. A 2019 study published in the Journal of Abnormal Psychology reports an increase of 63% in the incidence of serious psychological distress among young adults and a 53% rise for teenagers in the last decade.

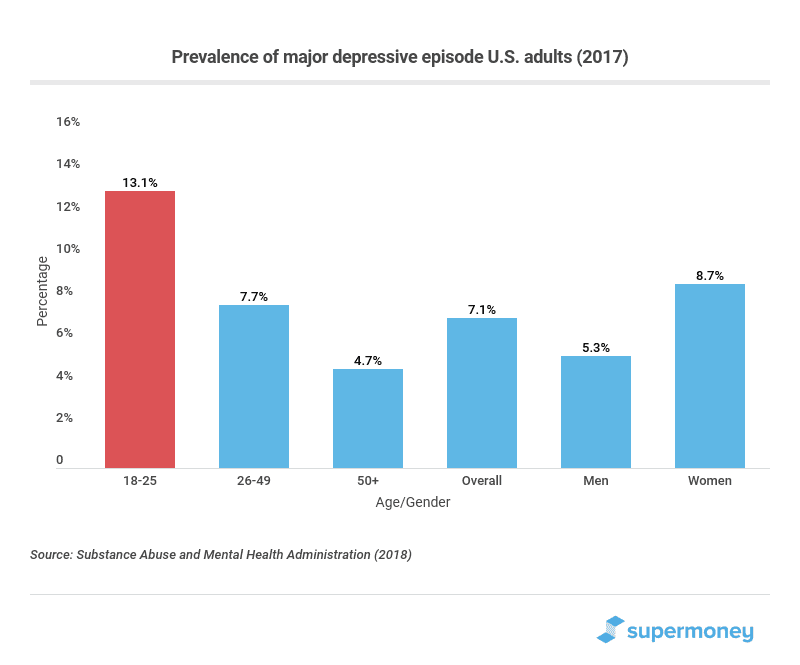

18-25-year-olds had 70% higher prevalence rates for major depression than 26-49-year-olds

Data from the Substance Abuse and Mental Health Administration (SAMHSA) also shows that younger Millennials with ages between 18 and 25 have high prevalence rates of major depressive episodes.

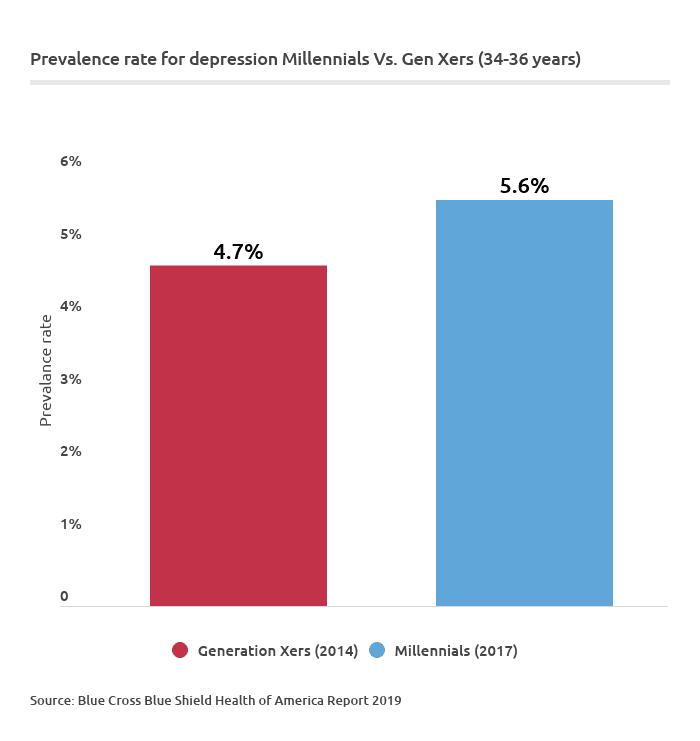

Millennials are more likely to suffer from depression compared to Gen Xers at the same age

The problem with many of these studies is it can be challenging to know which are unique generational traits and what is caused by differences in age, regardless of the generation. A 2019 study by Blue Cross Blue Shield tackled this problem by comparing the prevalence of major depression in Generation X members who were 34-36-years-old in 2014 and Millennials who were 34-36-years old in 2017.

Millennials were 18% more likely to suffer from major depression and had higher chances to have eight of the ten major health conditions the study measured.

