Americans Fear Running Out of Money More Than Death. The Real Problem Isn’t What You Think.

Last updated 05/06/2026 by

Andrew Latham

Edited by

Ante Mazalin

Summary:

A new Allianz survey finds that 67% of Americans now fear running out of money more than they fear death. The number keeps climbing every year. But here is the part that almost no one is reporting: half of Americans flat-out guessed at their retirement number, and only 23% have a written financial plan. The fear has two pieces. The math piece is real. The clarity piece is fixable in about three hours of work this week.

The fear is real. The cause is fixable.

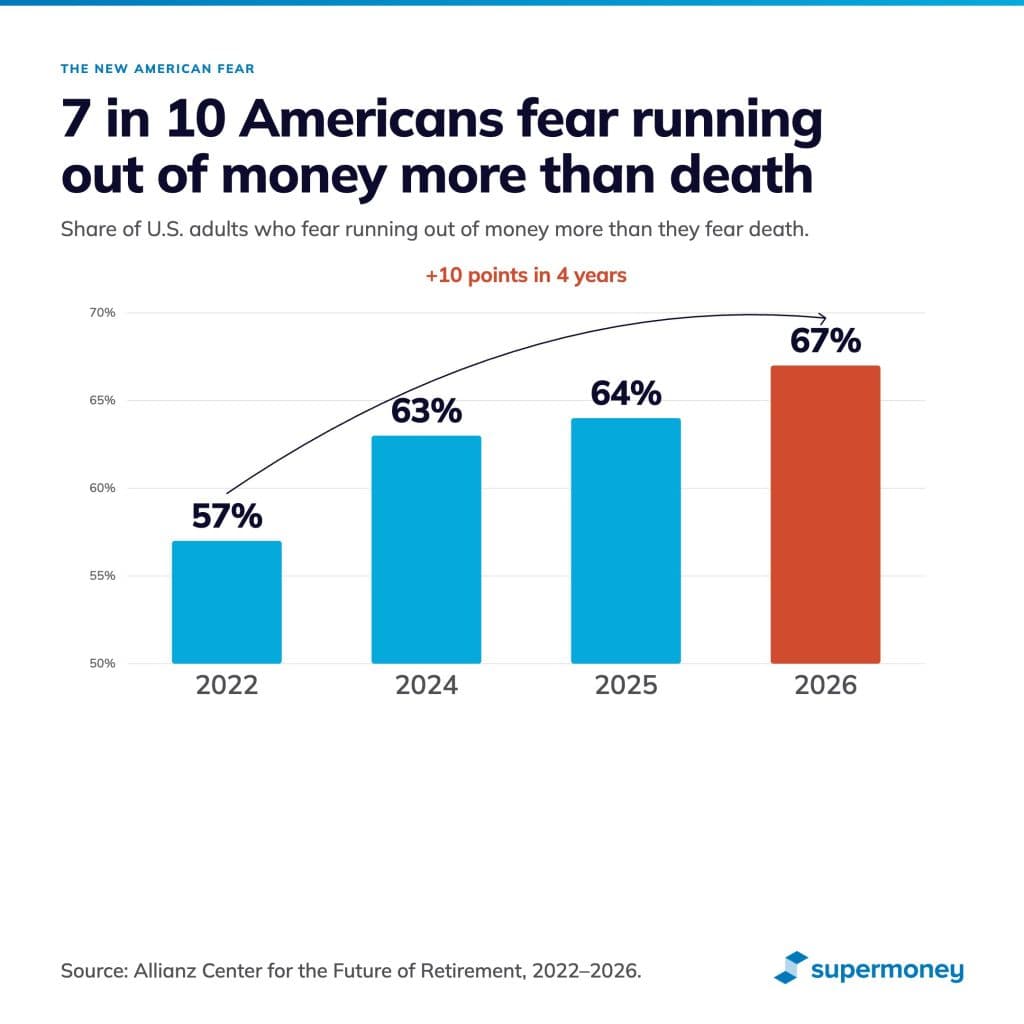

The Allianz Center for the Future of Retirement just released its 2026 Annual Retirement Study, and the headline finding is striking. Sixty-seven percent of Americans now worry more about running out of money than they worry about dying. And that number has climbed every year Allianz has run the survey: 57% in 2022, 63% in 2024, 64% in 2025, and 67% this year.

There are real reasons for concern. Inflation has compounded. Long-term care is expensive. The average assisted living facility now charges $6,200 a month, according to CareScout. Social Security trustees project a funding shortfall as soon as 2032, and if Congress does nothing, retirees would see roughly a 28% cut in monthly benefits. Life expectancy at birth hit 79 years in 2024. The math has gotten harder, and feeling uneasy about it is a reasonable response.

The fear is rarely about the numbers themselves. It is ©about not knowing them. And the not-knowing part is fixable. Three hours of homework this week, or about five minutes inside the right app, and the panic shrinks into a problem you can actually solve.

Most of us are flying blind

The Transamerica Institute’s Life & Money Report 2026, which surveyed more than 10,000 Americans, ranked our top retirement fears. The top three:

- Declining health that requires long-term care (39%)

- Social Security being reduced or eliminated (38%)

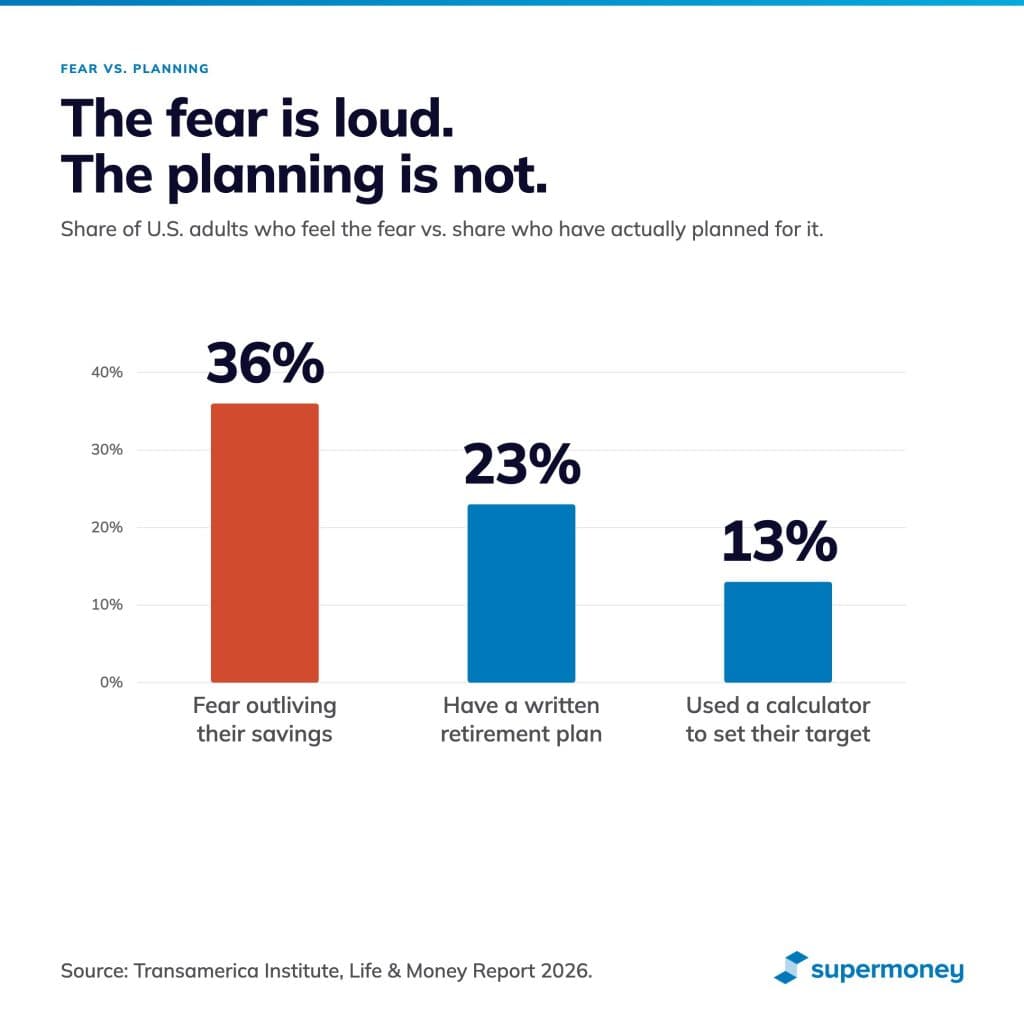

- Outliving savings and investments (36%)

Notice something? The top three fears are all about money. Even the long-term care fear is really a money fear in disguise. Most people are not afraid of needing care. They are afraid of how to pay for it.

Now look at the planning side of the same survey.

- Only 23% of Americans have a written financial strategy for retirement.

- 33% have no plan at all.

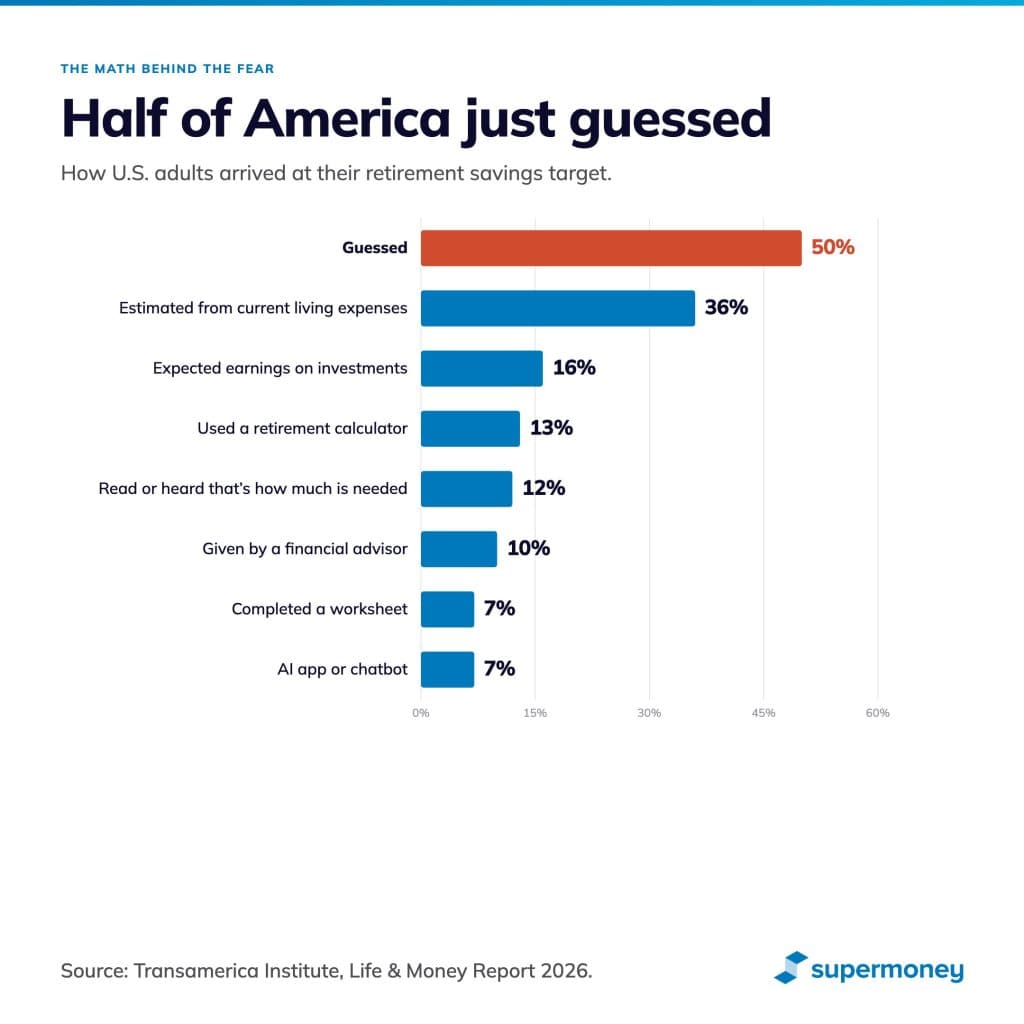

- Among the people who could even guess at how much they will need, half said they literally guessed. Only 13% used a retirement calculator. Only 12% got the number from a financial advisor.

- 64% admit they don’t know as much as they should about retirement investing.

- 45% prefer not to think about it until they get closer to retirement.

That last bullet is the part that should keep you up at night, not the size of your 401(k).

Most Americans are afraid of a number they have never calculated, based on a plan they have never written, while actively avoiding the subject. That is not a money problem. That is a clarity problem. And it makes the money problem feel ten times worse than it actually is.

Why uncertainty makes everything feel worse

Behavioral economists call this the ambiguity effect. People consistently choose a known risk over an unknown one, even when the known risk is mathematically worse. A specific bad outcome you can see is easier to live with than a vague bad outcome you can’t.

“I am $180,000 short of my retirement target” is a problem with solutions. Save more. Work two extra years. Cut retirement spending. Move somewhere cheaper. Pick a combo and start running it.

“I might run out of money someday” is a feeling. It has no solutions because there is nothing concrete to push against. So the feeling sits there, leaking stress into every news headline and every market dip.

The Transamerica report shows this disconnect playing out in real time. The median American thinks they need $500,000 saved by retirement. Sounds reasonable. Then you read the next chart and find out half of those people just guessed. Twenty percent think they will need less than $100,000. Forty-one percent think they will need more than $1 million. Almost nobody actually knows.

The four numbers that change the conversation

You don’t need a financial advisor to start. You need a quiet hour, your bank statements, and a willingness to look at what is already there.

1. Your annual retirement spending estimate

The shortcut: Pull 12 months of bank and credit card statements, total what you actually spent, then adjust for what changes in retirement (no commute, mortgage paid off, no payroll taxes). Time: about an hour.

Most retirees spend somewhere between 70% and 85% of their pre-retirement income, according to research from Aon and other plan consultants. Spending tends to run higher in the first decade of retirement when people travel, then taper, with a possible bump for healthcare in the final years.

Skip the guessing. If you make $90,000 and spend $70,000 today, plan for retirement spending of roughly $50,000 to $60,000, after adjusting for what changes (mortgage paid off, no commute, no payroll taxes) and what does not (groceries, utilities, insurance, the streaming subscriptions you forgot you had).

This is the single most useful hour you will spend on retirement planning.

2. Your “number” using the 4% rule

The shortcut: Multiply your annual retirement spending by 25. If you need $60,000 a year, your number is $1.5 million. Time: two minutes.

The 4% rule comes from financial planner William Bengen’s research and the follow-up Trinity Study. The basic idea: in year one of retirement, you withdraw 4% of your portfolio. Each year after, you adjust that dollar amount for inflation. Historically that withdrawal rate has held up over 30-year retirement windows in the vast majority of market scenarios.

If you need $60,000 a year from your portfolio, your number is $1.5 million. If Social Security covers a chunk and you only need $40,000 from your portfolio, your number drops to $1 million.

The 4% rule is not gospel. Recent research from Morningstar suggests something closer to 3.7% may be safer for new retirees facing low bond yields and stretched equity valuations. Bengen himself has said current conditions might support higher rates. Use 25x as a starting target, not a finish line.

3. Your Social Security estimate

The shortcut: Log in at ssa.gov and pull your estimated benefit. Subtract annual Social Security from your annual spending to find what your portfolio actually has to cover. Time: five minutes.

The average retired worker collected about $1,976 a month in 2025, but your number depends entirely on your earnings history and your claiming age. Look it up.

Worried about the 2032 funding shortfall? Reasonable. Plan for the cut. If your estimated benefit is $2,400 a month, model what happens if it drops to about $1,728 (a 28% cut). That is not pessimism. That is planning.

Then plug Social Security into your spending estimate. Annual spending minus annual Social Security equals what your portfolio actually has to produce.

Example: $60,000 in retirement spending, minus $24,000 in Social Security, equals $36,000 your portfolio has to cover. Apply the 25x rule. Your real target drops from $1.5 million to $900,000.

Watch how fast the fear shrinks when the math gets specific.

4. Your current retirement balance

The shortcut: Add up every retirement account: 401(k)s, IRAs, brokerage accounts earmarked for retirement, pension lump sums. Skip your home equity. Time: 20 minutes.

A house you live in is not a retirement asset until you sell it or take a reverse mortgage, both of which come with their own complications.

For context, the median household retirement savings for non-retired Americans is just $56,000, according to Transamerica. If you are above that, you are doing better than most. If you are below it, you have company. Either way, the gap between where you are and where you need to be is your real problem.

It is also solvable.

Three ways to close the gap

Once the gap is visible, you have three levers to pull. Most people use some combination.

Save more. The 2026 401(k) contribution limit is $24,500, with a $8,000 catch-up at 50, and a “super catch-up” of $11,250 for ages 60 to 63. IRA limits are $7,500 with a $1,100 catch-up. Even outside maxing those, an extra $300 a month for 20 years at a 7% return grows to roughly $156,000.

Work longer. Every extra year of work does three things at once. It adds savings. It delays the start of withdrawals. And if you delay claiming Social Security past full retirement age, your benefit grows roughly 8% per year up to age 70. That is one of the highest guaranteed returns you will find anywhere.

Spend less in retirement. Cutting annual spending by $5,000 reduces your target number by $125,000 (using the 25x multiplier). Moving from a high-tax state to a no-tax one, paying off the mortgage before you retire, downsizing the house: each move chips away at the gap from the spending side instead of the saving side.

The point is not to find the perfect plan. It is to pick a plan, any plan, and start running it.

What to do this week

If you read this and do nothing, the fear stays. So pick three small actions you can finish in seven days.

Three steps. One week. Less fear.

1. Pull your Social Security statement at ssa.gov. Five minutes if you have an account. Fifteen if you need to set one up.

2. Add up your retirement balances. 401(k)s, IRAs, brokerage accounts you have earmarked for retirement. Twenty minutes if your accounts are scattered. Two if you already track them in one place.

3. Estimate your annual spending from your last three months of bank and credit card statements, then multiply by four. About an hour.

That is the foundation. You will know more about your actual retirement situation than the 50% of Americans who just guessed.

You don’t need a CFP to do any of this. You need to look at your own information honestly. If you’d rather skip the manual work, SuperMoney’s free trial gives you the same picture in a few minutes: link your accounts, the app pulls your balances, estimates your spending from your transactions, and shows you where you stand. You can get the clarity for free and decide afterward whether the app is worth keeping.

The five-minute version

Clarity is the antidote to this fear, and you don’t have to spend a Saturday building a spreadsheet to get it. The SuperMoney app does the same exercise I just walked you through in a few minutes. Link your accounts and the app pulls your retirement balances, estimates your annual spending from your actual transactions, factors in your Social Security number, and shows you the gap between where you are and where you need to be. Then SenseAI, SuperMoney’s AI assistant, walks you through what to do about it.

Same four numbers. Same math. The difference is you don’t have to dig through six logins or build a spreadsheet from scratch. Get the SuperMoney app and stop being one of the 50% who guessed.

Key takeaways

- 67% of Americans now fear running out of money more than they fear death, up from 57% in 2022 and climbing every year Allianz has run the survey.

- The top three retirement fears are all financial: declining health requiring long-term care (39%), Social Security cuts (38%), and outliving savings (36%), per the Transamerica Institute’s Life & Money Report 2026.

- Only 23% of Americans have a written retirement plan, 33% have no plan at all, and among those who guessed at their savings target, half admitted they literally just guessed.

- The median American household has $56,000 saved for retirement (non-retired); among current retirees, total household savings excluding home equity sits at $126,000 (median).

- The 4% rule says your retirement target is roughly 25 times your annual retirement spending after Social Security and any pensions.

- If Congress does nothing, Social Security trustees project a 28% benefit cut starting around 2032; delaying your own claim past full retirement age boosts benefits roughly 8% per year up to age 70.

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

Share this post:

Table of Contents