Why Gen Z is Skipping Homeownership — and Investing in Stocks Instead

Last updated 10/14/2025 by

Andrew Latham

Summary:

Younger generations are rethinking the American dream of homeownership. Faced with high property prices, elevated mortgage rates, and a booming stock market, many Gen Z and millennials are choosing to rent and invest instead of buying a home. This shift has broad implications for wealth-building, real estate markets, and generational equity.

Buying a home has long been considered the cornerstone of building wealth in the U.S. But in today’s financial landscape, younger Americans are questioning that tradition. Soaring home prices, steep mortgage rates, and limited inventory are colliding with a thriving stock market and more accessible investing tools.

This new reality has led many in Gen Z and millennials to ask a fundamental question: Is it smarter to rent and invest, or buy and build equity the traditional way?

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

The affordability crisis meets a booming stock market

In 2025, the average price of a home is in the neighborhood of $400,000. With a 6.5% mortgage rate and a 15% down payment ($60,000), a buyer faces monthly mortgage payments of around $2,170. Add in property taxes, insurance, and maintenance, and housing costs can eat up nearly half of a median household’s income.

Even more discouraging is that this financial strain doesn’t guarantee a good investment return, especially if home price growth slows. For young people, these costs make entering the housing market feel increasingly out of reach.

Stocks: The new path to wealth?

At the same time, the stock market is booming. Many younger investors have grown up in a world where stocks return an average of 14% annually—well above historical norms. Combine that with zero-commission trading apps and viral financial advice on platforms like TikTok and YouTube, and it’s no wonder that 37% of 25-year-olds now have investment accounts—up from just 6% in 2015, according to JPMorgan Chase.

This shift signals a new mindset: instead of tying up capital in a home, many are opting to grow wealth through stocks and ETFs while enjoying the flexibility of renting.

What the Numbers Say: Renting and Investing vs. Buying

Let’s compare two disciplined households—one rents and invests, the other buys a home. Both are financially responsible, but outcomes vary based on market returns and rent inflation.

Scenario 1: Strong Market for Both Renters and Owners

- The investor-renter: Invests an $80,000 down payment plus $13,500 annually (savings from renting vs. owning). Assuming a 9% annual return, they end up with around $390,000 after 10 years.

- The homeowner: Buys a $400,000 home that appreciates at 4% annually. After 10 years, it’s worth $592,000. After paying off part of the mortgage and selling (net of 5% costs), they walk away with about $305,000.

In a strong market, disciplined investing can outperform—but it requires consistency, risk tolerance, and market cooperation. Homeownership delivers steady equity, housing stability, and tax advantages.

Scenario 2: Slower Market with Rent Inflation

- The investor-renter: Same disciplined investing strategy ($80,000 upfront + $13,500/year), but with a 6% annual return and 2.5% rent inflation gradually reducing the savings gap. After 10 years, the renter has about $293,000.

- The homeowner: Same purchase and appreciation. Net equity after 10 years remains around $305,000.

In a lower-return environment with rising rents, the homeowner pulls ahead—benefiting from fixed housing costs and consistent equity growth.

Bottom line: Renting and investing can match or beat homeownership—if you invest diligently and the market performs. But if returns lag or rents rise, owning often wins over the long term. And while home equity isn’t liquid, it’s a powerful tool for forced savings and financial stability.

Why younger generations are falling behind in homeownership

For decades, homeownership symbolized financial success and stability in America. But for today’s younger generations, that path is harder to follow. Gen Z and millennials are working, saving, and investing—but many are still falling behind when it comes to building wealth through real estate.

Generational ownership gaps widen

According to Redfin, homeownership rates among younger adults have stalled. In 2024, just 26% of Gen Z adults owned a home, and millennials held steady at 55%. In contrast, Gen X and baby boomers had significantly higher ownership rates at the same age.

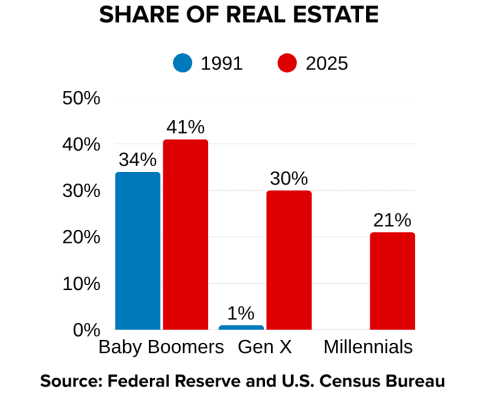

But the gap looks even wider when we step back and examine long-term data from the Federal Reserve. Between 1991 and 2025, the distribution of U.S. real estate ownership by generation has shifted dramatically:

The imbalance is clear: Millennials now own less than two-thirds of the real estate share that baby boomers held at the same age. And while millennials make up 34% of today’s homeowning-age population, they control just 21% of U.S. real estate.

One major reason for the disparity is timing. Baby boomers bought homes when prices were lower and mortgage rates were more favorable. They’ve benefited from decades of appreciation—and many aren’t planning to sell. In fact, one survey found that a third of boomers who own their homes say they intend to stay put, limiting housing inventory for younger buyers.

Barriers beyond price

High prices are only part of the challenge. Younger buyers are also burdened by student loan debt, elevated mortgage rates, and a severe lack of affordable inventory. Even lower-cost condos and townhomes can be out of reach when you factor in HOA fees, insurance, and rising maintenance costs.

With these headwinds, many in Gen Z and the millennial generation are opting to rent and invest instead. They’re looking for liquidity, flexibility—and a path to wealth that doesn’t depend on owning property.

One key reason is timing. Baby boomers bought homes when prices were far lower and mortgage rates were more favorable. They’ve since built up equity and wealth—while nearly a third say they never plan to sell. That limits inventory and keeps prices high, creating even more hurdles for younger buyers trying to get a foot on the property ladder.

Barriers beyond price

High home prices are only part of the story. Younger buyers also face heavy student loan debt, rising mortgage rates, and a severe lack of affordable housing. Even entry-level options like condos or townhomes can be out of reach once you factor in rising HOA fees and maintenance costs.

And with economic uncertainty, many prefer the freedom to rent and invest their money elsewhere—especially when homeownership feels more like a burden than a milestone.

The emotional side of buying vs. renting

Buying a home isn’t just a financial decision. It offers stability, pride of ownership, and freedom to renovate or stay put for years. Many homeowners aim to retire mortgage-free and avoid rent hikes in old age.

But renting offers its own perks—flexibility to relocate, lower upfront costs, and freedom from maintenance headaches.

Frequently asked questions

Is it smarter to rent and invest or buy a home?

It depends on your goals. If you value flexibility and can consistently invest savings, renting and investing can be smart. But if long-term stability and building home equity matter more, buying might be better.

Why is Gen Z buying fewer homes?

High prices, elevated mortgage rates, student debt, and limited inventory make it hard for Gen Z to buy. Many prefer to invest their money and maintain flexibility.

Can renting really build wealth?

Yes—if you invest the money you save by renting instead of buying. But it requires discipline and long-term planning.

What are the downsides of homeownership?

Homes come with maintenance, property taxes, insurance costs, and are harder to sell quickly. They also tie up a large portion of your net worth in one asset.

Key takeaways

- Gen Z and millennials face high barriers to homeownership.

- Stock market returns and tech-driven investing tools offer alternatives.

- Many are choosing to rent and invest to build wealth.

- Homeownership still offers long-term benefits like stability and equity.

- The best choice depends on personal goals, financial discipline, and location.

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

Share this post:

Table of Contents