90-Day Delinquencies Are Surging in 2025 —Here’s What Every Borrower Should Know

Last updated 12/01/2025 by

Andrew Latham

Summary:

Consumer debt delinquencies are rising across key loan types with student loans showing the sharpest spike after the end of COVID protections. A 90+ day delinquency signals serious financial strain. While the trend is concerning, borrowers do have tools that can help them understand their options and take control before things get worse.

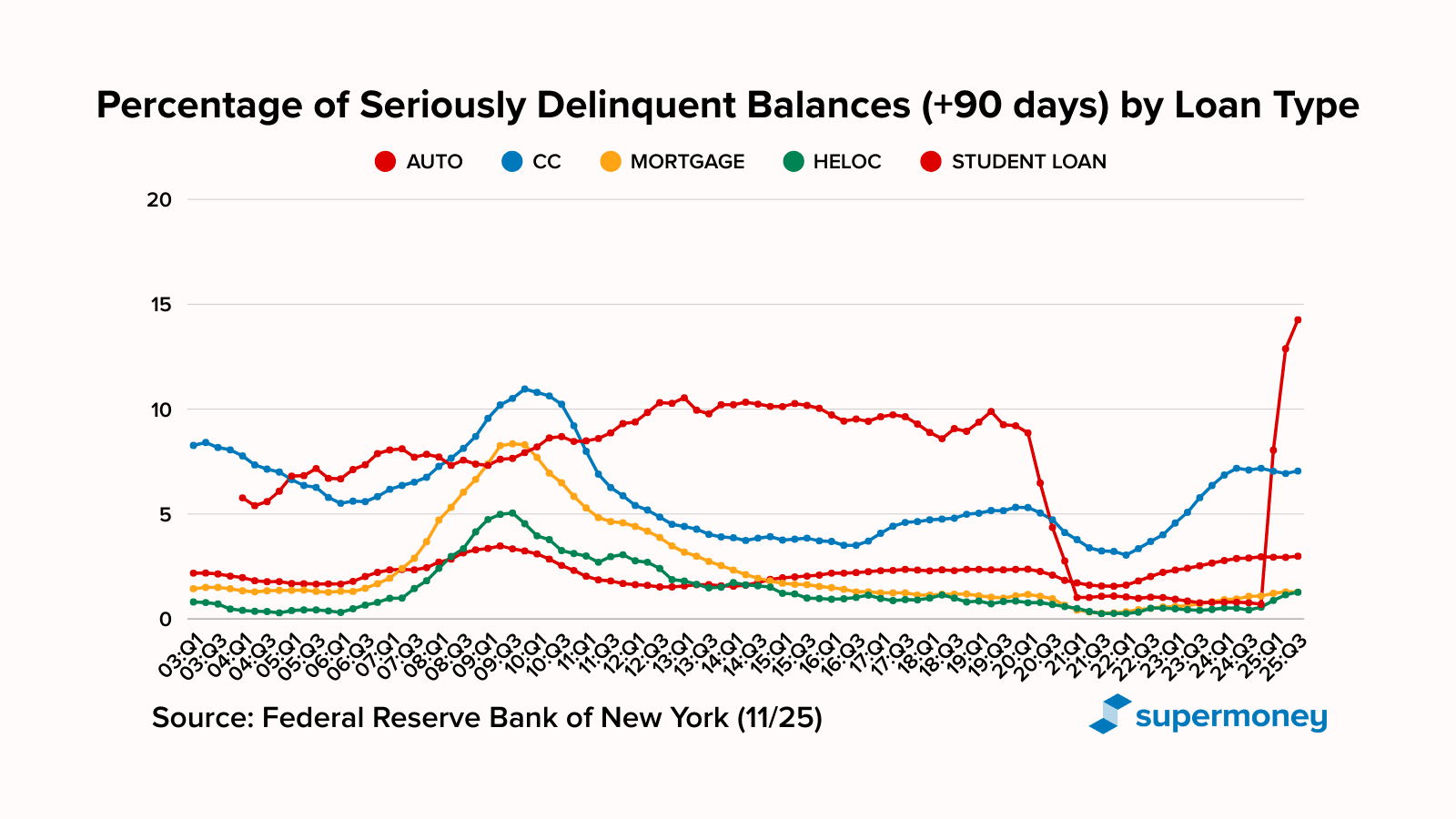

As 2025 winds down, a growing number of Americans are falling seriously behind on their debt payments — and the warning signs are getting harder to ignore. New data from the New York Federal Reserve shows an uptick in overall delinquencies to 4.5% (any stage), with 90+ day serious delinquencies particularly elevated in student loans, credit cards, and auto loans.

