Student Loan Refinance: Variable Vs Fixed — Which Offers the Best Deal?

HS

Last updated 04/19/2022 by

Heather SkylerWhen I decided to go with a fixed rate on my student loan refinance, I thought I’d made a great decision because interest rates were at a low 8%. Wait a minute — you’re probably thinking — 8% is not considered low.

That’s true: It’s a decent interest rate, but if I’d gone with a variable rate I could’ve locked it in as low as 4% at one point. But I was fresh out of college and really had no idea about interest rates, so for now, I’m stuck with my middle-of-the-road 8%.

Of course, interest rates could have shot back up to percentages seen in earlier decades where rates were in the teens. My point is, it’s hard to predict the market and what interest rates will do.

So how do you decide when it comes to refinancing your student loan? Should you go with a variable or fixed interest rate? Let’s take a look.

Get Competing Student Loan Refinancing Offers

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

Variable vs. Fixed

Rick Castellano, vice president of corporate communications at Sallie Mae, says, “Each situation is different, so it really comes down to the student’s preference. Fixed rate loans may be more predictable, but the rates tend to be higher so you’ll pay more.

Variable rates may be less and could mean lower total student loan costs, but the rate can rise or fall depending on the market index. At Sallie Mae, during the application process, we lay out both options and help estimate monthly payments with each.”

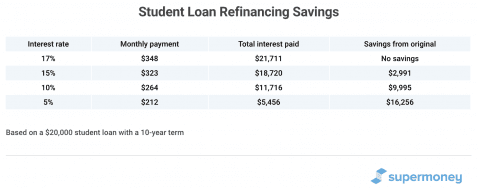

Loan payments based on interest rates

You can hear a number thrown out like 8%, but it’s difficult to envision what that means in terms of repayment. Let’s look at an imaginary student loan for $20,0000, with a 10-year term and varying interest rates.

As you can see, if your loan has a 5% interest rate over the life of the loan, you could save $16,255.72 in interest (if the other option was 17%). You’d also pay $135 less each month.

When you go to refinance your loan, remember this chart. If you can lock in an interest rate 5% or lower, a fixed rate loan is a pretty safe option. If rates are above 7%, consider risking a variable rate.

However, remember the pros and cons of each option and weigh your decision carefully.

How to get started

The process of refinancing entails renegotiating the terms of an existing student loan or multiple student loans into a brand new loan. You can shop around for your interest rate — and whether it will be fixed or variable — and your repayment terms, including the length of repayment.

If your student loan is a federal Stafford or Direct loan, it can’t be refinanced into a new federal loan so you’ll need to go through a third-party lender, like SoFi or CommonBond. Some banks, including CItizens Bank, also refinance student loans.

To find the best terms at the lowest rates, compare student loan refinancing companies now.

HS

Heather Skyler writes about business, finance, family life and more. Her work has appeared in numerous publications, including the New York Times, Newsweek, Catapult, The Rumpus, BizFluent, Career Trend and more. She lives in Athens, Georgia with her husband, son, and daughter.

Share this post: