Secret of Retirement Savings: Making Up For Lost Time?

JW

Last updated 03/20/2024 by

Jessica WalrackHave you begun to save for retirement? According to a recent survey, only two out of three workers feel confident about having enough money to live comfortably in their retirement. Most people don’t start saving for retirement until they hit 31, which undercuts their returns significantly.

Even though retirement may seem far off, the earlier you start to plan and save, the better. But why is it so important to start early? And where should you start? Read on for a quick crash course on retirement planning.

Wealth Management Companies

Compare the fees and perks of the leading wealth management companies. Find the best for your lifestyle.

What is retirement planning?

Retirement planning is the process of estimating how much money you will need after you retire, and then laying out a plan to get it.

A recent survey showed that only two out of five workers had tried to calculate how much money they would need to live comfortably in retirement. And one-third of workers who did do the math found they would need at least $1 million.

You don’t want to discover this revelation when you only have 10 or 20 years left to save. It’s much less stressful when you’re still 30 to 40 years away from retirement. That way, you can let compound interest do the heavy lifting.

What delays retirement savings?

When you’re young, it can be hard to save for several reasons. Here are two of the most common roadblocks to retirement savings.

Debt

Three in five workers say that debt impedes their ability to save for retirement. It’s no surprise, given the fact that 45 million Americans are carrying an average of $32,731 in student debt. If you’re one of them, that can be a significant obstacle to retirement savings.

And it’s not just student debt that keeps young people from planning for the future. Debt from credit cards, auto loans, and personal loans can eat up a large chunk of your disposable income. Seven out of 10 workers admit that non-mortgage debt impacts their ability to save for retirement.

Other financial goals

Additionally, more than half of workers feel that they are unable to save for retirement and other financial goals at the same time. And unfortunately, those other financial goals loom far closer on the horizon than retirement. Say you’re trying to save for a down payment on a house, for your wedding, or your child’s college fund. You likely only have 10 or 15 years to save up the money you need.

Retirement, on the other hand, can feel blissfully far off — easily 40 or even 50 years away — and thus get relegated to the end of your to-do list. If you’re in your 20s, saving for retirement may not even be on your radar yet. After all, you only have so much disposable income.

Unfortunately, that means that many Americans don’t start saving for retirement until it’s too late. And when you look at the big picture, starting to make contributions toward your retirement at age 23 can save you a ton of anxiety later.

Why is it so important to start early?

Just how big of a difference does it make to start saving at the age of 23 versus 31? A recent study looked at the difference between investing in an account with a 6% annual rate of return starting at 23 and 31.

If you invest $100 from each paycheck starting at age 23, you will have $434, 299 by the time you retire at age 65. But if you begin at age 31, you’ll only have $257,156. The first eight years make a difference of $177,143!

Now, let’s say you can only afford to invest $50 from each paycheck. If you start at age 23, you’ll end up with $257,156 by age 65. If, on the other hand, you begin at age 31, you’ll only have $128,578. That’s a difference of $88,572.

Why do those early years make such a big impact on your savings? Because of compounding interest. As such, it’s worth taking the time to set a budget in your 20s that enables you to invest $50 or $100 into your retirement fund every month.

Need help massaging your budget into shape? These money management tools can help.

How much does investing sooner really help your retirements savings?

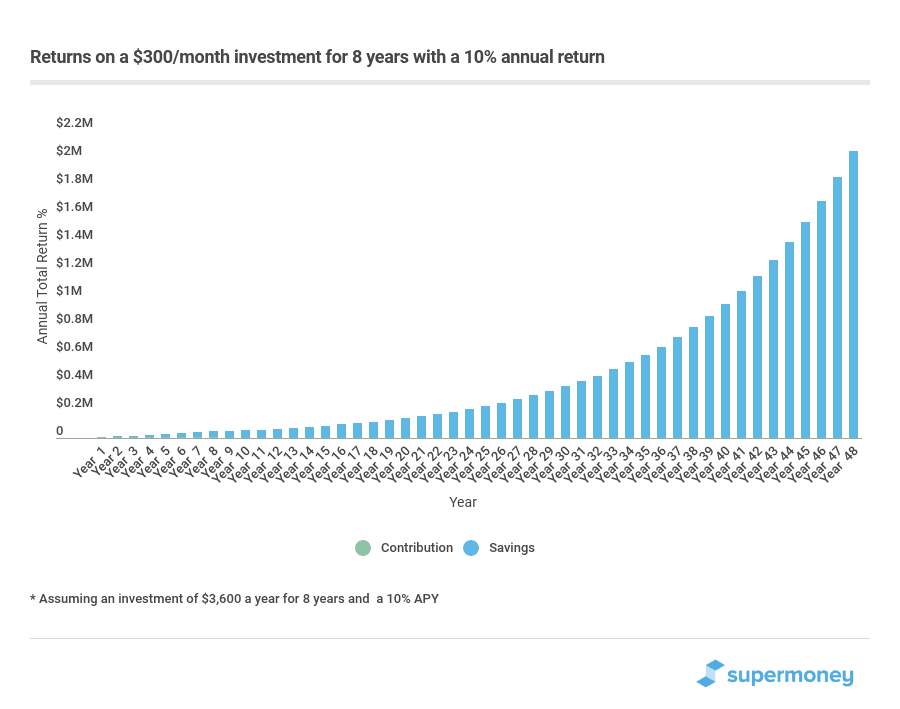

Let’s say an 18-year-old invests $300 a month for just eight years (a total of $28,800). She could retire with more than $1 million at age 58 even if she never invests another dime. If she waits till 65, the total will exceed $2 million.

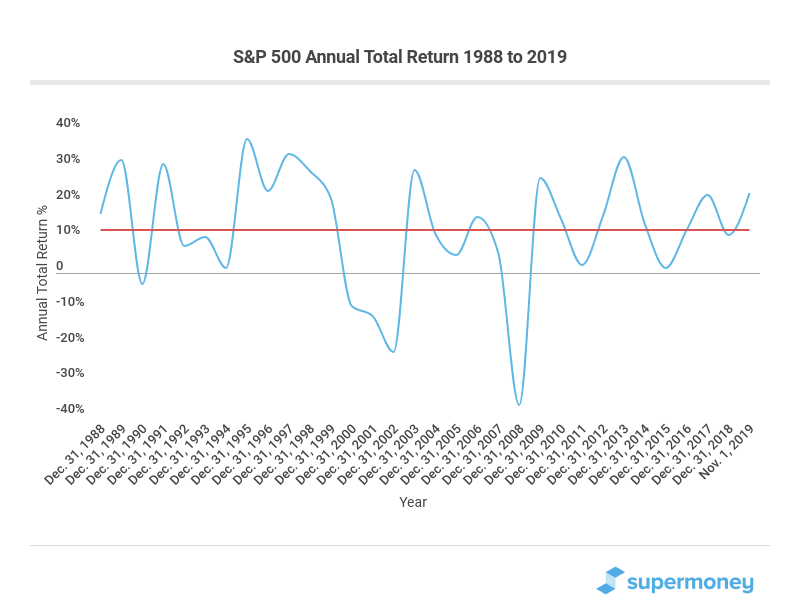

That impressive return on investment assumes a 10% annual return, which is the average return for the S&P 500 over the last 90 years. In the last 30 years, the average was 12.11%. Investors typically use the S&P as a benchmark for the overall stock market.

For more tips, read SuperMoneys’s investment guide.

Three ways to approach investing your money

Depending on how much experience you have with investing and whether or not you want to learn, there are three approaches you can take to investing your hard-earned cash.

1. DIY

Brokerages allow you as the investor to make your own investment decisions. That includes picking what assets to invest your money in, diversifying your portfolio to reduce your risk, and continually managing that portfolio over time. If you’re new to investing, this way of doing things might be daunting. But if you have the time and desire to learn, it’s a great way to learn from experience, allowing you to improve your investing skills over time.

2. Financial advisors

There’s an entire industry of people who have trained and are licensed to manage other people’s money. Financial advisors spend their lives in the financial markets, which can help them make good and timely investment decisions. That said, not all financial advisors put their clients first, and many of them work on commissions rather than a flat fee. Even if you get a fee-only advisor, that fee eats into your investment returns. This option is good if someone doesn’t want to manage their own money and is fine with paying a little extra to — potentially — get a better return than they can do on their own.

3. Robo-advisors

Relatively new onto the scene, robo-advisors do many of the same things that you or a financial advisor can do — picking your investments, diversifying your portfolio, and managing the funds as things change over time — at a fraction of what financial advisors charge. The primary problem with robo-advisors is that you have very little control over where your money is invested. You can say you want 90% of your money in stocks and the other 10% in bonds, for example, but you can’t choose the actual funds. You also can’t talk to a person about how your investments are doing. But if you’re new and aren’t concerned with those issues, a robo-advisor could be an inexpensive way to achieve your investing goals.

