It’s Not Just You: Auto Insurance Premiums Are Out Of Control. Here’s What You Can Do About It

Last updated 03/28/2025 by

Andrew Latham

Fact checked by

Ante Mazalin

Summary:

Auto insurance premiums are climbing rapidly nationwide, with rates rising over 35% in just three years. From inflation to advanced vehicle tech, several factors are driving costs higher. This article breaks down why your rates are going up and offers tips on how you can save money on your policy.

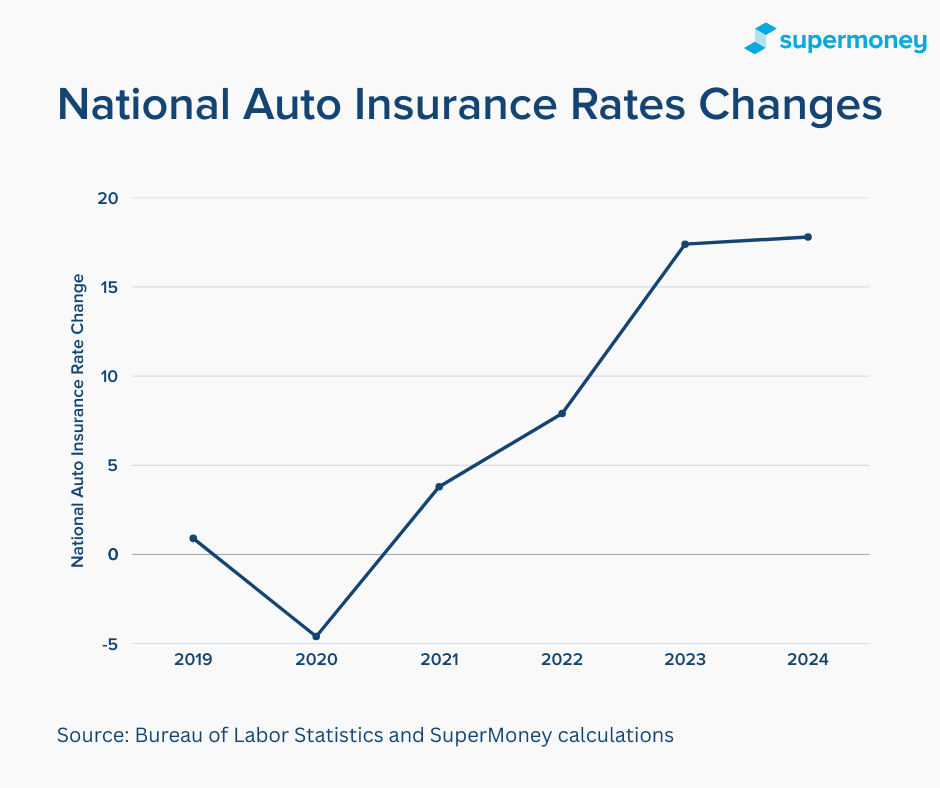

According to the Bureau of Labor Statistics (BLS), the cost of motor vehicle insurance has surged over the past four years. From 2020 to 2024, prices rose by a compounded 54.9%, with annual increases of 3.8% (2021), 7.9% (2022), 17.4% (2023), and 17.8% (2024).

If you were paying $100 per month in 2020, that same policy would cost $154.9/month in 2024 — without any changes to your coverage or driving record.

Compare Auto Insurance Providers

Compare multiple vetted providers. Discover your best option.

What’s driving the spike in auto insurance premiums?

There are several factors, as we will see, but your ZIP code plays a major role in your premium. In 2025, these are some of the most and least expensive states for full coverage:

- Most expensive: Nevada ($286/month), Florida ($272), Michigan ($263)

- Most affordable: Maine ($103/month), New Hampshire ($106), Vermont ($107)

Here is a full breakdown of the average monthly cost of insurance by state and how it compares the nationwide average.

| State | Avg monthly rate | % from average |

|---|---|---|

| Nevada | $286 | 64% |

| Florida | $272 | 56% |

| Michigan | $263 | 50% |

| Louisiana | $249 | 42% |

| Colorado | $241 | 38% |

| Rhode Island | $237 | 35% |

| Delaware | $230 | 31% |

| Arizona | $218 | 25% |

| Oklahoma | $200 | 14% |

| New Jersey | $199 | 13% |

| Kentucky | $198 | 13% |

| Washington, D.C. | $198 | 13% |

| Connecticut | $194 | 11% |

| Alabama | $194 | 11% |

| Arkansas | $193 | 10% |

| New York | $190 | 8% |

| Utah | $189 | 8% |

| Oregon | $185 | 6% |

| Montana | $185 | 6% |

| Georgia | $183 | 4% |

| Texas | $182 | 4% |

| Illinois | $179 | 2% |

| Kansas | $175 | 0% |

| South Dakota | $173 | -1% |

| Pennsylvania | $172 | -2% |

| Minnesota | $170 | -3% |

| Maryland | $170 | -3% |

| Missouri | $170 | -3% |

| New Mexico | $170 | -3% |

| California | $168 | -4% |

| Mississippi | $164 | -6% |

| Nebraska | $161 | -8% |

| Iowa | $159 | -9% |

| Washington | $159 | -9% |

| North Dakota | $158 | -10% |

| Tennessee | $157 | -10% |

| South Carolina | $151 | -14% |

| West Virginia | $149 | -15% |

| Massachusetts | $145 | -17% |

| Alaska | $141 | -19% |

| Virginia | $140 | -20% |

| North Carolina | $139 | -20% |

| Wisconsin | $135 | -23% |

| Indiana | $130 | -26% |

| Hawaii | $124 | -29% |

| Wyoming | $124 | -29% |

| Ohio | $115 | -35% |

| Idaho | $111 | -37% |

| Vermont | $107 | -39% |

| New Hampshire | $107 | -39% |

| Maine | $103 | -41% |

These quotes are for a 30-year-old man who drives a 2015 Honda Civic EX with good credit and a clean driving record. Quotes include the largest companies in each state from all available ZIP codes.

Why rates are rising

Several factors are fueling the rise in auto premiums:

- Increased vehicle costs: Cars are more expensive than ever, and so are repairs and replacements.

- Advanced tech, higher repair bills: Features like sensors and cameras improve safety — but they cost more to fix.

- Inflation: The cost of car repairs, parts, and medical services has risen with inflation, boosting claims costs.

- Riskier roads: More distracted driving and higher accident rates have pushed insurers to raise premiums.

Impact of mileage and driving habits

Your driving habits and annual mileage significantly impact how much you pay for car insurance. Insurance companies view drivers who spend more time on the road as higher risk, since increased mileage raises the chances of an accident.

For example, drivers averaging fewer than 7,500 miles per year typically qualify for low-mileage discounts that can reduce premiums by up to 10% or more. Additionally, adopting safer driving habits—such as avoiding late-night drives, heavy traffic hours, and maintaining a steady speed—can lead to savings through usage-based insurance (UBI) programs, which track driving behavior via smartphone apps or telematics devices.

Actionable tip:

Ask your insurer about mileage-based discounts or programs like StateFarm Drive Safe & Save® or Liberty Mutual, which reward safe, low-mileage drivers with discounted premiums.

Ask your insurer about mileage-based discounts or programs like StateFarm Drive Safe & Save® or Liberty Mutual, which reward safe, low-mileage drivers with discounted premiums.

Hidden factors that increase premiums

While most drivers know that their driving record and vehicle type influence insurance costs, fewer realize there are hidden factors insurers use to set premiums. Some of these surprising factors include:

- Marital status: Married drivers often receive lower rates due to perceived stability.

- Occupation: Certain professions (e.g., teachers, engineers, nurses, military personnel) can qualify for lower rates.

- Education level: Drivers with higher education degrees may receive discounts, based on insurers’ statistical risk assessments.

- Homeownership: Owning a home may lead insurers to offer discounts, seeing homeowners as lower risk.

Actionable tip:

When shopping around, be sure to mention your occupation, education level, marital status, or homeownership status. It may unlock unexpected discounts or lower quotes you didn’t anticipate.

When shopping around, be sure to mention your occupation, education level, marital status, or homeownership status. It may unlock unexpected discounts or lower quotes you didn’t anticipate.

How to lower your car insurance bill

While you can’t control the insurance market, there are several proven ways to save on your premium.

1. Shop around for quotes

Rates vary significantly between insurers. Comparing quotes could save you hundreds. For example, drivers of a 2020 Chevrolet Equinox L found a $1,370 difference between the average and lowest full-coverage premium. I was happy with my coverage with GEICO but compared my rates with this insurance company and was able to lower my rate and increase my coverage.

- Check your current policy.

- Make a note of your current coverages and the total cost.

- Compare three to five other providers and see what offers you get.

2. Boost your credit score

In most states, insurers use credit scores to set rates. Drivers with poor credit can pay nearly twice as much as those with good credit. Improving your score could unlock big savings.

