9 Steps to Reduce the Threat of Foreclosure

Last updated 05/20/2026 by

Teresa Ambord

Edited by

Andrew Latham

Summary:

Foreclosure rates are showing a slight increase, which can be concerning for homeowners. While foreclosure rates remain historically low, this uptick serves as a reminder of the potential challenges. If foreclosure has not affected you personally, you might know someone who has been impacted. It’s important to understand that mortgage lenders generally prefer to help you keep your home rather than repossess it, as they are not in the real estate business. They are usually motivated to work with you to rearrange your financing so you can stay in your home and continue making payments.

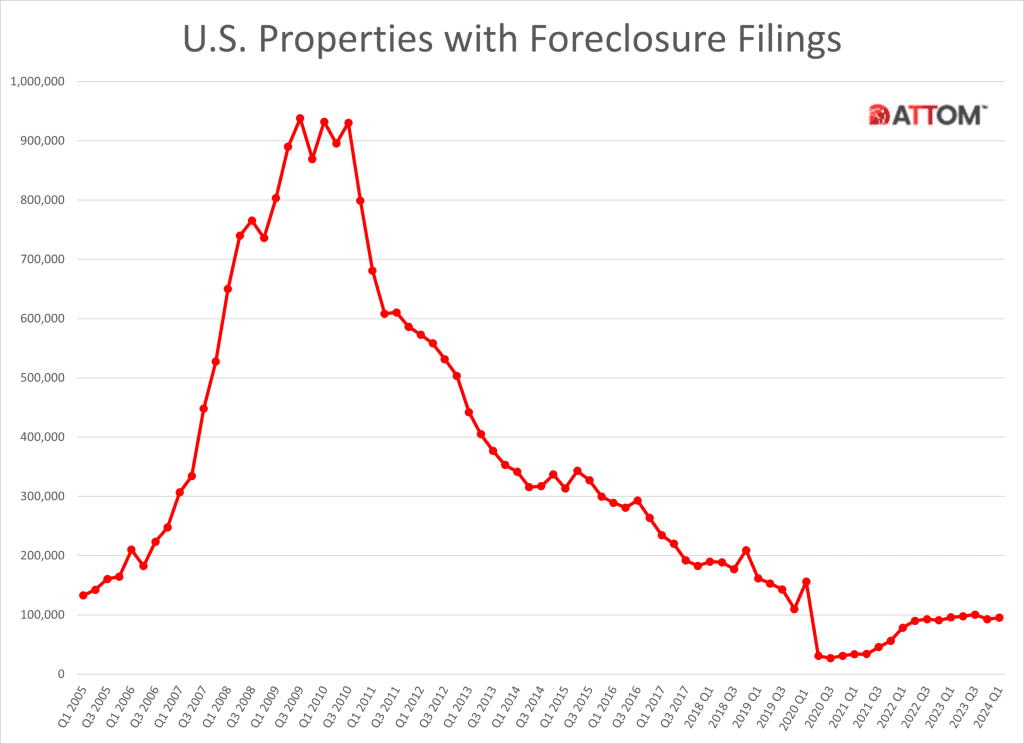

According to the ATTOM Q1 2024 U.S. Foreclosure Market Report, foreclosure filings have increased by 3 percent from the previous quarter. This slight uptick reminds homeowners of the importance of being vigilant and proactive. If you or someone you know is at risk of foreclosure, understanding your options and taking early action is crucial to protect your home.

Take control of your financial future

SuperMoney's AI-powered budgeting and personalized financial insights help you reduce financial stress and achieve your goals faster.

Reduce the threat of foreclosure

Mortgage lenders typically prefer to work with you to avoid foreclosure, as their primary interest is in helping you maintain your payments and stay in your home. Here are 9 steps you can consider if you are facing the risk of foreclosure.

1. Face the problem head-on

It won’t go away by ignoring it. The longer you wait, the harder it will be to reinstate your loan, and that’s when the danger of losing your home escalates.

2. Call your lender right away

When you realize you’ve got a problem, reach out to talk to your lender as soon as possible. Again, the bank doesn’t really want your home, so give them the best chance of helping you save it by acting early.

3. Open the scary letters

When you open your mailbox and see the letter you’ve been dreading, your knees may turn to gelatin. Resist the temptation to set the letters aside and hide—this isn’t an audit. The first letters may contain helpful information on how to prevent foreclosure, but only if you take action. If ignored, the good information turns to notices of pending legal action.

4. Determine your rights

Find the documents the lender gave you when you bought the house. These papers should explain your rights and what happens if you fail to make payments. Foreclosure laws vary by state, so you may need to contact your state’s government housing office.

5. Learn the options

Start by contacting HUD (the US Department of Housing and Urban Development) and talking to a HUD-approved housing counselor. These counselors are provided free, nationwide.

6. Prioritize spending

You may be under a boatload of debt, but make your house payment the first priority. Take a hard look at what you are spending and eliminate what you can, like cable TV and expensive phone plans, memberships. Put credit card payments and other loan payments on hold as long as you can, to get your house secured.

7. Review your other assets

If you have a whole life insurance policy, this could be a source of cash. Also look at what you can sell (a second car, expensive jewelry, etc.) to raise cash. Is there someone in the household who can get an extra job, even for a few hours a week? If you’re way behind on your mortgage, you may not be able to raise enough through these methods to get you up-to-date, but your efforts will demonstrate to your lender that you are serious.

8. Don’t get involved with a foreclosure prevention company

This will only waste money you need to pay your mortgage payments. Some of these companies are legitimate, and some are looking for the next easy buck. But legitimate or not, they may charge you a bundle for services and information you can get for free with a lender or a HUD counselor.

9. Don’t accidentally sign away your title

This may sound like a no-brainer, but there are companies that will claim to be able to halt a foreclosure process if you sign their form, allowing them to act on your behalf. Don’t believe it. The form may actually lead you to sign away your title, effectively making you a renter in your own home. To be safe, don’t sign anything without getting professional advice from an attorney, a financial professional, or a HUD housing counselor.

What if you miss a house payment?

After you miss a payment, it may take three to six months before a lender starts the foreclosure process, generally closer to three. By the time you get the first demand for payment, chances are there will already be late fees and penalties added to what you owe. So if it looks like you are not going to be able to make a mortgage payment, don’t hunker down in fear. Contact your lender right away and talk it over. Explain your situation. They may be able to extend you a grace period before they have to add fees and penalties or take legal action.

The possibility of getting a grace period quickly decreases if you try to ignore the problem. Generally, 30 days after you’ve missed a payment you will be found in default, so don’t wait, contact your lender and stay in touch. By keeping honest communication open, you can get your lenders on your side. Also, contact HUD and ask for a housing counselor. A solution still must be found, but by acting fast you are showing good faith.

Options that can help you retain your home

Don’t give up too easily. There are several programs currently available to help prevent foreclosure and assist homeowners in financial distress.

Homeowner Assistance Fund (HAF)

The Homeowner Assistance Fund (HAF) provides financial assistance to help homeowners avoid foreclosure, with funds available for mortgage payments, property taxes, insurance, and other housing-related costs.

FHA Loan Modification

The FHA Loan Modification program allows homeowners to modify their loans to make monthly payments more affordable. This can include extending the loan term, reducing the interest rate, or deferring part of the loan balance.

VA Home Loan Programs

The VA Home Loan Programs offer several options for veterans, including repayment plans, special forbearance, and loan modifications to help avoid foreclosure.

USDA Single Family Housing Guaranteed Loan Program

The USDA Single Family Housing Guaranteed Loan Program provides options for rural homeowners to avoid foreclosure through loan modifications and payment assistance.

Refinancing options

For those who are current on their mortgage but need lower payments, the FHA Streamline Refinance Program can be a viable option. This program offers reduced documentation and underwriting requirements, making it easier to refinance into a more affordable mortgage.

U.S. foreclosure activity increases quarterly in Q1 2024

In the intro we mentioned the recent increase in foreclosure filings reported by ATTOM. Here is a summary of the ATTOM Q1 2024 U.S. Foreclosure Market Report.

The report shows a total of 95,349 U.S. properties with a foreclosure filing during the first quarter of 2024, up 3 percent from the previous quarter but down less than 1 percent from a year ago.

