Subprime Credit Returns to Pre-Pandemic Levels: More Than One in Four Americans Is Now Non-Prime

Last updated 01/08/2026 by

Andrew Latham

Summary:

Subprime credit has returned to pre-pandemic levels, signaling that the temporary credit gains many Americans saw during COVID have largely faded. At the same time, more than one in four consumers now falls into the non-prime category. As credit stress normalizes, research shows that small behavioral changes can help prevent further slippage.

The credit rebound many Americans experienced during the pandemic is officially over. After several years of stimulus, payment relief, and reduced spending, subprime credit has climbed back to where it stood before COVID—while the share of non-prime consumers has quietly grown even larger.

New data from TransUnion shows that this shift is not sudden or dramatic. Instead, it reflects a steady return to pre-pandemic patterns as household budgets tighten and financial cushions thin.

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

Subprime credit has fully reverted to pre-pandemic levels

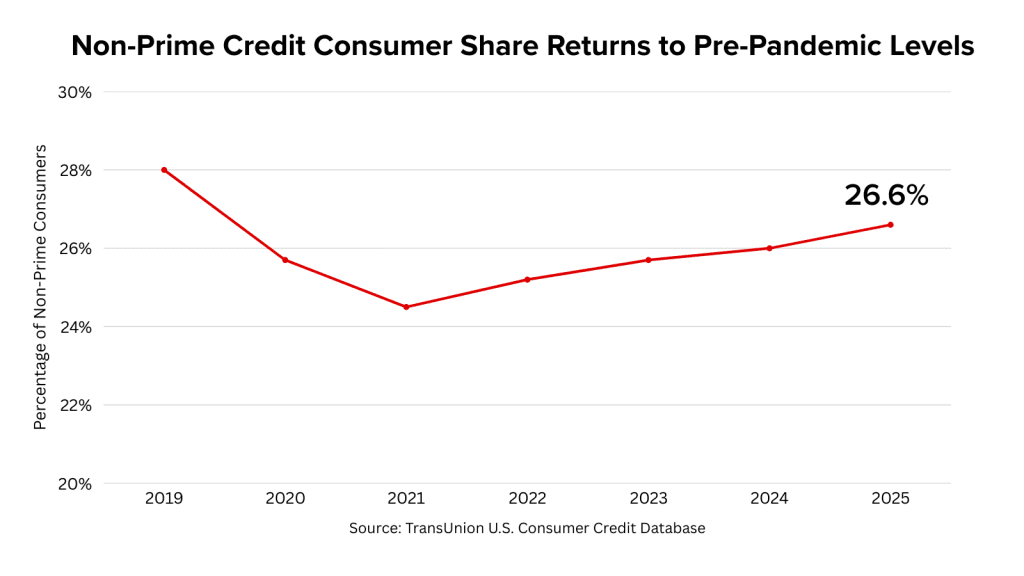

In Q3 2019, just before the pandemic, subprime borrowers made up 14.5% of consumers. By Q3 2025, that share stands at 14.4%—a clear return to pre-pandemic levels after a temporary dip in 2020 and 2021.

| Credit tier | Q3 2019 | Q3 2020 | Q3 2021 | Q3 2022 | Q3 2023 | Q3 2024 | Q3 2025 |

|---|---|---|---|---|---|---|---|

| Super prime | 37.1% | 38.9% | 38.4% | 38.3% | 39.3% | 40.3% | 40.9% |

| Prime plus | 17.6% | 17.9% | 19.2% | 18.9% | 18.0% | 17.4% | 16.9% |

| Prime | 17.4% | 17.5% | 18.0% | 17.6% | 17.0% | 16.3% | 15.6% |

| Near prime | 13.5% | 13.2% | 12.7% | 12.4% | 12.3% | 12.1% | 12.2% |

| Subprime | 14.5% | 12.5% | 11.8% | 12.8% | 13.4% | 13.9% | 14.4% |

| Total non-prime | 28.0% | 25.7% | 24.5% | 25.2% | 25.7% | 26.0% | 26.6% |

What has changed is the size of the broader non-prime population. When near-prime borrowers are included, 26.6% of Americans—more than one in four—now fall outside the prime credit range.

The middle is shrinking as credit becomes more polarized

While subprime credit has normalized, the composition of the credit spectrum has shifted. The share of super prime consumers has continued to rise, reaching nearly 41% by Q3 2025. At the same time, traditional prime and prime-plus tiers have gradually thinned.

This pattern points to growing polarization. Some households have emerged from recent years with stronger credit than ever, while others are sliding back as higher prices, interest rates, and everyday expenses strain budgets.

That strain is widespread. According to PNC Bank, 67% of U.S. workers live paycheck to paycheck, leaving little room to absorb missed income, medical bills, or higher credit card balances. In that environment, small setbacks can quickly translate into lower credit tiers.

Why small behaviors matter more as stress normalizes

Credit scores are shaped primarily by repeat behaviors. The Consumer Financial Protection Bureau notes that payment history and credit utilization account for the largest share of most scoring models. As a result, consistency matters more than one-time financial decisions.

Behavioral finance research supports this. A Federal Reserve Bank of Boston field experiment found that simple reminders helped low-score consumers reduce debt and improve payment behavior, leading to meaningful credit score gains. Other research from the Federal Reserve and the National Bureau of Economic Research shows that making finances more visible and automated reduces missed payments and helps consumers adjust before balances grow.

These effects are especially important for near-prime consumers—the group most at risk of slipping into subprime as financial pressure builds.

Preventing credit slippage before it starts

As subprime credit returns to pre-pandemic levels, the lesson is not that credit is collapsing—but that the temporary relief of the pandemic era has faded. For many households, avoiding further slippage will depend on building systems that support consistency.

Budgeting tools that emphasize spending visibility, bill planning, and habit formation can help reinforce the behaviors that matter most. SuperMoney’s app, for example, is designed to help users anticipate bills, track spending, and reduce missed payments before they affect credit.

In today’s environment, small behavioral nudges may be the difference between holding steady and falling behind.

Key takeaways

- Subprime credit has returned to pre-pandemic levels.

- More than one in four Americans (26.6%) is now non-prime.

- The middle credit tiers are shrinking as polarization grows.

- Consistent habits matter most as pandemic-era relief fades.

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

Share this post:

Table of Contents