Other ways to invest your retirement savings

Investing in stocks, bonds, and mutual funds is more traditional. But there are other investment options that can help you achieve your investing goals.

Other securities

There are several different types of assets you can invest in through most brokerages. Here are just a few:

- Options: These derivatives are contracts to buy or sell a stock or any other financial product.

- Futures: These are agreements to buy or sell assets, especially commodities, at a fixed price but to be delivered and paid for later.

- Exchange-traded funds: These function similarly to mutual funds, which means that they invest your money in a diversified group of assets. But unlike mutual funds, you can buy and sell ETFs like a stock.

Marketplace investing sites

Instead of investing in an asset, these companies allow you to invest by lending money directly to borrowers. Marketplace platforms, also known as peer-to-peer lending, make it easy to diversify your portfolio away from conventional financial assets that may be sensitive to market changes.

Crowdfunding Sites

Investing in startups and real estate used to be something only wealthy investors could do. Thanks to crowdfunding platforms, you also help startups get off the ground or invest in large real estate projects and reap the benefits of their success.

Seven steps to start investing today

It’s not easy to choose the best way to invest for you. But it’s better to start somewhere than to wait years because you don’t have the time or desire to nail down your investment strategy. To help you get started, here are seven steps:

1. Decide how much you want to invest

It’d be nice to get a windfall you can place in the stock market and watch grow. But for most people, it comes down to investing a little each month. Even if you just have a few dollars to invest each month, there are investment options out there for you. So, take a look at your budget and decide how much you can comfortably invest without cutting essential expenses.

2. Start with retirement

Investing for a time that’s still decades to come doesn’t sound exciting. But when it comes time to enjoy your golden years, your older self will thank you. If you have a 401(k) or similar retirement plan with your employer, start there. Employers often offer a contribution match, which essentially gives you an immediate 100% return on your investment. For example, say you contribute 3% of your salary, and your employer matches it dollar for dollar. You’re now saving 6% of your salary while only doing half the work.

3. Decide what your other investment goals are

Once you’ve got a good savings rate for retirement, start thinking about what other investment goals you have. If you just want to save for something in the future, it’ll be harder to stick to your investment plan. But if you have something specific, such as buying a house or going on a once-in-a-lifetime vacation, it’ll be a lot easier to stay focused on your goal each month.

4. Automate your investments

If you are an employee, setting up your 401(k) is easy — your employer will automatically deduct your contributions from your paycheck. If you are self-employed or want to invest in other ways, set up an automatic contribution. More importantly, make it part of your budget. You may be tempted to try just to invest what’s leftover at the end of the month. But if you do this, you’ll likely have a hard time investing enough for your future needs. After all, going out to eat now sounds a lot more fun than waiting for years to see an investment pan out.

5. Keep it as simple as possible

When you’re just starting out, you may have dreams of hitting it big with the stock market. But right now, it’s all about getting some experience under your belt. It’s best to invest in mutual funds and similar investments. That way, you don’t need to do the significant research required to make a good stock pick, and you don’t need to worry about whether your investments are too risky.

6. Learn as much as possible

As you get started, you can leave the management of your investments to a financial advisor or robo-advisor. But over time, the more you know about how the investment world works, the higher your chances of earning higher returns. There are countless investing books and websites out there dedicated to helping investors like you to learn how to improve their understanding. Also, if you’re using a brokerage, you may have special access to their tools and resources that can give you practical insight as you’re managing your investments.

7. Be cost-conscious

As mentioned previously, the higher your costs of investing, the lower your effective return. Different brokerages and advisors charge different fees, so it’s important to consider several options before choosing one.

The bottom line on investing

Becoming a sophisticated investor takes years of experience and learning. But the longer you wait to start, the longer it will take to figure things out. More importantly, the longer you wait to invest, the less money you’ll have for future goals. So, even if you’re not ready to take on the firehose of information about investing, setting up a basic investment account, and contributing each month can help you get started.

JW

Jessica Walrack is a personal finance writer at SuperMoney, The Simple Dollar, Interest.com, Commonbond, Bankrate, NextAdvisor, Guardian, Personalloans.org and many others. She specializes in taking personal finance topics like loans, credit cards, and budgeting, and making them accessible and fun.

Share this post: