Revenge Saving Trend Pushes 401(k) Contributions to All-Time High

Last updated 07/19/2025 by

Andrew Latham

Summary:

Americans are getting serious about saving again. After a wave of post-pandemic splurging, people are now contributing more to their 401(k)s and rebuilding personal savings. The national personal savings rate has nearly doubled from its 2023 low, and Fidelity reports a record-high 401(k) contribution rate of 14.3%. But this time, it’s not about fear. It’s about reclaiming control. Welcome to revenge saving.

After years of treating themselves, Americans are treating their future selves.

Welcome to the age of revenge saving, where people are shifting from impulsive spending to intentional saving. After years of revenge spending, many are now flipping the script. And the trend is real. From higher retirement contributions to a rise in personal savings rates, financial discipline is back and more purposeful than ever.

Compare Savings Accounts

Compare savings accounts. Discover your best option.

Personal saving is making a comeback

According to the U.S. Bureau of Economic Analysis, the national personal savings rate (the portion of disposable income people save rather than spend) has increased from a post-pandemic low of just 2.0% in June 2023 to 4.5% as of mid-2025. That’s a sharp turnaround during a time of economic recovery.

While 4.5% is still well below historical norms—personal saving rates were often between 7% and 10% before the 2000s—it’s a meaningful reversal from the revenge-spending slump that followed COVID-19 lockdowns. And it signals that Americans are ready to rebuild their financial buffers.

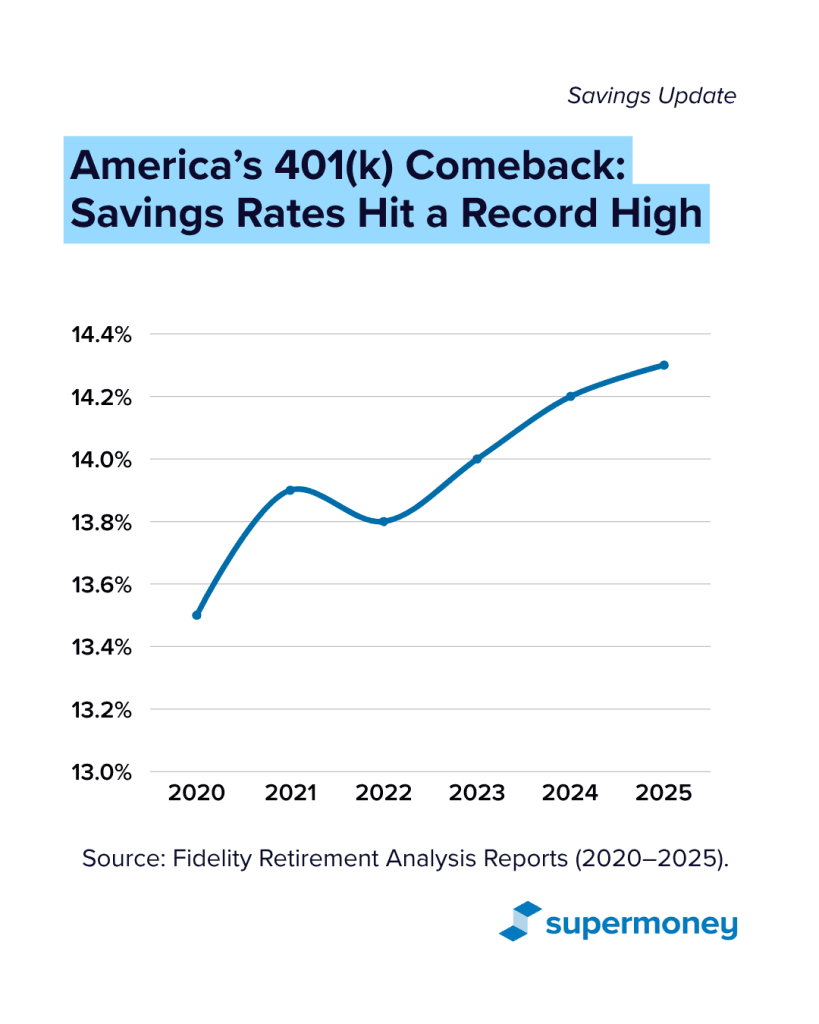

401(k) contributions hit a record high

According to Fidelity’s Q1 2025 report, the average total 401(k) savings rate reached an all-time high of 14.3%. That includes 9.5% from employees and 4.8% from employers, just shy of the gold-standard 15% target recommended by most financial experts.

Even more impressive? Americans kept saving even as the markets wobbled. While the average 401(k) balance dipped 3% in early 2025 due to volatility, 17.4% of workers increased their contribution rate. Less than 1% stopped saving altogether. That’s the kind of long-term confidence we want to see in investors.

Automation is boosting results

Better plan design is quietly revolutionizing how Americans save. Fidelity reports that:

- 43.7% of plans now automatically enroll employees

- 35.1% start employees at a 5%+ contribution rate (up from the old 3%)

- 67% of those who increased savings used auto-escalation tools

This “nudge effect” is reshaping financial behavior one paycheck at a time. Whether it’s a default setting that boosts your 401(k) each year or a reminder to top off your savings, gentle automation removes friction and helps people build habits that stick.

Apps and platforms that support this approach are making it easier than ever to stay on track. We believe in this model so strongly, we’re building one ourselves: the SuperMoney app is designed to help automate budgeting and deliver helpful nudges right when they matter most. Because sometimes, small reminders can lead to big results.

Cross-generation growth

All generations are catching the revenge saving wave, with younger groups quickly closing the gap.

- Baby Boomers: 17.2%

- Gen X: 15.4%

- Millennials: 13.5%

- Gen Z: 11.2%

One of the most encouraging shifts? Younger savers are increasingly choosing Roth 401(k)s. Nearly 19% of both Gen Z and Millennials now opt to contribute to Roth accounts, prioritizing tax-free growth over time.

Unlike traditional 401(k)s, Roth contributions are made with after-tax dollars, which means withdrawals in retirement are tax-free. That’s especially beneficial for younger workers who are early in their careers, likely in lower tax brackets now, and stand to benefit from decades of compounding. Choosing Roth early reflects a savvy understanding of long-term financial planning and a shift away from short-term thinking that defined the post-pandemic years.

How to ride the revenge-saving wave

Want to join the movement? Here’s how to make it work for you, without feeling deprived:

- Bump your rate by 1%: It’s a small move now, but it compounds significantly over time.

- Max your match: Don’t leave employer dollars on the table. Match it if you can.

- Turn on auto-escalation: Let your contributions grow each year without lifting a finger.

- Redirect raises or windfalls: Commit a portion to savings before it becomes spending.

- Use a tracker: Tools like SuperMoney’s app make planning and saving simple and stress-free.

Why this trend matters

Revenge saving isn’t about fear. It’s about freedom. After years of economic uncertainty, Americans are realizing that financial discipline gives them more power, not less. It’s not just about what you don’t spend. It’s about what you gain: confidence, options, and a stronger future.

Key Takeaways

- The average 401(k) savings rate hit 14.3% in Q1 2025, a new all-time high.

- More than 17% of savers increased their contributions, despite market dips.

- Auto-enrollment and escalation features are helping people save more with less effort.

- Generations across the board are saving more. Gen Z and Millennials are closing in fast.

- Nearly 1 in 5 young savers now contribute to Roth 401(k)s or Roth IRAs for future tax-free withdrawals.

- The national personal savings rate has risen from 2.0% in 2023 to 4.5% in 2025 (encouraging but still historically low).

- Revenge saving is a movement that replaces spending guilt with financial confidence.

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

Share this post:

Table of Contents