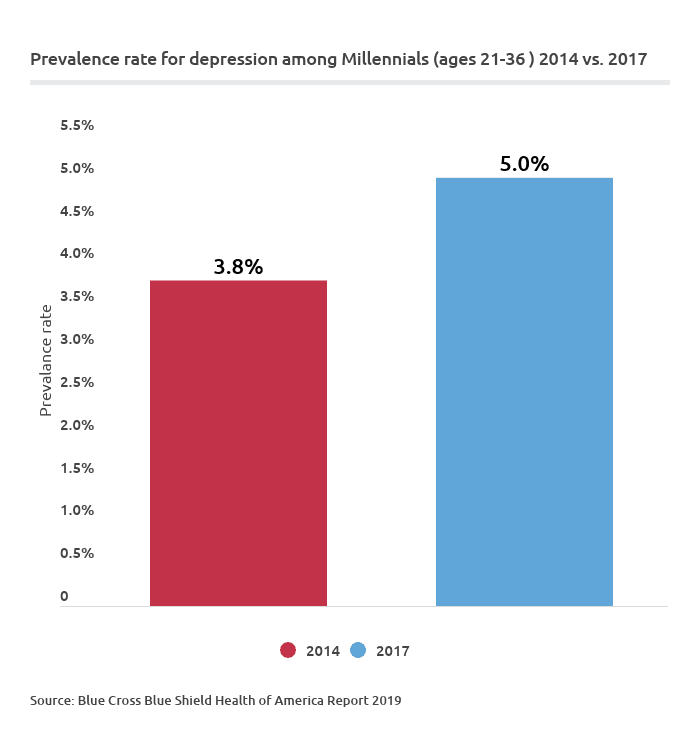

The prevalence of major depression among Millennials increased by 31% within 3 years

The higher prevalence of major depression also holds when you take a wider range of ages. The same report by Blue Cross Blue Shield shows that the increase in the incidence of major depression is accelerating. In 2014, the rate was 3.8%, and in 2017 it climbed to 5.0.%. That is a 31% increase (source).

The rapid increase in major depression rates among Millennials is terrifying, particularly when you consider mortality rates. Between 2008 and 2016, mortality rates among young adults between 25 and 34 years old increased by more than 20%, according to a 2019 report by the Stanford Center on Poverty and Inequality. The leading cause of the increase were suicides and drug overdoses.

So, why are Millennials more depressed than previous generations?

It’s not just that Millennials are more depressed than other generations at their age. What’s even scarier is that Millennial depression rates are growing fast. Why is this happening?

There isn’t a neat narrative that answers these questions. However, multiple studies have shown a strong correlation between depression and financial security. For instance, researchers from the University of South Hampton carried a meta-analysis of pooled odds (a measure of correlation) on the relationship between personal unsecured debt and mental health. They examined 65 studies and found an odds ratio of 3.24 for mental disorders in general and 2.77 for depression. In plain English, this means your odds of having depression if you’re in debt were 277% higher than if you weren’t.

Of course, financial insecurity is just one potential cause for the increase in depression among young adults. Some experts, such as Jean M. Twenge from San Diego State University and A. Bell Cooper from Lynn University, don’t think financial reasons are a significant factor in the rise of depression incidence rates among younger adults during the last decade (source). They point out that this growth has occurred during a period of economic expansion and falling unemployment. However, as we discuss below, economic growth has not benefited all age groups equally.