Your credit score directly impacts your car insurance rates. Regularly monitoring your credit can help you spot inaccuracies or fraud early, protecting your score and potentially lowering your premiums. Consider a trusted credit monitoring service to stay informed and secure.

3. Take advantage of discounts

Ask your insurer about available discounts. Common ones include:

- Safe driving courses: Completing a defensive driving class can lower rates by up to 10%. In New York, it can save drivers 10% for three years.

- Bundling policies: Combine auto and home insurance for discounts. Some providers offer savings of up to 24%.

4. Raise your deductible

Opting for a higher deductible can lower your monthly premium. Just make sure it’s an amount you could afford to pay in case of a claim.

5. Keep your driving record clean

Fewer accidents and violations mean lower premiums. Many insurers offer discounts for drivers who stay claim-free for a certain period.

6. Rethink coverage

Auto insurance isn’t one-size-fits-all. Whether you’re driving a brand-new SUV or a decade-old sedan, it’s worth reviewing your coverage each year to make sure it still fits your needs and budget.

For some drivers, especially those with older cars, dropping comprehensive or collision coverage might make sense if the premiums outweigh the potential payout. But even newer car owners might find they’re overinsured—or underinsured—depending on how much they drive, where they live, and their personal risk tolerance.

The table below shows how full coverage compares to minimum state-required coverage for a 2023 Toyota Camry, just one example of how your choices can affect your rates.

| Alabama | $173 | $42 |

| Alaska | $200 | $41 |

| Arizona | $228 | $68 |

| Arkansas | $207 | $42 |

| California | $245 | $70 |

| Colorado | $268 | $49 |

| Connecticut | $222 | $85 |

| Delaware | $241 | $89 |

| Florida | $351 | $95 |

| Georgia | $248 | $88 |

| Hawaii | $142 | $34 |

| Idaho | $123 | $31 |

| Illinois | $204 | $56 |

| Indiana | $146 | $37 |

| Iowa | $157 | $27 |

| Kansas | $213 | $48 |

| Kentucky | $238 | $64 |

| Louisiana | $333 | $86 |

| Maine | $138 | $36 |

| Maryland | $236 | $84 |

| Massachusetts | $172 | $44 |

| Michigan | $263 | $73 |

| Minnesota | $215 | $61 |

| Mississippi | $196 | $44 |

| Missouri | $217 | $55 |

| Montana | $202 | $34 |

| Nebraska | $200 | $43 |

| Nevada | $305 | $96 |

| New Hampshire | $154 | $41 |

| New Jersey | $245 | $106 |

| New Mexico | $183 | $36 |

| New York | $341 | $145 |

| North Carolina | $163 | $50 |

| North Dakota | $151 | $33 |

| Ohio | $149 | $39 |

| Oklahoma | $229 | $47 |

| Oregon | $175 | $73 |

| Pennsylvania | $203 | $43 |

| Rhode Island | $212 | $66 |

| South Carolina | $164 | $53 |

| South Dakota | $192 | $31 |

| Tennessee | $174 | $43 |

| Texas | $214 | $60 |

| Utah | $177 | $67 |

| Vermont | $126 | $27 |

| Virginia | $180 | $63 |

| Washington | $155 | $47 |

| Washington, D.C. | $251 | $74 |

| West Virginia | $185 | $47 |

| Wisconsin | $163 | $37 |

| Wyoming | $147 | $22 |

Frequently asked questions

Why are car insurance premiums increasing so much?

Insurance rates are rising due to inflation, more expensive repairs, increased vehicle prices, and higher accident rates.

Which states have the most expensive car insurance?

As of 2025, Nevada, Florida, and Michigan have the highest average premiums for full coverage auto insurance.

How much can I save by comparing quotes?

Shopping around could save you hundreds of dollars annually. Some drivers report savings of over $1,000 per year.

Does credit score really affect car insurance rates?

Yes. Drivers with poor credit often pay significantly more for auto insurance than those with good or excellent credit.

Is it safe to increase my deductible?

It can be a good way to lower your premium, but only if you have enough savings to cover the higher out-of-pocket cost after a claim.

Key takeaways

- Auto insurance premiums rose 7.5% in 2025 and over 35% in three years

- Factors include inflation, costly vehicle repairs, and more accidents

- Nevada, Florida, and Michigan are among the most expensive states

- Compare quotes, boost your credit, and raise deductibles to lower your premium

- Older vehicles may not need full coverage, depending on their value

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

Share this post:

Table of Contents