How to Remove a Tax Lien from Credit Reports and Public Records

Last updated 03/19/2024 by

Andrew Latham

Tax liens are the nuclear option in the IRS’s arsenal. They can affect all your property, including your home and vehicles. Even financial assets and businesses that you might own are not safe. Also, they can attach to assets that you buy once the IRS issues the demand for payment. The good news is that tax liens no longer appear on your credit report. Unfortunately, that doesn’t mean a tax lien doesn’t hurt your chances of accessing credit.

Tax liens no longer appear on credit reports

There was a time when a state or federal tax notice would appear on your credit reports and could lower your credit score by as much as 100 points. They would stay on your credit report for up to seven years. Even paying off all of your tax liens wouldn’t get the lien removed from your credit report. Credit bureaus were not required to remove them until they expired.

Having tax liens on your credit report could prevent you from qualifying for a credit card, personal loan, or mortgage. Even now, having a tax lien can stop you from getting a job. In the financial and tax administration sectors, for example, you can get disqualified from certain professional jobs or licenses (e.g., realtor and financial advisor licenses) if you have a tax lien.

In 2018, all three credit bureaus stopped collecting and removed all information on tax liens from credit reports

So, state and federal tax liens no longer appear on your credit reports. However, they are a matter of public record and can still affect your chances of getting approved for a loan or a job regardless of credit reporting changes. The good news is you can remove your tax lien from the public record. This is done with a withdrawal of Notice of Federal Tax Lien.

A tax lien can still harm your chances of qualifying for a job or getting a mortgage, credit card, or personal loan if it appears on public records.

Although it is no longer necessary to remove a tax lien from your credit report, this article will provide detailed instructions on how to remove a tax lien from your public records. But, first, let’s start with some basics.

What is a tax lien?

A federal tax lien is the government’s legal claim against your property when you neglect or fail to pay a tax debt. The claim protects the government’s interest in all your property, including real estate, personal property, and financial assets. This hold on your property exists when the IRS puts your balance due on the books, sends you a bill that explains how much you owe (Notice and Demand for Payment), and then sees that you neglect or refuse to fully pay the debt in time.

What is a tax lien notice?

The IRS uses tax lien notices to inform current and future creditors that they have dibs on whatever property a delinquent taxpayer owns.

For example, in 2014, singer Vanessa Williams incurred a federal tax lien on all her property for $369,249.89 in unpaid income tax. The IRS then filed a tax lien notice at the New York County register office, which made the lien public. In Vanessa Williams’ case, the lien was only for one tax liability, income tax for the 2011 financial year. However, a tax lien notice could include up to 15 different tax liabilities.

Note that tax levies are different from federal tax liens. A lien is a legal claim against your property to secure payment of your debt for unpaid taxes, while a levy actually takes the property to satisfy the debt. A levy is a legal seizure of your property to satisfy a tax debt. The rest of this article discusses how you could remove a tax lien, not avoid a tax levy.

Why should you remove a tax lien notice from public records?

When you apply for a credit card, a mortgage, a car loan, a student loan, or any other type of credit, lenders will not only check your credit report. They often also check the public record for any liens to your name.

So although tax liens are officially part of your credit report, lenders, credit card companies, landlords, and potential employers can still find out about liens against your property. You can be confident they will use this information when determining eligibility for a loan, a lease, or a new job.

When can you remove a tax lien notice?

There are four scenarios in which the IRS will consider removing a tax lien:

- The IRS jumped the gun and didn’t have its paperwork in order when it filed the notice.

- You have an installment agreement with the IRS, and you are current with your payments.

- You convince the IRS that removing the lien will make it easier for you to pay your taxes.

- It is in the best interest of the IRS and you to do so, such as when the debt has already been paid.

How to remove a tax lien from public records?

The first step is to either pay your tax debt in full or reach an agreement with the IRS. If you can’t afford to pay it in one lump sum, the IRS may consider other options. For example, the IRS may release a tax lien to allow you to sell a property if it allows you to pay some or all of your tax debt.

Thirty days after paying your tax in full, the IRS will release the lien on your property. However, this doesn’t mean it will be removed from the public record.

Other options that allow a withdrawal of your Notice of Federal Tax Lien

According to the IRS, your tax lien may be eligible for withdrawal if you meet the following conditions-

- You are a qualifying taxpayer (this includes individuals, businesses with income tax liability only, and out-of-business entities with any type of tax debt).

- You owe $25,000 or less in unpaid tax payments. (If you owe more than $25,000, you may pay down the balance to $25,000 before requesting withdrawal of the Notice of Federal Tax Lien.)

- Your Direct Debit Installment Agreement (DDIA) must fully pay the amount you owe within 60 months or before the Collection Statute expires, whichever is earlier.

- You’ve paid three full consecutive direct debit payments.

- All tax returns have been filed and you have no pending payments.

- You have not defaulted on your current, or any previous, Direct Debit Installment agreement.