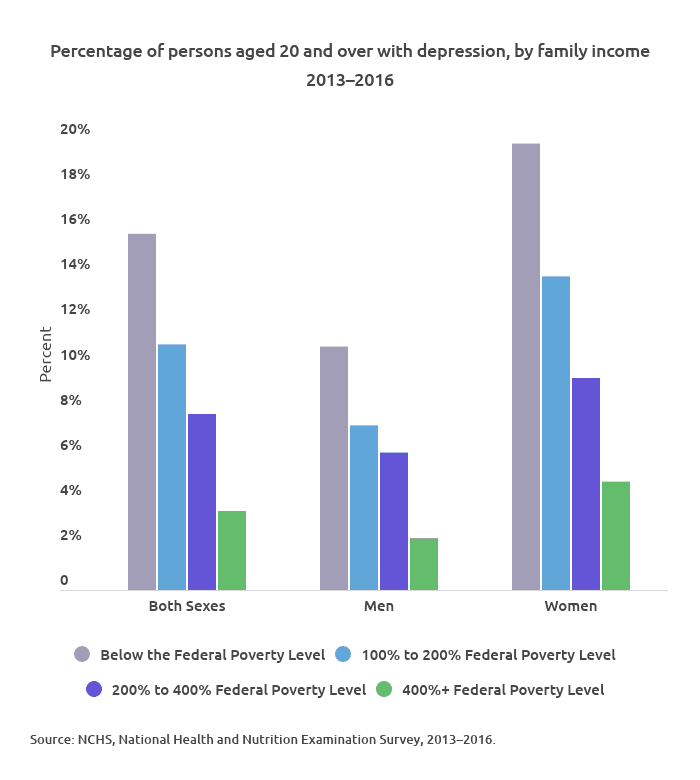

Financial security and depression

Data from the National Health and Nutrition Examination Survey shows a strong correlation between depression rates and financial security. The prevalence of depression decreased as family income levels increased. People with family incomes below the Federal Poverty Level (FPL) had a depression prevalence rate that was more than 4.5 times higher than people with family incomes that were 400% of the FPL. This ratio held for men (4.7) and women (4.125).

Whether financial circumstances are a causal factor in the rise of depression rates for Millennials is still unclear, but depression rates have grown inline with harsh economic conditions.

Millennials have faced the worst macroeconomic conditions we have seen in decades. Their introduction to the job market occurred in the middle of the Great Recession, and they are dealing with rising inequality, a drop in economic mobility, lower salaries, unaffordable housing, and higher education costs. Let’s have a look at some of these economic factors from the perspective of Millennials.

Millennials, housing, and income growth

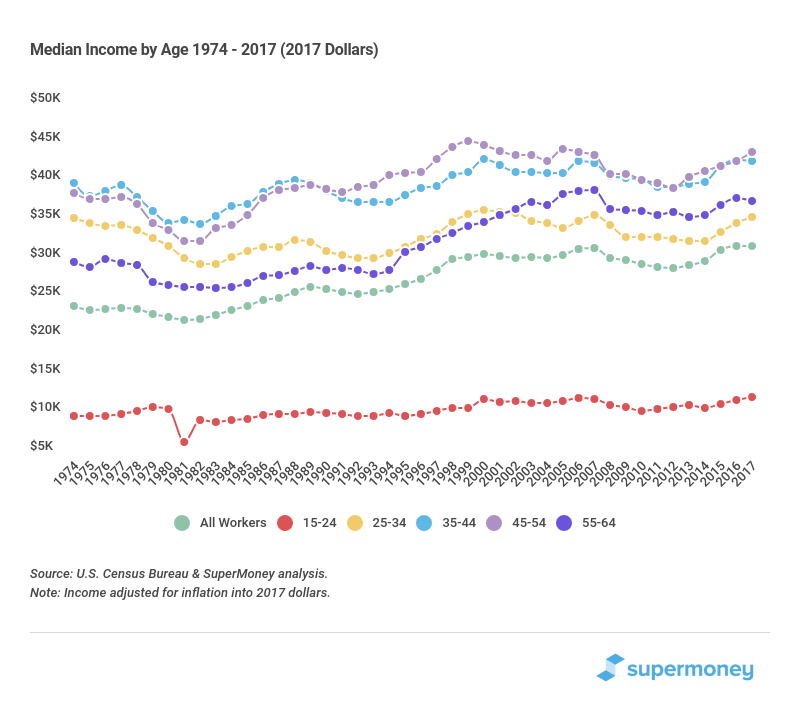

Millennials have been accused of killing the real estate market because they are less interested in buying a home. Although it is true they are buying fewer houses than previous generations, the demand for homeownership is there. The problem is they can’t afford to buy them. Income growth in the last 45 years has been modest among all age groups, but adults with ages between 25 and 34 only make $29 more today than in 1974 if you take into account inflation.