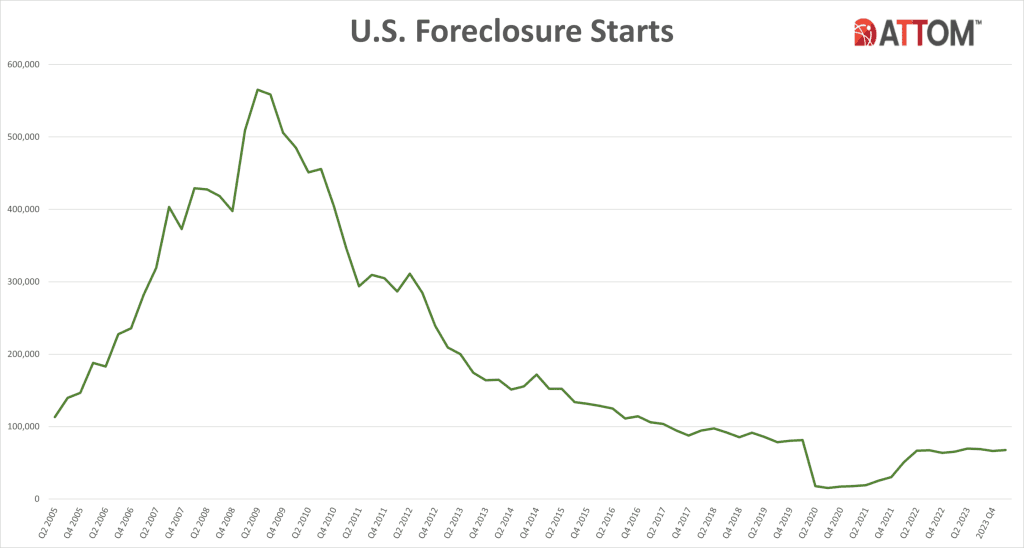

Foreclosure starts increase nationwide

A total of 67,657 U.S. properties started the foreclosure process in Q1 2024, up 2 percent from the previous quarter and up 4 percent from a year ago.

States with significant quarterly increases in foreclosure starts include:

- New Hampshire (up 43 percent)

- Illinois (up 26 percent)

- Florida (up 22 percent)

- Rhode Island (up 21 percent)

- Nevada (up 16 percent)

Major metros with the greatest number of foreclosure starts in Q1 2024 include:

- New York, New York (4,404 foreclosure starts)

- Houston, Texas (2,977 foreclosure starts)

- Chicago, Illinois (2,867 foreclosure starts)

- Los Angeles, California (2,398 foreclosure starts)

- Miami, Florida (2,319 foreclosure starts)

Highest foreclosure rates in Delaware, New Jersey, and South Carolina

Nationwide, one in every 1,478 housing units had a foreclosure filing in Q1 2024. States with the highest foreclosure rates were:

- Delaware (one in every 894 housing units)

- New Jersey (one in every 919 housing units)

- South Carolina (one in every 929 housing units)

- Nevada (one in every 961 housing units)

- Florida (one in every 973 housing units)

Among major metropolitan areas, those with the highest foreclosure rates in Q1 2024 were:

- Columbia, South Carolina (one in every 569 housing units)

- Spartanburg, South Carolina (one in 597)

- Lakeland, Florida (one in 624)

- Atlantic City, New Jersey (one in 628)

- Cleveland, Ohio (one in 662)

Bank repossessions increase 7 percent from last quarter

Lenders repossessed 10,052 U.S. properties through foreclosure (REO) in Q1 2024, up 7 percent from the previous quarter but down 20 percent from a year ago. States with the greatest number of REOs in Q1 2024 were:

- Michigan (1,049 REOs)

- California (845 REOs)

- Pennsylvania (838 REOs)

- Illinois (810 REOs)

- Texas (596 REOs)

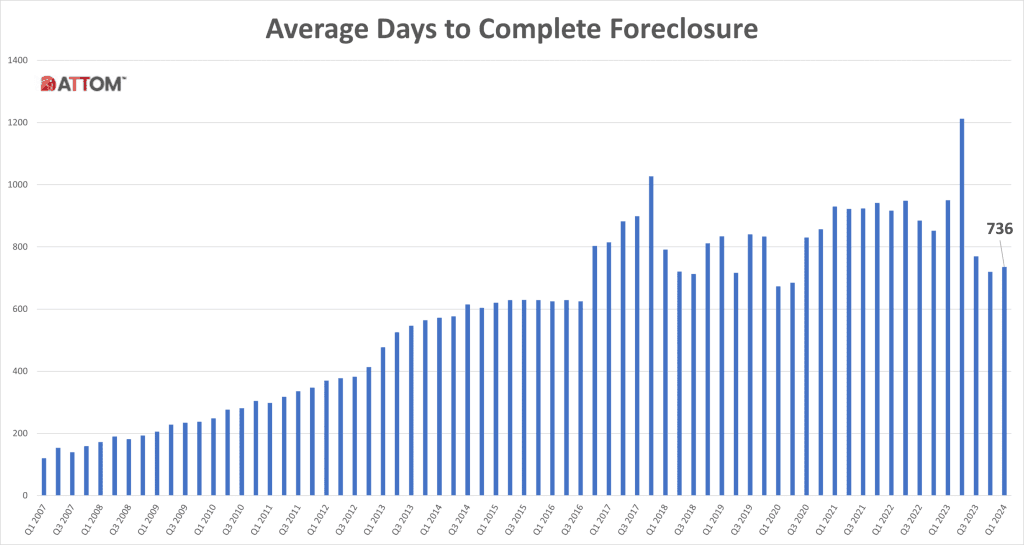

Average time to foreclose increases 2 percent from previous quarter

Properties foreclosed in Q1 2024 had been in the foreclosure process for an average of 736 days. This marks a slight increase from the previous quarter but represents a 20 percent decrease from the same time last year, continuing a downward trend since mid-2020.

States with the longest average foreclosure timelines were:

- Louisiana (2,641 days)

- Hawaii (2,031 days)

- New York (1,958 days)

- Nevada (1,701 days)

- Kentucky (1,701 days)

States with the shortest average foreclosure timelines were:

- Montana (123 days)

- Virginia (152 days)

- Texas (163 days)

- Wyoming (191 days)

- West Virginia (217 days)

March 2024 foreclosure activity high-level takeaways

Nationwide in March 2024, one in every 4,286 properties had a foreclosure filing. States with the highest foreclosure rates in March 2024 were:

- Illinois (one in every 2,548 housing units)

- Connecticut (one in every 2,609 housing units)

- New Jersey (one in every 2,638 housing units)

- Florida (one in every 2,779 housing units)

- South Carolina (one in every 2,867 housing units)

A total of 23,312 U.S. properties started the foreclosure process in March 2024, up 3 percent from the previous month but down 4 percent from March 2023. Lenders completed the foreclosure process on 2,701 U.S. properties in March 2024, down 20 percent from the previous month and down 44 percent from March 2023.

Key takeaways

- Contact your lender immediately if you are facing financial difficulties.

- Open all correspondence from your lender to stay informed about your options.

- Consider reaching out to HUD-approved housing counselors for free advice and assistance.

- Prioritize mortgage payments over other expenses to avoid foreclosure.

- Review current foreclosure prevention programs such as the Homeowner Assistance Fund (HAF), FHA Loan Modification, and VA Home Loan Programs.

- Seek professional advice before signing any documents related to foreclosure prevention.

- Foreclosure activity has increased slightly in Q1 2024, with a 3 percent rise in foreclosure filings from the previous quarter.

- States with the highest foreclosure rates include Delaware, New Jersey, and South Carolina.

- Lenders repossessed 10,052 properties in Q1 2024, marking a 7 percent increase from the previous quarter.

- The average time to foreclose increased to 736 days in Q1 2024, though this is a 20 percent decrease from a year ago.

Feeling overwhelmed by money worries?

SuperMoney's AI-powered budgeting tools help you track your money goes, set realistic goals, and reduce financial stress.

Teresa Ambord is a former accountant and a former Enrolled Agent with the IRS. Now she writes for various publications, specializing in B2B and personal finance articles. She lives in rural far northern California, and is a fully owned and operated by her posse of small dogs.

Share this post:

AddTable of Contents