Average Millennial Income Is Up, But At What Cost?

Last updated 03/20/2024 by

Andrew Latham

If you are a demographic economics nerd – and why else would you be reading an article on average millennial income? – you have probably read headlines like these.

“Young adult households are now earning more than ever before.”

“Are Millenials on track to become the richest generation?”

“Millenials may be the wealthiest generation.”

But you have also seen headlines that highlight how “broke” young adults are and that they are worse off financially than their parents and grandparents were at their age. How are both of these narratives possible?

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

Why are Millennials labeled as both the richest and poorest generation?

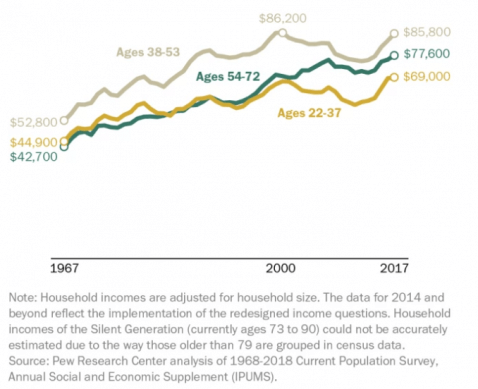

The quick answer is it depends on whethePr you look at households or individuals. Many of the recent positive headlines have been triggered by this 2018 study by the Pew Research Center and this 2018 report by the Federal Reserve Board. Both studies focus on Millennial households (not individuals), which include people born between 1981 and 1996. This graph has been widely republished to highlight the findings. The key point is that households with ages between 22 and 37 make $24K more a year than they did in 1967.

There are two main reasons for Millennials‘ “financial bonanza.

First, more young women are joining the workforce.

Second, Millennial women are getting paid more than young women in the past.

The narrowing of the gender income gap is good news. But, it is not a reflection of the financial situation of young adults as a group. On the contrary, when you dig a little deeper, they are good reasons for concern.

Just because young households have higher incomes doesn’t mean they are better off. To illustrate this, let’s look at the median income of American individuals from 1973 to 2017.

Median incomes increased for all age groups but 15-24 year-olds lost ground to their seniors

The overall growth in incomes is obvious from this data set. Notice though that young adults (25-34) practically made the same as middle-aged workers (35-54) and more than 55-64 year-olds in 1974. Fast forward to 2017 and their median income trails behind all age groups except 15-24 year-olds.

In any case, this graph is misleading because it doesn’t consider the increase in the cost of living since 1974. See what happens to the growth inclines of the previous graph when you convert the incomes into 2017 dollars.

Average millennial income growth is practically flat when you consider inflation and young adults are the worst off

Income growth is modest for all age groups but it is particularly bad for young adults (25-34) when you take into account inflation.

- Middle-age workers with ages between 45 and 54 fared the best, with income growth of nearly $5,400.

- Adults between the ages of 35 and 44 made nearly $2,900 more than their 1974 counterparts.

- However, young adults with ages between 25 and 34 saw an increase of only $29 in their incomes since 1974.

It gets worse. Compare the growth in income for young adults with the median value of home sales in 2017 dollars.

The median house price to income ratio is close to record-high levels and it’s hitting young adults the hardest

So, while the annual income of 25-34-year-olds grew by a whopping $29, the median price of house sales has grown by $127,862. In other words — taking into account inflation — home prices have increased by about 39% in the last 45 years, but the income of 25-to 34-year-olds has not changed.

Let’s not even get into healthcare costs.

National health expenditure per person has increased by $9K since 1970 after adjusting for inflation

Now consider the increase in education costs.

The cost of education has more than doubled (inflation-adjusted) but incomes for young adults are stagnant

Americans are borrowing more than ever to pay for education. Some students even take out personal loans to help cover living expenses. And for good reason. Workers who don’t have a college degree are worse off than in previous generations. In fact, education levels and their relationship to income shed some light on some of the apparent contradictions of young adults’ financial situation.

A 2019 report from the Stanford Center on Poverty and Inequality shows that 25-year-old-men with a bachelor’s degree or higher have an annual income of approximately $50K, which is slightly higher than in previous generations. Again, this sounds like good news. The payoff for attending college is as high as it has ever been. However, this is not a net win for young adults. The median income of 25-year-old men who only have a high school degree is $29K a year. That is about $2,600 less than what Generation X made, and nearly $10K less than what Baby Boomers earned at the same age.

If you ignore student debt, which is a $1.5 trillion blind spot, young adults with a college degree are slightly better off than previous generations. Those who don’t have a college education are in a much worse situation than their parents and grandparents.

The financial situation of the Millennial generation does not fit a simple narrative

Overall, the median income of young adults hasn’t changed in 45 years, but the cost of housing, education, and healthcare have never been higher.

For men, the Millennial gloom and doom narrative is not far-fetched. The median income of young men is lower than those of Generation X when you consider inflation.

However, the American Dream lives on for women who are seeing a steady generational improvement in their median income. The gender income gap between young men and women has narrowed. This has helped increase the incomes of households, but whether it makes them better off financially is a more complicated story. Homeownership rates are lower than in previous generations. Among other things, you can blame student debt, and high prices in coastal cities where the best jobs are found.

For a generation that is often portrayed as privileged, the Millennial population is bearing an unprecedented burden of cost inflation. It explains why Millennials are more likely to be concerned about consumer debt, tax debt, and taking investment risks. While real income has increased moderately for some, it’s nowhere near enough to keep up with the burden of cost inflation in key areas like home, healthcare, and tuition.

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

Share this post:

Table of Contents