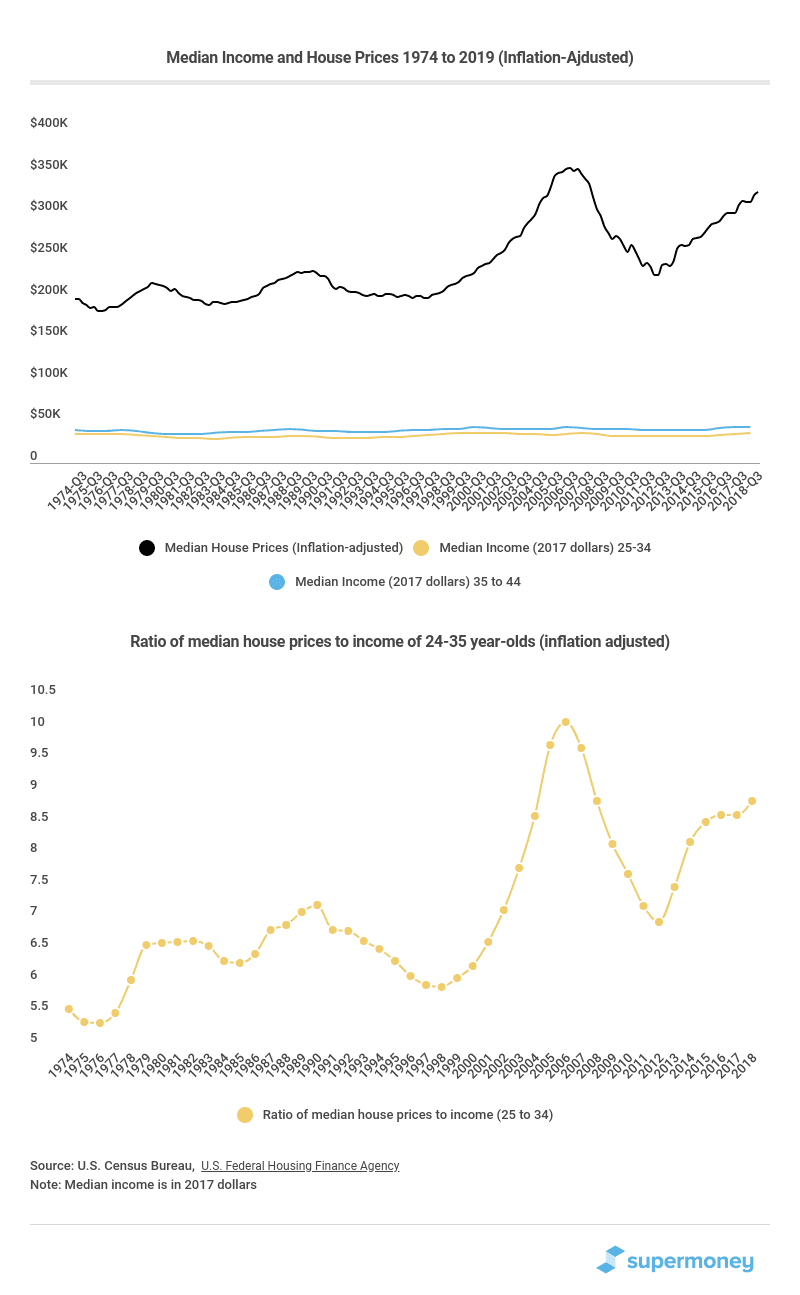

Now consider the median house prices (inflation-adjusted), which have increased from $197,300 (1974) to $325,200. The ratio of median house prices to the income of 24-35 year-olds has increased from 5.57 to 8.86.

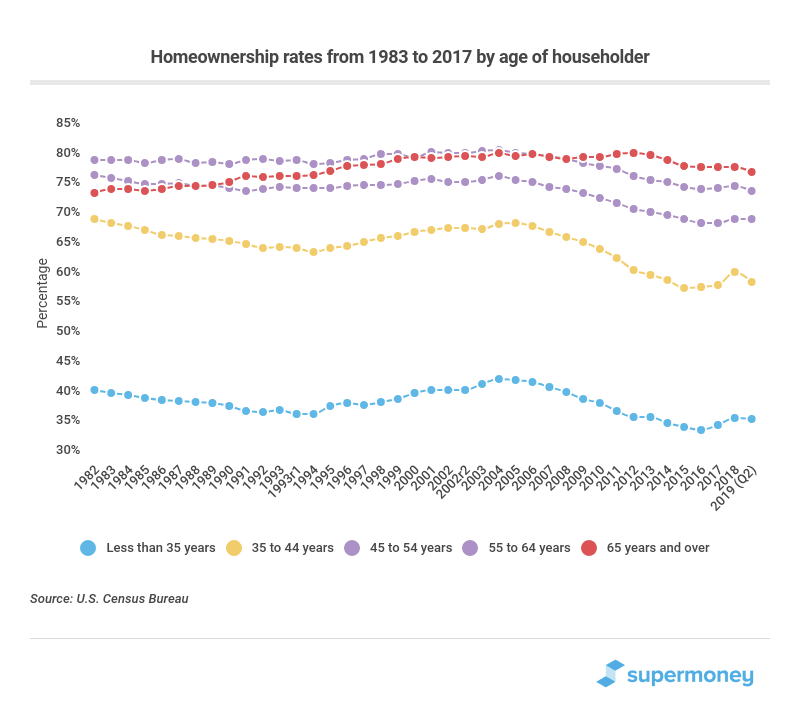

When you consider that the income of young adults has stagnated and housing prices have increased by 165% since 1974, it is no surprise Millennials are buying fewer homes. The Great Recession hurt all age groups, but particularly Millennials. The young-adult homeownership rate is lower for Millennials than for any other generation.

