Bankruptcy: The Ultimate Guide

AL

Last updated 04/26/2023 by

Andrew LathamFact checked by

The idea of bankruptcy is thrown around a lot, but few people understand what bankruptcy proceedings actually entail. You may be wondering yourself, what is bankruptcy? And is it a good option for me? We’re here to answer the key questions for you.

In 2019, there were 774,940 bankruptcy filings in United States courts, 97% of which were personal (non-business). While the number of people going through bankruptcy courts has decreased from its peak in 2013, there is still a sizeable group of people saddled with debts, from student loans to overdue taxes, that they can’t repay.

Making a filing in a bankruptcy court could be the best way to start over. But bankruptcy is a legal matter with far-reaching consequences. There are some things you should understand before taking this step.

In this ultimate guide to bankruptcy, we cover all of the major topics, including:

- How a bankruptcy proceeding works

- Explanation of each bankruptcy chapter

- The cost of filing for bankruptcy

- Alternatives to consider

Bankruptcy laws are complicated but not impossible to understand. By the end of this article, you should know what it entails and which type of bankruptcy filing would be best for you.

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

Understanding bankruptcy: How bankruptcies work

The word bankruptcy is derived from the Italian phrase “banca rotta,” which means broken bank.

Unpaid debt is the start of any bankruptcy proceeding. When individuals or businesses can’t repay those debts, they can file for bankruptcy with a federal court to discharge their qualifying obligations.

Depending on which of the bankruptcy types is being used, the solution could include a payment plan, the liquidation of assets, a reorganization of the debt, or a discharge of the debt.

What is the downside of filing for bankruptcy, and how does it affect your credit report?

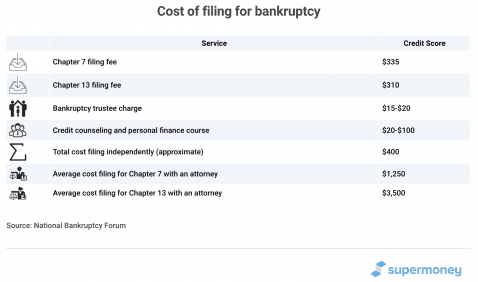

Filing for bankruptcy in the United States is not easy or painless. In fact, there are some heavy terms involved for the debtor. This person has to pay a filing fee and administrative costs. Since bankruptcy is a legal issue, they may also have to pay attorney fees.

Here’s a look at the average costs for filing:

A second consideration is that bankruptcy proceedings stay on a debtor’s record for seven to 10 years. How long depends on which of the six types a person chooses to file under.

That can make it hard for a debtor to qualify for credit, get a job, and get good insurance rates. It should be the last resort when all other avenues have been exhausted.

Who pays for bankruptcies?

The debtor pays for filing bankruptcy. They must also pay as much as possible of the debt balance to creditors by selling assets or setting up a payment plan. Any qualifying balance on the debt that can’t be paid is discharged and chalked up as a loss for the creditor.

How much debt do you need to file bankruptcy?

The amount of debt you can have in a bankruptcy case is dependent on which type of bankruptcy you are filing for. You can file under a certain type as long as you meet these restrictions.

There are terms for each, which are outlined in the U.S. bankruptcy code. The exact amount of debt can fluctuate with the consumer price index.

What do you lose if you file bankruptcy?

In some cases, filing in a bankruptcy court can result in the debtor losing their property or assets, but this isn’t always the case. The different types of bankruptcy you can choose from have different results.

While the terms of Chapter 7 allow for property loss, for instance, they don’t qualify for Chapter 13. Instead of paying with assets, you are setting up a payment plan to cover your debts.

Can you declare bankruptcy for IRS tax debts?

For people seeking debt relief related to taxes, bankruptcy is an option. As with every scenario when you file for bankruptcy, certain restrictions are in place and outlined in the bankruptcy code, but your tax debts will be treated like your other debts.

If you owe a lot of money to the IRS, enlisting a tax relief company may also be a good choice. The best tax relief companies have tax lawyers and enrolled agents on staff, provide a money-back guarantee and charge competitive rates. Check out which tax relief company is the best fit for you.

Types of bankruptcy

Now that we have a foundation for some of the general questions about bankruptcy, we can dig deeper into the different types of bankruptcy. Each situation calls for something different to be used, and what works for a business might not work for an individual. Let’s go through each bankruptcy chapter in detail.

Chapter 7 bankruptcy

Chapter 7 bankruptcy is called a “no-asset” or “liquidation” bankruptcy. This could be an option for an individual or a business. The terms for this involve a court-appointed trustee who is assigned to the case to sell the debtor’s non-exempt property and get as much repayment as possible.

In many cases, the people filing bankruptcy don’t have any non-exempt assets to sell. In this case, the trustee files a no-asset report, and the creditors don’t receive anything. If assets are sold and debts remain after the liquidation, those that qualify will be discharged.

What property is exempt?

Exemptions allow bankruptcy petitioners to keep a minimum amount of money and property to continue to support themselves with the bare necessities.

While the United States federal government has authority over bankruptcy laws, states can regulate exemptions. A debtor will have to look up the regulations and choose whether to opt for those set by the state or the federal government.

What kind of debt is dischargeable?

Debt that qualifies for Chapter 7 must be incurred before the date you file your petition and can’t be tied to any bankruptcy fraud or misconduct.

Some debts are not dischargeable, meaning they won’t go away if you file for bankruptcy. These include secured loans, child support, alimony, and student loan debt.

Unsecured debts – such as those from personal loans, medical bills, and past-due rent – will qualify for discharge.

What happens to secured loans?

Chapter 7 bankruptcy does not remove liens. If you stop making payments on a loan, the lien holder can seize your property. However, bankruptcy can discharge repossession deficiency balances.

