The Most Popular Financial Resolutions of 2022

AL

Last updated 04/08/2024 by

Andrew LathamSummary:

Most people (seven out of ten, to be precise) have financial resolutions for 2022, but only a few of us will do something to achieve our goals. If you are looking to achieve your financial resolutions this year, here are the three most popular financial resolutions of 2022 (and one resolution that might just help you achieve them all).

‘Tis the season for optimism. That is at least the takeaway you get when you read the 2022 Financial Resolutions Study1 Fidelity just published.

- Six out of 10 Americans feel optimistic about the future despite everything.

- 72% are confident they will be in a better financial position in 2022.

- 68% are considering a financial resolution this year.

All this optimism is refreshing and contagious, but it’s all words unless we put it into action. So, what financial resolutions are you considering this year?

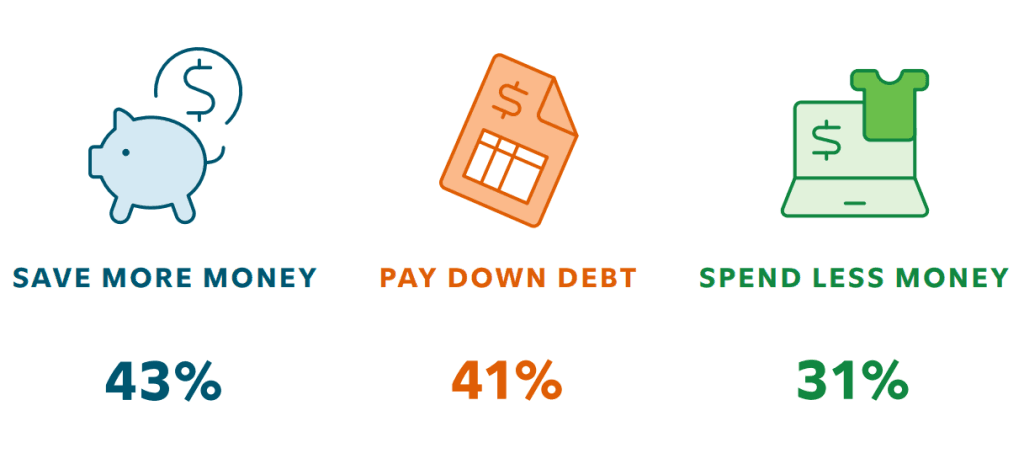

Here are the three most popular financial resolutions according to Fidelity’s study.

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

Save more money

Saving money when you are on a tight budget can be a real challenge. It’s particularly annoying when well-intentioned friends and relatives (and articles like this one) suggest “savings rules” that are not realistic for you. I’m talking about rules like saving 10% or 20% of your monthly salary. Don’t feel discouraged. Decide on your own personal rule to live by that works for your financial situation.

Saving money regularly—even if it’s a small amount—can help you manage unexpected expenses and emergencies and reach your financial goals. However, when it comes to financial resolutions, try to use set-it-and-forget-it strategies, so you never have to think about it again.

Automation is your friend in these cases. Instead of trying to remember every month to save money, set up automated transfers from your checking account to your savings or brokerage account every payroll period. Ideally, you should set up automated transfers as part of your employer’s direct deposit, as this will make it a little more difficult to turn them off. This added friction will make it harder to stop saving when you’re tempted to use the money for non-essential purchases. Even $20 per pay period is an excellent start if you’re currently not saving at all.

If you don’t have a suitable emergency fund start with that. Having enough to cover three months of living expenses if you’re a two-wage family or six if you’re a one-wage household is a good rule of thumb for many households.

Increasing your retirement savings is an excellent goal for families that already have an emergency fund. A superb resolution — if you can afford it — is to max out your tax-advantaged contributions to at least one of your retirement accounts. For a 401(k), that is $20,500 in 2022. SEPs allow you to contribute up to $61,000, and IRAs have a maximum of $6,000 ($7,000 if you are 50 or older). However, this is not realistic for many households.

At the very least, try to match your employer’s contribution match to your 401(k) — if your employer provides it.

Matching contributions are contributions your employer makes to your retirement plan account if you contribute to the plan from your salary. Here are the main tax benefits of matching contributions.

- They don’t count toward your tax-advantaged contribution limit ($20,500 in 2022).

- The money grows tax-free while in the plan.

- You only have to pay taxes when you make withdrawals from the plan.

Another great thing about your 401(k) contributions is they come straight out of your paycheck. It’s automatic. You don’t have to remember to contribute, which increases the likelihood you will actually make those contributions exponentially.

Pay down debt

Your credit card debt is costing you. Here’s a realistic example of how much it costs. The average credit card balance in 2021 was $5,525, according to Experian and the average interest rate for cards with a balance is 17.13% APR (source).

If you pay $200 a month, it will take nearly 3 years (35 months) to pay off and cost you $1,436 in interest. Ouch.

The smartest way to pay off credit card debt when you have multiple accounts is to prioritize the credit card with the highest interest rate and pay the minimum balance on all other accounts regardless of your balance.

If you qualify for a 0% APR balance transfer credit, you can save hundreds of dollars by paying it off during the 0% APR introductory offer. Some credit cards have introductory offers of up to 21 months.

Another great option is to consolidate your high interest debt in a low interest personal loan, a mortgage refinance, or a home equity line of credit.

Spend less money

Saving money isn’t just about willpower and budgeting tricks. It’s about changing your lifestyle. To consistently spend less and save more, you need to change your lifestyle.

Articles like these provide dozens of ideas on how to save money, but I would like to focus on just one — and it doesn’t even require cutting any expenses — track your spending. That’s it. Regardless of your income or how much debt you have, consider tracking every dollar you spend for the next three months.

Keeping a record of all the stuff and services you pay for is a powerful money management tool.

Notice how nutritionists recommend keeping a food diary when you go on a diet (source)? The simple act of tracking your food intake makes it less likely you’ll overeat or binge on unhealthy food.

The same applies to spending. If you don’t track your purchases, you can easily spend hundred dollars a month on stuff you don’t need without even realizing it.

Tracking your spending will provide you with valuable insights into your spending habits. You will quickly spot what triggers impulse spending and find areas where you can save money by cutting unnecessary purchases. When you track your spending, you are also more likely to spot fraudulent activity and less likely to miss a payment, which can help your credit score.

It’s one thing to agree that tracking your monthly expenses is a good idea in theory, but it’s another thing altogether to start doing it. So whether you prefer using pen and paper, fancy spreadsheets, an app, or your online checking account, start tracking today. This is a resolution we can all achieve regardless of our financial situation, and it can help us reach other important goals, such as saving more and paying off debt.

Key takeaways

- Americans are optimistic about the future: 72% are confident they will be in a better financial position in 2022, and 68% are considering a financial resolution this year.

- The three most popular financial resolutions are saving more money, paying down debt, and spending less.

- Saving regularly—even if it’s a small amount—can help you manage unexpected expenses and emergencies and reach your financial goals.

- The smartest way to pay off credit card debt when you have multiple accounts is to prioritize the credit card with the highest interest rate and pay the minimum balance on all other accounts regardless of your balance.

- Consider consolidating your high interest debt into a low interest loan (balance transfers, mortgage refinance, and HELOCs).

- At the very least, try to match your employer’s contribution match to your 401(k)

- Tracking your spending will provide you with valuable insights into your spending habits. You will quickly spot what triggers impulse spending and find areas where you can save money by cutting unnecessary purchases.

AL

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

Share this post: