Are Home Improvement Loans Tax Deductible?

Last updated 03/14/2024 by

Julie Bawden-Davis

Looking to spruce up your digs with a little remodeling? You’re part of a growing trend.

If you’re planning on taking out a loan to help fund a home improvement project, you’ll be happy to know that you may also be able to score some tax savings.

In certain situations, home improvement loans are tax deductible. Let’s take a closer look.

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

Tax credit for home improvement loans

According to the IRS, you can deduct the full amount of points in the year paid on your home improvement loan, provided you meet the following six criteria:

- Your loan is secured by your main house, which is typically where you live most of the year.

- It’s an established business practice to pay points in the area where the loan was made.

- The points paid are comparable to what’s generally charged in your area (cannot be more).

- You use the cash method of accounting (as most people do) – you report your income in the year it’s received and deduct your expenses in the year you pay them.

- The points you paid weren’t in place of other amounts that generally appear on a different part of the loan settlement statement. These include title, appraisal, inspection and attorney fees, as well as property taxes.

- Any funds you provided at or before the closing of your loan — including any points paid by the seller — amount to at least as much as the points being charged.

Which home improvements are tax deductible?

If you take out certain types of home improvement loans, you can deduct the interest if you use the money to make capital improvements to your house – these are considered renovations that go beyond repair.

A home repair just brings your home back to its original condition. Capital improvements, on the other hand, prolong the life of your home, increase the structure’s value, or adapt your house to a new use.

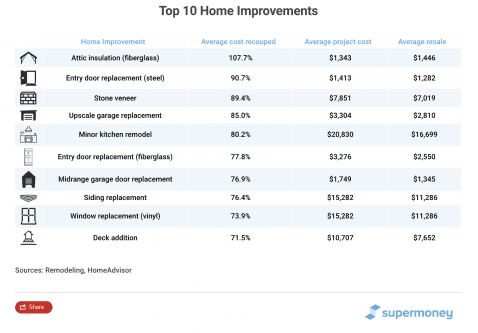

For instance, a new roof would qualify, whereas patching a leaking roof would not. According to HomeAdvisor’s Chief Economist, Brad Hunter, a new roof is your best return on investment.

Says Hunter, “According to one study, a roof replacement in many cases pays the homeowner more at resale than was invested in the project. Replacing the roof is something that many homeowners put off because it’s an expensive project. But they might not put it off if they understood how much the next owner is willing to pay for that work.”

Other capital improvements include adding a new garage door, fence, swimming pool, porch, deck, siding and window replacement, kitchen and bath remodel, new wood flooring, entry door replacement, manufactured stone veneer, basement finishing, and an addition of a master suite.

There is one exception to all of this. If your home experiences fire or damage from a natural disaster, all renovations and repairs count as a tax deduction.

Keep in mind property taxes

Before counting your tax savings, keep in mind that, if any of these changes increase the square footage of your home or lead to a significant improvement, your house could be reassessed for property taxes. Your taxes are likely to increase as a result.

When repairs are tax deductible

It’s a good idea to keep track of all repairs and renovations made in your home. This is true even if they aren’t tax deductible right now. Repairs become tax deductible when you sell your home. These home improvements are added to the tax basis of your house.

The tax basis refers to the amount of your investment in your home for tax purposes. The more improvements you’ve made, the greater your basis and the less profit you’ll get when you sell your home. This reduces the amount of tax you must pay.

Home improvement loans are also tax deductible when you buy a home. At the time of purchase, you can take out additional money to make renovations. That money is built into your mortgage. You then get tax benefits with your mortgage interest deduction.

How much can you write off for a home office?

If you qualify for a home office deduction, you can deduct 100% of the improvements you make to that office. The IRS stipulates that the home office needs to be used regularly and exclusively for business.

For instance, if you use a room in your home as your office and have shelving installed by a professional carpenter, you can deduct 100% of this cost. Improvements you make to your entire home are also depreciable.

This is based on what percentage of your home accounts for your office. For example, if 15% of your home accounts for your office, then you can depreciate 15% of a new HVAC system.

Tax deductions for rentals

If you own rental property, you can usually write off any improvements that you make to the property. Says certified financial planner Rockie Zeigler III, “Generally speaking, there may be tax benefits from improvements you make to rental properties.

Just make sure you know whether you’re able to deduct or depreciate them. I’d recommend a consultation with a competent tax advisor before proceeding with any improvements.”

Types of Home Improvement Loans

There are two general types of home improvement loans – home equity loans or lines of credit (HELOC) and personal loans.

The biggest difference between these two categories is that only home equity loans and lines of credit are tax deductible. Personal loans are not.

Personal loan

Though a personal loan doesn’t give you a tax deduction, it also doesn’t put your home in jeopardy should you have a hard time paying it off. You also don’t need equity in your home to get a personal loan for improvements.

With personal loans, the interest rates tend to be higher than home equity loans. You may also have a shorter repayment period. However, you can borrow smaller amounts with personal loans. This helps you better control your finances.

Some of the most active lenders in the home improvement space are Greensky, Sofi, LendingClub, and Lightstream. However, different personal loans come with different rates, fees and requirements, so check out what the best personal loans are to ensure that you choose the best option for you.

SuperMoney has made it easy to apply with all of them with one simple form via the SuperMoney loan offer engine.

Home equity loan/HELOC

A home equity loan and a HELOC both use your home as collateral to lend you money.

Home equity loans are essentially second mortgages for a fixed amount of money. You repay the loan via monthly payments. A HELOC is a line of credit that you can draw from. You repay only on the amount that you take out.

If you fail to repay either of these types of loans, the lender can foreclose on your home. You must also have equity in your home in order to qualify.

The good news is that both of these loan types are considered “acquisition debt” by the IRS. This is the same as your first mortgage. These loans are, therefore, tax deductible when you use the funds to make home improvements.

Where’s the best place to start?

Making home improvements is an exciting undertaking that can improve the value of your home. But with so many loan options, you may not know the best place to start.

To make sure you’re heading in the right direction, start by getting personal loan offers from competing lenders in a matter of minutes. Doing so will not hurt your credit score, and you’ll be able to quickly see what you qualify for.

Julie Bawden-Davis is a widely published journalist specializing in personal finance and small business. She has written 10 books and more than 2,500 articles for a wide variety of national and international publications, including Parade.com, where she has a weekly column. In addition to contributing to SuperMoney, her work has appeared in publications such as American Express OPEN Forum, The Hartford and Forbes.

Share this post:

Table of Contents