Personal Loans vs Credit Cards: Things You Should Know

Last updated 09/12/2024 by

Audrey Henderson

Summary:

The main difference between personal loans and credit cards is how the funds are accessed and repaid: personal loans provide a lump sum of money that is repaid over a fixed period with fixed payments, while credit cards offer a revolving line of credit that allows for ongoing borrowing up to a limit, with flexible repayment options and interest charged on outstanding balances.

In either case, you’re faced with the prospect of using credit. But should you take a personal loan or use a credit card to cover that unexpected expense or purchase that costly item? Both options have both advantages and disadvantages. The right answer for you depends on several factors, including your personal financial profile.

In either case, you’re faced with the prospect of using credit. But should you take a personal loan or use a credit card to cover that unexpected expense or purchase that costly item? Both options have both advantages and disadvantages. The right answer for you depends on several factors, including your personal financial profile.Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

Advantages of Credit Cards

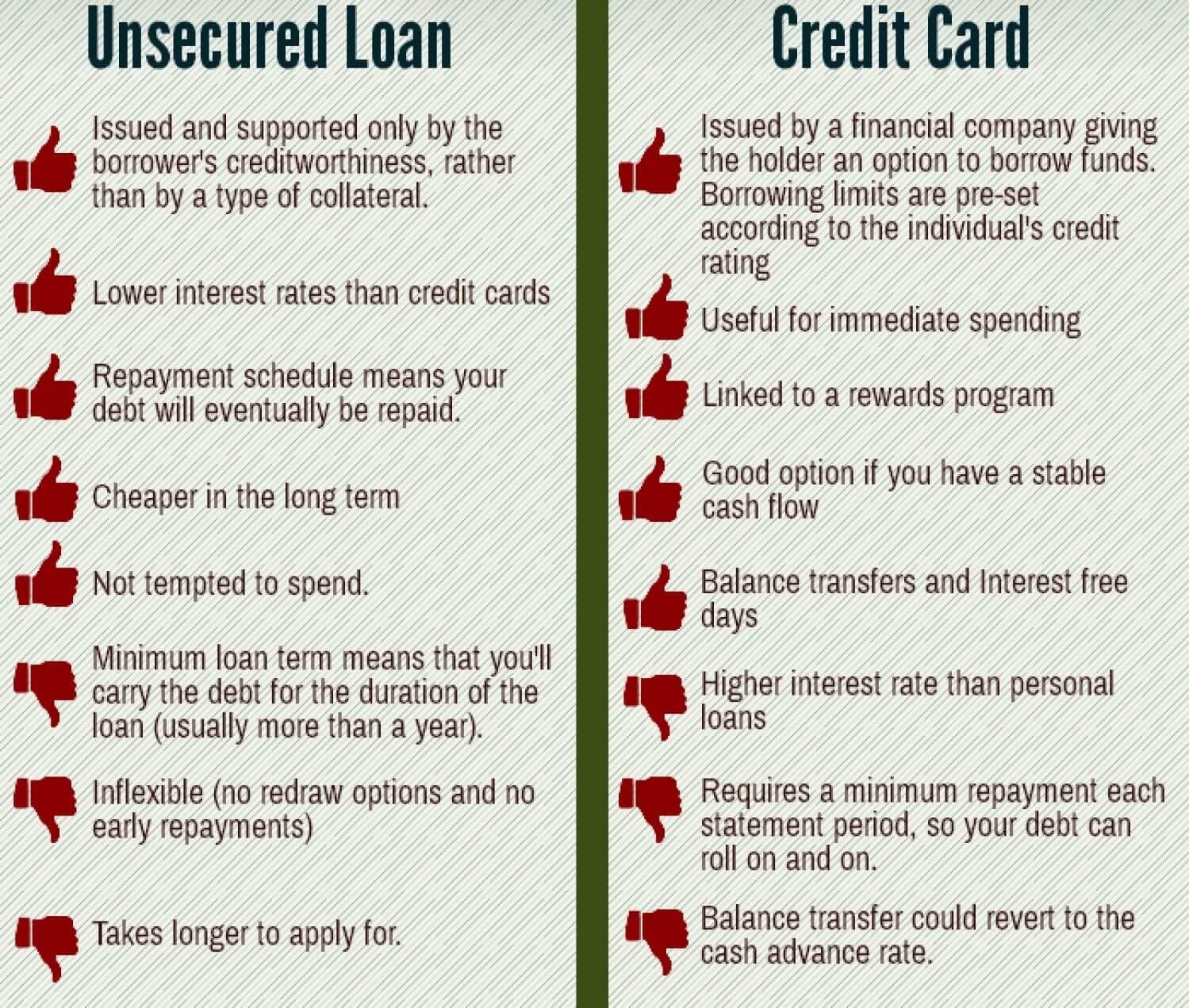

If you have good or excellent credit, you may qualify for a credit card with very low interest or a zero percent APR, which is equivalent to receiving a no-interest loan. Many credit cards offer rewards programs that allow you to earn cash back, score free merchandise or other goodies. Extended warranties and insurance programs are also common credit card perks. Credit card accounts are also protected by law against fraud or unauthorized access. If you’re dissatisfied with a purchase made with a credit card, in many cases you can receive a full refund of your purchase price.