The truth is Millennials have similar consumption tastes to older generations; they just have less money to spend on them. For example, a recent study by Zillow showed that Millennials are taking longer to get married and have kids. Still, they are the largest generation of home buyers, and they’re nearly as likely as older generations to buy a condo in the suburbs and get an SUV.

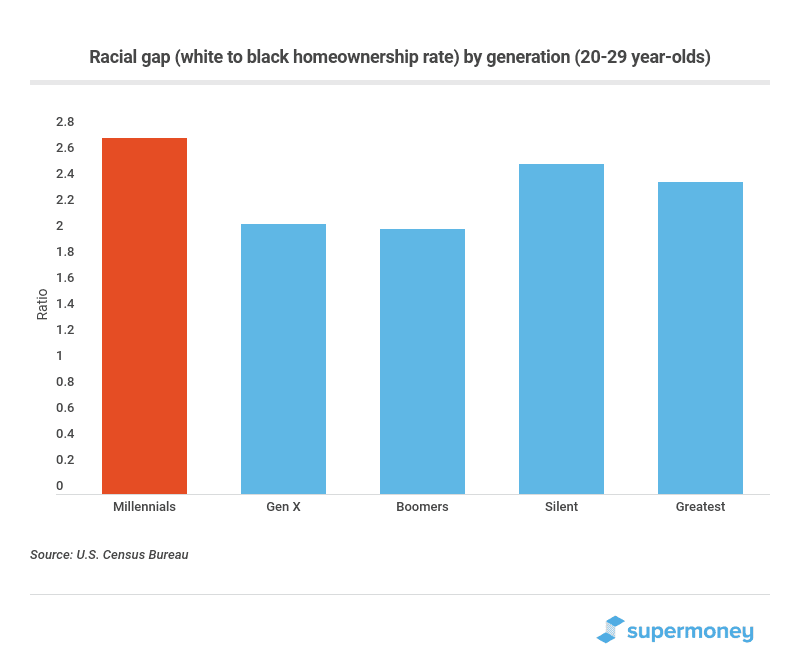

The racial inequality in homeownership rates is higher for Millennials than for any generation since WWII

Shockingly, the racial divide in homeownership for Millennials is higher than in any other generation since the Greatest Generation, which includes people born between 1901 and 1927. The graph below shows the racial gap between white and black homeownership rates for people with ages between 20 and 29 for each generation.

This rise in inequality and a decline in economic mobility make it harder for Millennials, particularly those from minorities, to attain financial security.

