5 Reasons Why Trump’s 50 Year Mortgage Proposal Is a Horrible Idea

Last updated 11/11/2025 by

Miron Lulic

Edited by

Andrew Latham

Summary:

The 50-year mortgage offers lower monthly payments and easier loan qualification, but at a high cost. Homeowners pay significantly more over time, build equity slowly, and would face higher interest rates. While it may help a few buyers in high-cost markets, it could worsen the housing crisis by pushing prices higher. True affordability requires fixing supply, not stretching debt.

Compare Home Loans

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

5 reasons 50 year mortgages are not a good idea

Trump’s proposal to extend mortgage terms to 50 years has sparked a national conversation, but beneath the promise of lower monthly payments lies a minefield of long-term risks. Below are five reasons why this plan could do more harm than good.

1. Little effect on affordability

With home prices and mortgage rates both high, a new idea is gaining traction—the 50-year mortgage. President Donald Trump floated it on November 8–9, 2025, as a way to expand homeownership. Supporters say it could make housing more affordable. Critics argue it only adds long-term financial risk.

How a 50-year mortgage works:

It stretches repayment over 50 years instead of the traditional 30. The longer term reduces monthly payments, helping buyers meet debt-to-income (DTI) ratios.

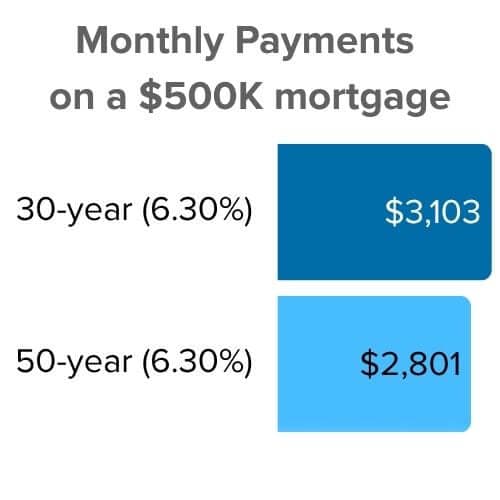

Illustrative example at the same 6.30% rate on a $500,000 loan:

- 30-year loan: ~$3,103/month

- 50-year loan: ~$2,801/month

- Monthly savings if rates were identical: ~$302

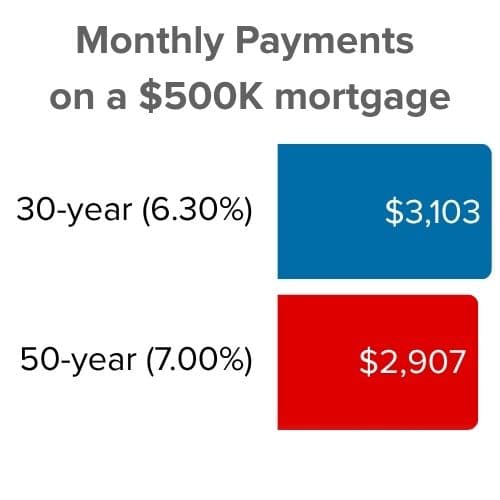

Longer terms have higher interest rates

Reality check: 50-year loans would carry higher rates (+0.7% to +1.0% or more) because they expose lenders to decades of extra risk. At a realistic 7.00%, the 50-year payment rises to ~$2,907, cutting savings to just $196/month. At 7.30%, savings shrink to $146/month.

2. Explodes the long-term cost

| Scenario | Rate | Monthly payment | Total interest |

| 30-year standard | 6.30% | $3,103 | $617,080 |

| 50-year — Same rate (unrealistic) | 6.30% | $2,801 | $1,180,600 |

| 50-year — Realistic rate +0.70% | 7.00% | $2,907 | $1,244,200 |

| 50-year — Conservative +1.00% | 7.30% | $2,957 | $1,274,200 |

Bottom line: The longer term guarantees a higher rate. Once that penalty is added, the monthly “savings” become tiny, but the lifetime cost explodes past $600,000 extra interest.

3. Retirement risk

A borrower who buys a home in their early 30s could still be making payments well into their 80s. That timeline fundamentally changes what homeownership means.For one, it blurs the line between owning and renting — you may technically own your home, but you’re still making payments for most of your life.

Entering retirement with a mortgage means a large, fixed expense at precisely the time income typically drops. Instead of freeing up cash flow for travel, healthcare, or leisure, a big portion of retirement income would go toward the bank.What seems like affordability in the short term could become a generational form of debt — stretching from one phase of life into another, with retirement becoming less a milestone and more a continuation of repayment.

4. Will lead to housing inflation

Longer terms let buyers qualify for bigger loans, which pushes prices higher in supply-constrained markets. Canada (40-year loans pre-2008) and the UK (35–40-year terms) saw similar demand spikes followed by tighter rules. Extending terms doesn’t add homes, lower land costs, or raise wages, it just inflates another bubble.

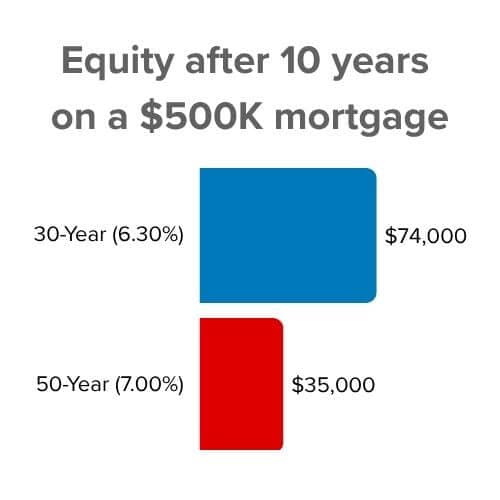

5. Slows equity growth

A long mortgage term builds equity slowly, so homeowners have less to tap into if they want to downsize, relocate, or take out a home equity loan. The extended debt burden can even make it harder to qualify for new credit, as lenders see a large, decades-long obligation on your balance sheet.

After a decade, the 50-year borrower has less than half the equity despite paying only ~$196 less per month.

Are there better ways to help first-time buyers?

Yes. One alternative would be for the Federal Reserve to offer banks access to low-cost borrowing facilities specifically for funding first-time homebuyer loans. Instead of banks lending at 6–7%, they could lend at a reduced rate, say, 3.3%, by borrowing from the Fed at a preferential rate tied to this program.

This kind of targeted facility would allow private lenders to offer lower-rate mortgages without needing direct subsidies or long-term taxpayer guarantees. It could deliver far more monthly savings than a 50-year mortgage, while avoiding the debt drag that comes with ultra-long terms.

For example, a $500,000 loan at a reduced 3.3% rate would result in a monthly payment of about $2,190, saving roughly $950/month compared to a 30-year loan at today’s average 6.3% rate—and 5× more than the savings from a 50-year loan at a realistic 7.0% rate.

Countries like Japan and Singapore have used similar targeted lending strategies to support first-time buyers effectively without inflating the market with risky, long-term debt.

But even this type of targeted interest-rate relief is still treating the symptom. The real cure is increasing housing supply and the biggest roadblock to supply is NIMBYism.

What is NIMBYism?

“NIMBY” stands for “Not In My Back Yard.” It describes residents who oppose new housing construction in their neighborhoods even when the region desperately needs more homes. Common NIMBY tactics include:

- Filing endless appeals against new apartment buildings or townhouses

- Pushing for restrictive zoning laws

- Demanding huge parking requirements or environmental reviews

- Arguing that new residents will “ruin the character” of the neighborhood

The result? In cities like San Francisco or Boston, it can take 5–10 years and millions in legal fees to build even modest housing. Land that could hold 200 homes ends up with 4 McMansions.

What would actually fix housing?

- Federal incentives tied to zoning reform

- State laws legalizing duplexes and fourplexes by right

- A federal Housing Abundance Act overriding restrictive local ordinances

- Fast-track permitting within 1/2 mile of transit

Until we override NIMBYism and build millions more homes, every demand-side trick, 50-year mortgages, rate discounts, and tax credits will mostly just raise prices.

Key takeaways

- 50-year loans will carry higher rates (+0.7–1.0%+), slashing monthly savings to $146–$196

- Interest paid can exceed 2× the amount paid on a 30-year loan

- Equity builds painfully slowly; debt may last into your 80s

- Demand-side fixes raise prices unless matched by supply reform

- The real solution: override NIMBY zoning and build more housing

Miron Lulic is founder and CEO at SuperMoney, a service that helps millions of people transparently compare financial services such as loans, investments, and more.

Share this post:

AddTable of Contents