If you have good or excellent credit, you may qualify for a credit card with very low interest or a zero percent APR, which is equivalent to receiving a no-interest loan. Many credit cards offer rewards programs that allow you to earn cash back, score free merchandise or other goodies. Extended warranties and insurance programs are also common credit card perks. Credit card accounts are also protected by law against fraud or unauthorized access. If you’re dissatisfied with a purchase made with a credit card, in many cases you can receive a full refund of your purchase price.Disadvantages of Credit Cards

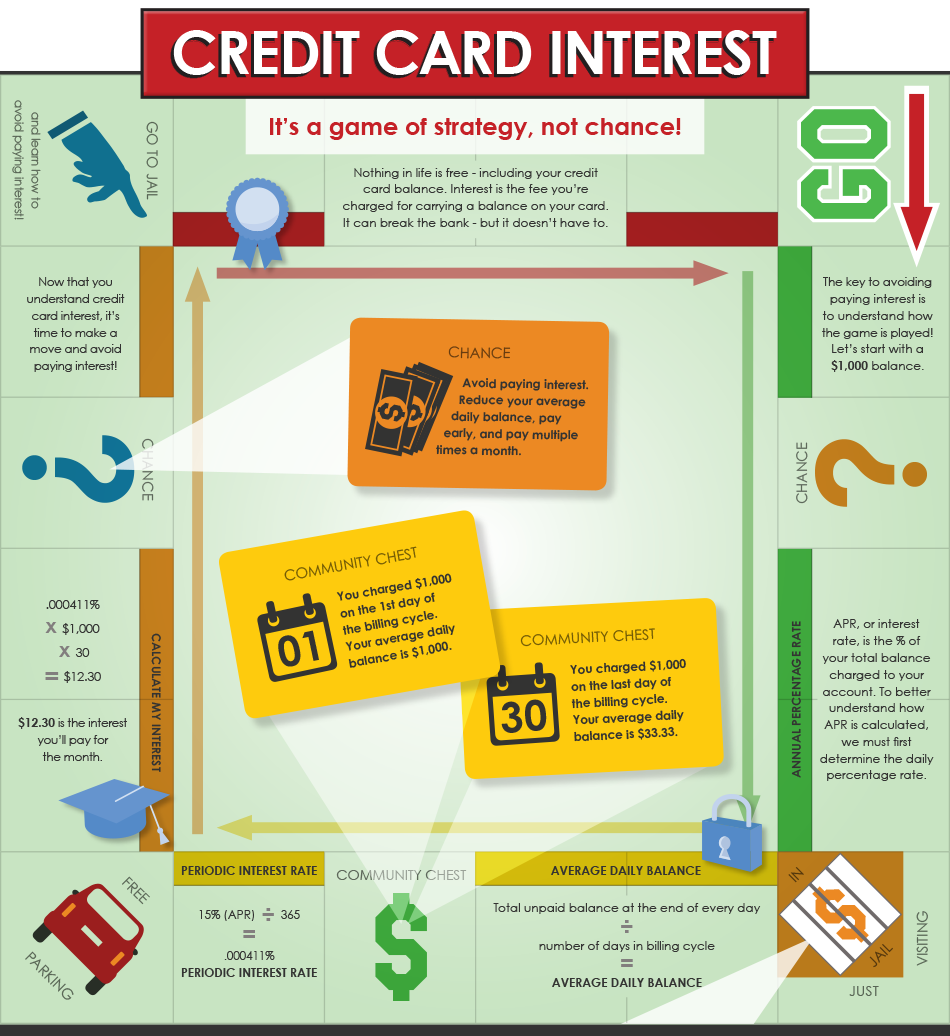

Unlike personal loans, credit cards are considered to be revolving debt. Your monthly payments – and in some instances, your interest rates – vary according to your credit card account balance. If you typically carry a balance on your credit card accounts and only make minimum monthly payments, you could be paying many times the actual cost of your purchases. The 20 dollars you spend on pizza one weekend could eventually cost you hundreds of dollars by the time you pay off your credit card balance.

Unlike personal loans, credit cards are considered to be revolving debt. Your monthly payments – and in some instances, your interest rates – vary according to your credit card account balance. If you typically carry a balance on your credit card accounts and only make minimum monthly payments, you could be paying many times the actual cost of your purchases. The 20 dollars you spend on pizza one weekend could eventually cost you hundreds of dollars by the time you pay off your credit card balance.Many credit cards charge high fees for late payments or for going over the credit limit. Others impose stiff penalty APRs for missed payments that may be permanent. Besides lowering your FICO score, fees and penalty APRs can dramatically increase your debt, which in turn could have a detrimental effect on your credit report and FICO score. And unlike mortgage or student loan interest, credit card payments are not tax deductible.