Millennials and access to healthcare

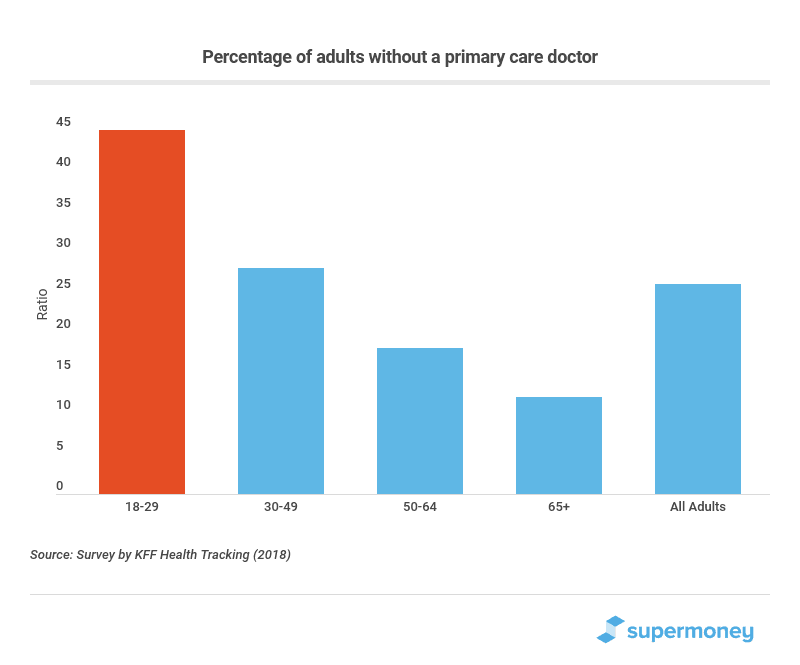

Not surprisingly, they stress about money. According to a recent survey by the Economic Innovation Group, 74% of Millennials worry about being able to afford unexpected healthcare bills, and 79% worry about having enough money to live on in retirement. A 2017 survey by the Employee Benefit Research Institute reported that 33% of Millennials didn’t have a regular doctor (source). In contrast, only 15% of people between the ages of 50 and 64 didn’t have a regular doctor. Concerns about healthcare costs are one of the reasons 45% of people between the ages of 18 to 29 don’t have a primary care provider, according to a 2018 poll by the Kaiser Family Foundation.

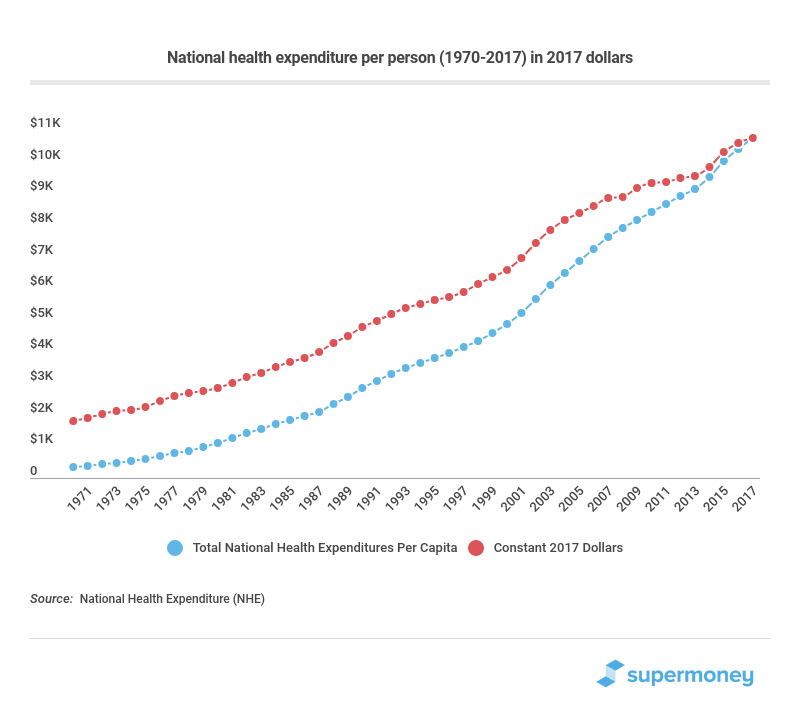

Not having a primary doctor can cause early signals of mental illness to go unnoticed and, therefore, untreated. The concern for medical costs is entirely understandable. National health expenditure per person has grown dramatically, and as we will see, salaries have not kept the pace. Even after allowing for inflation, medical costs per person are more than five times higher than 50 years ago.

Millennials, education, and employment

Millennials have a harder time finding well-paid work than previous generations, particularly in the manufacturing sector. We are witnessing the effects of the U.S. transition from a manufacturing economy to a knowledge-based economy. In previous generations, unskilled workers could get well-paid jobs in the booming manufacturing industry; the demand is not there today. The decline in manufacturing jobs is closely tied to technological advancements in automation. It’s not that the U.S. has stopped building things. The U.S. manufactures more now than it ever has, but a lot is done by machines. Today, the economy puts a higher value on a worker’s knowledge and intellectual capital, which requires time to develop and typically means having a college education.