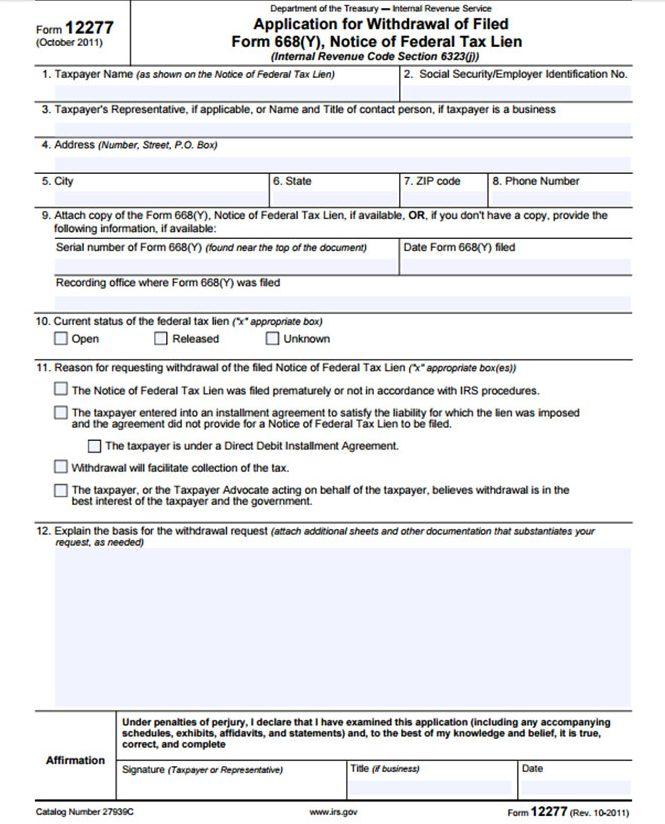

Complete IRS form 12277, “Application for Withdrawal of Filed Notice of Federal Tax Lien.”

Once the tax lien has been withdrawn, it is time to remove it from the public record.

To complete IRS Form 12277, follow these guidelines:

- Provide basic personal identification, such as your name, SSN, and address (items 1 to 8)

- Attach a copy of the tax lien notice, Form 668(Y) (item 9) you want to remove from your credit report. If you don’t have it, provide whatever information you do have so the IRS can identify the notice of federal tax lien you want to remove. Note that the IRS may have filed more than one tax lien notice.

- Specify if the debt that triggered the tax lien is open, released, or unknown (item 10).

- Give the government a reason for requesting the withdrawal of the tax lien notice (item 11). If your reason is that the IRS already released your tax lien, check the last box. Include a detailed explanation of why you think the IRS should remove the notice and attach any documents that support your claim (item 12). Make sure you write “see attached” in the box if you’re providing additional documents.

- Sign and date the document.

For additional guidance, review this video on the IRS website.

Provide the IRS with authorization to share the tax lien notice release

Here is a little know step that can really slow down things if forgotten. Attach a short letter authorizing the IRS to send a copy of your tax lien notice release to any financial institution or creditor you want to inform. Back when credit bureaus collected this information, you would also ask the IRS to notify all three credit reporting agencies. Nowadays, this is no longer necessary.

Without this authorization, the IRS cannot share the information with other institutions. Specify in the letter the name and address of each third party you want to notify. When tax liens used to appear on credit reports, consumers would request the IRS to send it to all three agencies.

Send the IRS Form 12277 to your local IRS advisory group manager

You can find the address for your local IRS advisory group manager in Publication 4235. Be sure to make copies of all of your documents before mailing them. If at a later date, additional copies of the withdrawal notice are needed, you must provide a written request to the IRS Advisory Group Manager. The request must provide:

- The taxpayer’s name, current address, and taxpayer identification number with a brief statement authorizing the additional notifications.

- A copy of the notice of withdrawal, if available; and

- A supplemental list of the names and addresses of any financial institutions or creditors to notify of the withdrawal of the filed Form 668(Y).

Wait for a response from the IRS

After 30-45 days, the IRS will contact the courthouse where the lien was filed to notify them to withdraw it. You will also be sent a copy of this notification.

The IRS may send a notice to the financial institutions or creditors you attached to your Form 12277, but don’t hold your breath. To be safe, send the tax lien withdrawal yourself.

Can you get the lien withdrawn from public records without paying the debt in full?

Yes, you can, but it’s rare. The IRS will only consider this move if it increases your ability to repay your debt. For example, imagine you are being offered a job in the financial sector, and your potential employer will only hire you if the tax lien is withdrawn. In that case, you can fill out Form 12277 and explain in part 12 of the form how the new job would help you pay your taxes. Of course, you will need to provide proof of your claims.

Should you hire a professional to remove your tax lien?

It’s always smart to get a tax attorney to look over any documents you send the IRS, especially if you’re being audited or applying for tax relief. However, you can also do it all on your own. The IRS also provides experts in lien withdrawals that provide advice to taxpayers. Publication 4235 provides the contact details of IRS lien advisors.

Remember that any information you provide to the IRS can be used against you. Having a tax expert on your team could help you avoid expensive mistakes and protect you from handing over self-incriminating information. This is particularly important if you’ve received a tax audit notice or if you’re dealing with a large tax debt.

At least find out what your options are under the IRS Fresh Start Program. If the IRS filed a tax lien on your property, you might qualify for a free consultation with a tax professional. While the cost of an attorney may be substantial, the impact on your finances a fresh start could provide is well worth it.

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

Share this post:

Table of Contents