Are there eligibility requirements?

To qualify for Chapter 7, the monthly income for individuals throughout the six months before their filing date must be less than the median income for a household of their size in the state.

Additionally, you must pass the “means test.” This requires your disposable income to be under certain limits (after deducting certain expenses and monthly payments that would be required in chapter 13). Some exceptions for this apply.

If you don’t qualify, you will have to file Chapter 13.

Chapter 13 Bankruptcy

The second major bankruptcy filing type, Chapter 13 Bankruptcy, involves individuals or businesses submitting a bankruptcy repayment plan to the court, which usually lasts three to five years.

This plan requires the full repayment of certain debts (alimony, child support, taxes, secured debt, etc.). Any leftover disposable income is used to make payments on unsecured debts.

Although this option often takes longer and can cost more, it allows you to keep some of the property you’d lose in filing bankruptcy using Chapter 7. When the payment plan is complete, all eligible debts can be discharged.

The dischargeable debts are broader with Chapter 13, but as with Chapter 7, debts tied to bankruptcy fraud or other misconduct are not dischargeable.

Other bankruptcy options

In addition to Chapter 7 and Chapter 13, four other less common bankruptcy chapters exist:

Chapter 9 Bankruptcy

Allows municipalities (school districts, counties, cities, etc.) to reorder their debt and create a reimbursement strategy.

Chapter 11 Bankruptcy

Open to businesses and individuals but primarily for businesses that exceed the limits of Chapter 13. Chapter 11 bankruptcy is the only other option for individuals.

Chapter 12 Bankruptcy

For family farmers or fisherman who meet the conditions.

Chapter 15 Bankruptcy

For any foreign debtor (or related parties) that files for bankruptcy in another country and need access to United States courts.

No matter which option you choose, any individual filing for bankruptcy must take a debtor education course and credit counseling before they can be discharged according to the bankruptcy code.

“Chapter 20 Bankruptcy”

A debtor could also benefit from what is known as Chapter 20 Bankruptcy. This is not an actual bankruptcy chapter. It’s a strategy. Chapter 20 is the informal term when a debtor files Chapter 7 with a bankruptcy court and immediately after files for Chapter 13.

This makes sense when you have large debts that can’t be discharged and large amounts of dischargeable debts, such as medical bills. Chapter 7 takes care of the unsecured debts. In contrast, the protections of Chapter 13 Bankruptcy allow you to qualify for affordable payments on non-dischargeable debts without having to worry about creditors calling.

For more information on all of these bankruptcy types, you can refer to the bankruptcy code. While many types of bankruptcy filings exist, the majority of United States citizens will fall under either Chapter 7 or Chapter 13.

Alternatives to bankruptcy

Now that you understand more about bankruptcy law, you may have a clear idea of how it fits in with your situation. If you feel that declaring bankruptcy is not right for you, there are some other actions you can take to handle your debt.

Debt settlement

Debt settlement involves an agreement with creditors in which you pay less for the debt than you owe. This option is usually only available on unsecured debts, and creditors won’t settle if they think you can pay.

For this option to work, you typically have to be behind on payments. When you hire a debt settlement agency, they will have you stop paying your creditors and instead put your payments into a savings account.

When the amount is large enough to make a lump-sum offer, they will contact the creditors and agree on a debt repayment plan. If the creditor agrees, the amount is paid from the savings, and the debt is settled. You may have to pay taxes on forgiven debt, however.

The downside is that when you stop making payments, you rack up fees and interest. The missing payments are reflected on your credit report, which will cause your score to drop.

The debt settlement company will also charge you a fee for its services. In cases where creditors don’t accept a settlement, individuals could end up with a larger debt and hurt their credit scores for no reason.

Debt consolidation

You can also get some debt relief by consolidating your debt. The idea here is that you get a new loan (a home equity loan, line of credit, personal loan, or balance transfer credit card), and you use it to pay off your old loans.

This can benefit you if you qualify for a loan with a lower overall cost than your existing loans combined. It can also make your debt easier to manage as you have one creditor instead of multiple.

Going this route, you won’t have any debt discharged or forgiven, but you can save your credit. The catch is that you will have to find a loan that is large enough to cover your debts.

If you can’t find such a loan, or if your debt is beyond what you can repay in three to five years, it’s probably better to look into bankruptcy or debt settlement.

Tax Relief

In some cases, if you owe a lot of money to the IRS, it can help to have a tax relief company on your side. The best tax relief companies have tax lawyers and enrolled agents on staff, provide a money-back guarantee and charge competitive rates. Check out which tax relief company is the best fit for you.

Bankruptcy: Is it right for you?

Finding the right solution for you will require analyzing your current situation and weighing each option’s benefits and disadvantages. A good place to start is seeing if you can get pre-approved for a debt consolidation loan and figuring out if you can manage the payments. If debt consolidation doesn’t work, debt settlement, Chapter 7 Bankruptcy, and Chapter 13 Bankruptcy can offer relief.

There is a lot to consider when choosing the right debt relief option. Here is a summary of the three most common debt relief options.

- Debt settlement can help you settle your debt for less while avoiding bankruptcy, but it takes two to three years. Negative marks will stay on your credit report for seven years, and there are no guarantees that a settlement will occur.

- Chapter 7 Bankruptcy will help qualifying individuals or businesses discharge many of their debts within three to six months, but it will follow them for 10 years.

- Chapter 13 can enable a business or individual with more income and assets to keep them while paying back what they can afford. Payment plans last 3-5 years, and the bankruptcy follows them for seven years.

Each case is unique, so it is important to make sure you are using the right tool for your circumstances. Talking to a tax professional or credit counseling firm can help you decide the best option for you.

AL

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

Share this post: