What Does 2011 Teach us About the 2025 U.S. Debt Downgrade?

Last updated 05/19/2025 by

Miron Lulic

Edited by

Andrew Latham

Summary:

The U.S. debt downgrade by Moody’s has revived comparisons to the 2011 S&P downgrade. However, history suggests that the immediate impact may be more symbolic than systemic. Falling Treasury yields and rising mortgage-sector activity could again defy expectations, even as federal deficits remain historically wide.

Moody’s downgraded U.S. government debt from AAA to AA+. That kind of headline sounds ominous—and it has stirred fresh anxiety across the markets. Stocks have slipped and Treasury yields spikes in response to the downgrade. After all, a downgrade from one of the big three ratings agencies should raise borrowing costs and signal weakening fundamentals, right?

Not necessarily.

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

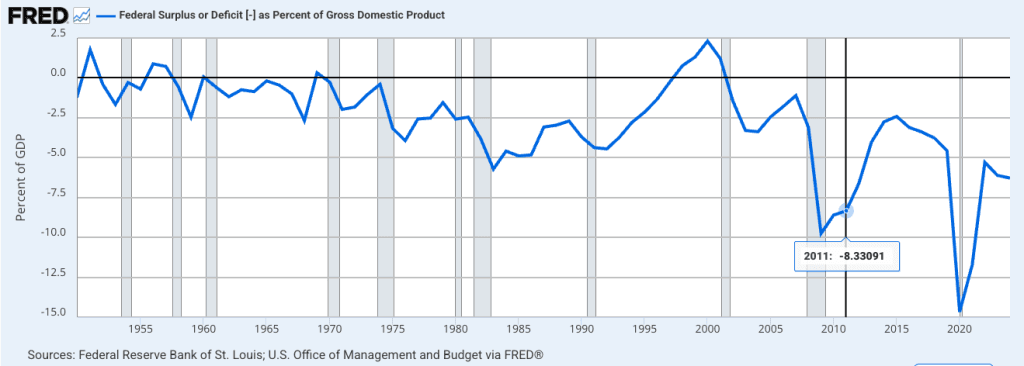

How budget gaps evolved—and what changed after the 2011 downgrade

This chart tracks the U.S. federal surplus or deficit as a percentage of GDP since 1950. Blue bars mark recession periods.

- Deficits typically widen during recessions due to falling revenues and higher spending.

- Post-crisis recoveries are taking longer to normalize. The COVID-19 deficit spike was historic, but even today, the deficit remains high.

- As of early 2025, the deficit sits near -6.3% of GDP—unusually high for a non-recessionary period.

This persistent shortfall helps explain concerns from ratings agencies. It also underscores the paradox: even with a strong labor market and moderating inflation, the government is borrowing at levels once reserved for emergencies.

The chart illustrates a familiar pattern. U.S. fiscal deficits widen significantly during recessions as government spending rises and revenues fall. What’s interesting is that the first-ever downgrade of U.S. debt by S&P in August 2011, which triggered a surprising market rally, also marked a turning point in fiscal trends. From that point on, deficits became more persistent, even during economic expansions, reflecting a shift toward chronic structural imbalance.

If history is any guide, the market reaction might surprise you. Back in 2011, when S&P delivered the first-ever downgrade of U.S. sovereign debt, the result wasn’t a bond market meltdown. It was a rally. Treasury yields fell. Mortgage rates dropped. And sectors tied to housing and credit outperformed. Here’s why that same contrarian outcome could repeat in 2025.

Flight to quality: why Treasuries remain the world’s safe haven

Despite the downgrade, U.S. Treasuries continue to offer unmatched liquidity and trust. With no true substitute on the global stage, institutional investors often respond to uncertainty by buying, not selling, government bonds. That can drive yields lower, counter to conventional wisdom.

Falling rates fuel housing and mortgage-linked sectors

Lower Treasury yields usually mean lower mortgage rates. That opens the door for homebuyers and refinancers, while boosting demand for mortgage REITs, homebuilders, and fintech platforms tied to housing. The 2011 playbook may repeat, making this a contrarian buying opportunity.

The Fed has a cover to remain dovish

If the downgrade tightens financial conditions or rattles sentiment, the Federal Reserve has room to pause or pivot. That would further support rate-sensitive equities and lending activity, even as inflation normalizes.

The real risk is political dysfunction, not default

The downgrade reflects governance concerns more than financial instability. Unless the U.S. hits another debt ceiling deadlock, default risk remains negligible. But investors may grow increasingly wary of fiscal policy uncertainty.

Takeaway: symbolic downgrade, real opportunities

Markets may shrug off the downgrade much like they did in 2011. The bigger story could be falling yields, Fed flexibility, and momentum in mortgage-linked sectors. For long-term investors, this could be less of a crisis and more of a contrarian signal.

Stay calm. Stay contrarian. And look where fear might be mispricing opportunity.

Key takeaways

- Moody’s has downgraded U.S. debt to AA+, following S&P and Fitch.

- Past downgrades have led to falling Treasury yields and housing sector strength.

- U.S. deficits remain wide at -6.3% of GDP, even outside of recession.

- Investor confidence in U.S. debt remains strong due to global liquidity needs.

- The downgrade is more about political dysfunction than fiscal collapse.

Miron Lulic is founder and CEO at SuperMoney, a service that helps millions of people transparently compare financial services such as loans, investments, and more.

Share this post:

AddTable of Contents