Advantages of Personal Loans

Most personal loans are available without requiring collateral. Instead, you must demonstrate that you have the ability to repay the loan, usually through a credit check. Personal loans also have fixed interest rates and finite repayment periods, which means that once your repayment period is finished, your loan is repaid in full.

Most personal loans are available without requiring collateral. Instead, you must demonstrate that you have the ability to repay the loan, usually through a credit check. Personal loans also have fixed interest rates and finite repayment periods, which means that once your repayment period is finished, your loan is repaid in full.Your credit utilization ratio, that is, the percentage of your available credit that you’re actually using, counts for 30 percent of your FICO score. Using too much of your available credit can really give your FICO score a hit. Personal loans don’t have an adverse affect on your credit utilization ratio because they are considered to be installment loans rather than revolving credit. Handling a personal loan responsibly can also improve your credit profile and your FICO score.

Disadvantages of Personal Loans

Because they are unsecured, personal loans usually carry higher interest rates than secured loans. You also must usually pass a fairly stringent credit test to qualify for personal loans. If your credit is damaged, you may not qualify for personal loans, or only for loans with very high interest. The wait for personal loans can also be lengthy, which is a disadvantage when you’re facing a financial emergency.

Because they are unsecured, personal loans usually carry higher interest rates than secured loans. You also must usually pass a fairly stringent credit test to qualify for personal loans. If your credit is damaged, you may not qualify for personal loans, or only for loans with very high interest. The wait for personal loans can also be lengthy, which is a disadvantage when you’re facing a financial emergency.Personal loans also don’t provide perks such as zero percent APR or rewards programs. Making a purchase with a personal loan won’t provide you with an extended warranty or insurance unless you purchase them separately. Personal loans also don’t provide a refund option if you’re not satisfied with your purchase. If the merchant doesn’t allow refunds, you’re generally out of luck.

Many payday lenders extend credit to nearly anyone who has an income. Payday loans are also processed within hours or one or two business days. But in exchange for speed and convenience, payday lenders impose triple-digit interest rates and unrealistically short repayment periods that result in an endless cycle where the amounts owed get bigger, not smaller. Payday loans also usually don’t report payments to the three major credit reporting bureaus: TransUnion, Equifax or Experian, so maintaining on-time payments does nothing to improve your credit profile or your FICO score.

When to Use Credit Cards

Using credit cards makes the most sense if you’re faced with a financial emergency. If the transmission goes out on your car and you have no other way to get to work, use your credit card to have your car repaired now, rather than wait three weeks or longer for your bank to approve a loan. Whipping out the plastic to cover concert tickets for your favorite band or that hot new gadget MIGHT be OK, but only if you’re confident you can repay the cost of the transaction in full before interest charges kick in.

Using credit cards makes the most sense if you’re faced with a financial emergency. If the transmission goes out on your car and you have no other way to get to work, use your credit card to have your car repaired now, rather than wait three weeks or longer for your bank to approve a loan. Whipping out the plastic to cover concert tickets for your favorite band or that hot new gadget MIGHT be OK, but only if you’re confident you can repay the cost of the transaction in full before interest charges kick in.When to Use Personal Loans

Personal loans are a better choice when you know you’ll be making payments over time. You can budget a certain amount each month for servicing your debt. Avoid personal loans with prepayment penalties, and be sure that any payments you make that are above the set monthly installment amount are applied to the principle, if possible. Personal loans may also be a better choice for large expenditures such as planned household improvements. Depending on your credit profile and your bank, you may be able to obtain a lower interest rate from a personal loan than from a credit card. This is especially true if you take a credit card advance to obtain cash.

Personal loans are a better choice when you know you’ll be making payments over time. You can budget a certain amount each month for servicing your debt. Avoid personal loans with prepayment penalties, and be sure that any payments you make that are above the set monthly installment amount are applied to the principle, if possible. Personal loans may also be a better choice for large expenditures such as planned household improvements. Depending on your credit profile and your bank, you may be able to obtain a lower interest rate from a personal loan than from a credit card. This is especially true if you take a credit card advance to obtain cash.The Final Verdict

There is no strict formula to determine whether personal loans are better or credit cards are better. Each type of credit has its place in your financial portfolio. Wisely using personal loans and credit cards can improve your overall credit profile, but misusing either credit cards or personal loans can cause serious harm to your financial profile. Your best bet is to use cash as much as possible while relying on credit cards or personal loans only when you really need them, and avoiding payday loans at all costs.

There is no strict formula to determine whether personal loans are better or credit cards are better. Each type of credit has its place in your financial portfolio. Wisely using personal loans and credit cards can improve your overall credit profile, but misusing either credit cards or personal loans can cause serious harm to your financial profile. Your best bet is to use cash as much as possible while relying on credit cards or personal loans only when you really need them, and avoiding payday loans at all costs.Audrey Henderson is a Chicagoland-based writer and researcher. She holds advanced degrees in sociology and law from Northwestern University. Her writing specialties are sustainable development in the built environment, policy related to arts and popular culture, socially and ecologically responsible travel, civic tech and personal finance.

Share this post:

AddTable of Contents