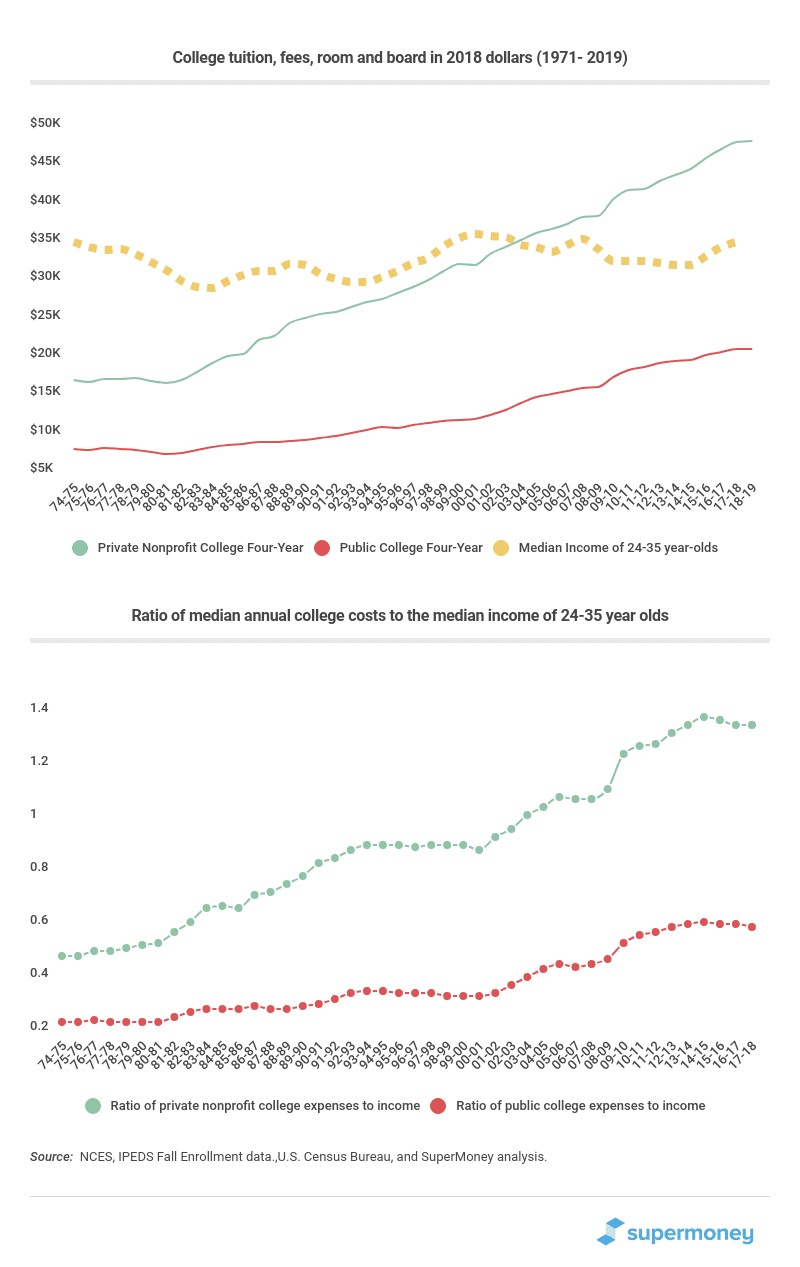

This education that is so vital to attain a well-paid job has never been more expensive. The cost of education has more than doubled. However, incomes have remained stagnant. Look at the ratio of the median cost of attending college and incomes of 24 to 35-year-olds.

Millennials with a bachelor’s degree or higher are earning around $50K, which is more than previous generations even after accounting for inflation. The payoff for attending college is as high as it has ever been. However, that also means the opportunity cost of not getting a higher education has also never been higher. The median income of 25-year-old men who only have a high school degree is $29K a year. That is about $2,600 less than what Generation X made, and nearly $10K less than what Baby Boomers earned at the same age. This increase in inequality arises from higher demand for highly educated workers and a decline in the need for unskilled labor.

Millennials and student loans

Student loan debt is now at $1.5 trillion. According to a recent study by Realtor and American Student Assistance, 85% of Millennials say they can’t save for a down payment because of student loan payments.

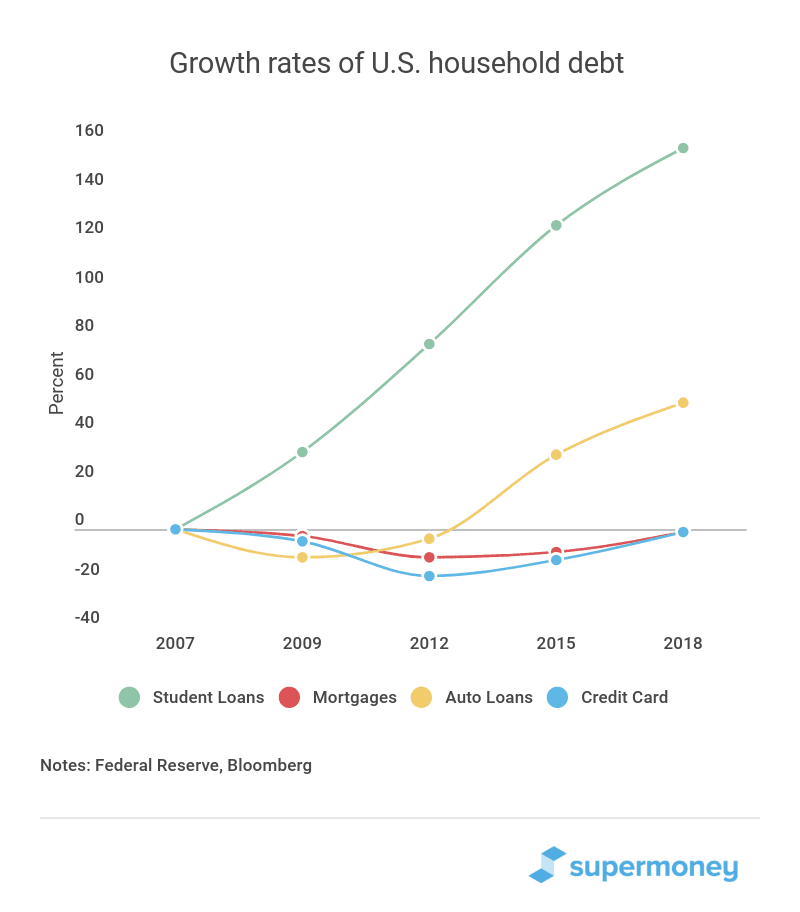

Student loans are the fastest-growing source of debt for U.S. households. Since 2007 it has grown three times faster than auto loans and 150 times more than mortgages. Student loans are now the largest source of unsecured debt in the United States and have become a financial industry in their own right (source).

The average student pays about $24,000 a year (around $96,000 for four years) to go to college. Most households cannot afford to pay that with savings, which is why student loan balances are growing at an unprecedented rate. More than half of families (53%) need loans to pay for their children’s undergraduate education (source).

In summary, there is a strong correlation between financial insecurity and depression prevalence rates. However, correlation is not the same as causation. And other factors have been linked to higher depression rates, such as substance abuse and social media consumption.

Millennials and social media

The use of electronic communication and digital media has grown dramatically in the last decade. Multiple studies have shown that people who spend more time on social media and less time with face-to-face have lower well-being levels and are more likely to be depressed (source). One reason is that an increase in social media consumption can cause younger adults to worry more about peer status. The desire to keep up with your peers affects all age groups, but social media exaggerates that process.

The increase in depression also correlates with a growth in the ownership of smartphones, which started in 2012. The later rise (around 2014) in depression rates among older adults could be caused by a later adoption of smartphones among older age groups (source).

Millennials, the scapegoat generation

It’s typical for Millennials to get the blame for cultural and economic changes. In most cases, their only crime is to behave like everybody else. A classic example is this article by The Wall Street Journal, which practically blamed Millennials for killing grocery stores. The report noted that 25- to 34-year-olds are spending less at traditional grocers than their parents did. However, this is a national trend. Americans of all ages are changing the way they eat and shop. For instance, consumers across the age spectrum are relying more on convenience stores and superstores. We are all eating out more instead of buying food to cook at home. In fact, people over 65 are the demographic that is shifting toward restaurants the fastest.

As I mentioned in the introductions, Millennials also have a reputation for lousy work ethic and not being loyal employees who are always job-hopping. However, research by the Pew Research Institute shows that Millenials are changing jobs just as frequently as Generation X workers did (source). Interestingly, research by the U.S. Travel Association revealed that older Americans take more time off than Millennials (source).

Unfortunately, there are reasons for concern when it comes to Millennials and mental health problems in general and depression in particular.

It’s complicated, but the economic circumstance of Millennials is probably an important factor

Depression is a complex mental health disorder. Doctors can rarely — if ever — explain precisely what causes it. Sometimes, depression has a genetic component. It can also be triggered by a severe medical illness or a life change, such as the death of a loved one, losing a job, or getting divorced.

Therefore, nobody can be sure why Millennials and Gen Z’s are seeing such rapid growth in depression rates. However, multiple studies have established a strong correlation between financial security and mental health disorders like depression. And Millennials have been dealt a tough hand when it comes to employment and income security. Millennials started working during the Great Recession. They are dealing with rising inequality, a drop in economic mobility, less access to primary health care doctors, lower salaries, unaffordable housing, and higher education costs.

So, it wouldn’t be shocking if the anxiety and stress caused by living during some of the worst macroeconomic conditions experienced in decades are partially responsible for the increase in mental health disorders among Millennials.

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

Share this post:

Table of Contents