This trend isn’t just a data point. Serious delinquency — defined as falling more than 90 days behind on a loan — is a key signal of financial stress. It can also impact your credit score, limit future borrowing options, and increase the cost of your existing debt.

End Your Credit Card Debt Problems

Get a free consultation from a leading credit card debt expert.

It's quick, easy and won’t cost you anything.

What the data shows about 90+ day delinquencies

According to the latest Household Debt and Credit Report from the New York Fed (Q3 2025):

- Student loan delinquencies have spiked post-forbearance: the share of balances that newly fell 90+ days behind reached a record ~14.3% in Q3 2025 (four-quarter transition rate). The overall serious delinquency rate now sits at 9.4% — the highest among major loan types.

- Credit card delinquency rates remain elevated, with new transitions into serious delinquency at approximately 7.2% — the highest sustained level since the Great Recession (and over 20% in some low-income areas).

- Auto loan delinquencies are stable overall at around 2.8–3%, but low-income and subprime borrowers have seen sharper increases (up ~70 basis points in Q3).

- Mortgage and HELOC delinquencies remain historically low, though regional increases in the South are worth watching.

| Loan type | Serious delinquency rate (Q3 2025) | Transition rate (flow into 90+) | Trend |

|---|---|---|---|

| Student loans | 9.4% | ~14.3% (record high) | Sharp post-On-Ramp spike; stabilizing |

| Credit cards | ~7.1–7.2% | ~7.2% (20%+ in low-income ZIPs) | Elevated; stable in Q3 |

| Auto loans | ~2.8–3.0% | ~2.9% (higher in low-income areas) | Stable overall; rising for subprime borrowers |

| Mortgages | 0.9% | <1.0% | Historically low; some regional increases |

| HELOCs | ~3.2% (est.) | Slight uptick | Low but slowly rising |

Note: The student loan transition rate spiked because the post-COVID “On-Ramp” period ended in September 2024, allowing lenders to report previously paused missed payments.

Why 90+ day delinquencies matter

Being 90 days or more late on a payment isn’t just a missed due date. It’s a sign that a borrower may be in serious financial distress. Here’s why it matters:

- It heavily impacts your credit score, making future loans more expensive or harder to get.

- It can trigger collections activity and lead to additional fees or even legal action.

- It usually indicates chronic cash flow problems — not just a one-time oversight.

According to Federal Reserve analysis, the rise is driven by persistent inflation in essentials (rent, insurance, food), the resumption of student loan payments, higher auto payments (up ~30% since 2020), and thinner household savings buffers. Younger borrowers and lower-income households are being hit the hardest.

What you can do if you’re falling behind

1. Know your numbers

Take stock of your debt, interest rates, due dates, and total balances. Understanding where you stand is the first step to improving your financial health.

2. Look into debt consolidation

Consolidating multiple high-interest debts into one lower-interest loan could help reduce monthly payments and simplify your finances. Platforms like SuperMoney make it easy to compare your consolidation options.

3. Use technology to your advantage

Budgeting apps, such as SuperMoney’s app, can help you connect your accounts, track spending, monitor your credit, and get personalized recommendations. SuperMoney’s AI, for instance, helps identify where you might save or which options are worth exploring based on your specific circumstances and goals. There is a 2-week trial at the moment, so borrowers can check their options for free.

4. Seek help early

Waiting until you’re in collections makes everything harder. Reaching out for support early — whether from a nonprofit credit counselor or other tools — can prevent the worst outcomes.

5. Explore federal relief (especially for student loans)

Many borrowers qualify for $0 payments or forgiveness through IDR plans such as SAVE.

Frequently asked questions

What does it mean to be 90 days delinquent?

It means a borrower has missed a payment for more than three consecutive months. At this point, most lenders report the delinquency to credit bureaus and may begin collections efforts.

Which types of debt have the highest delinquency rates?

As of Q3 2025, student loans (9.4%) have the highest serious delinquency rate, followed by credit cards (~7.2%). Auto loans are lower (~3%) but rising fastest among subprime and low-income borrowers.

Does debt consolidation hurt your credit?

Applying for a new loan may cause a temporary dip. But if consolidation helps you make timely payments and lower your balances, your credit score can improve over time.

Can SuperMoney help if I’m already behind?

Yes. SuperMoney helps you compare debt relief options — including consolidation loans and other strategies — and its app can help you monitor your credit and stay on track.

Key takeaways

- Overall delinquency rose to 4.5% in Q3 2025; student loans (9.4%) and credit cards remain the most stressed categories.

- Rates stabilized for most loan types in Q3 — but low-income and younger borrowers remain under pressure.

- Debt consolidation and personal finance tools like SuperMoney’s app can help you take control before things spiral.

- Understanding your options early can help reduce stress and protect your long-term financial health.

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

Share this post:

Table of Contents