How to Calculate the APR of a Loan

Last updated 04/16/2024 by

Andrew Latham

The key question to ask when comparing loans is, “how much will this cost me?” Learning how to calculate the APR of a loan will allow you to compare apples to apples when searching for the best deal available. The problem is millions of borrowers don’t even know what an APR is.

So, how do you calculate the annual percentage rate (APR) of a loan? Is it the same method for all loans?

Let’s start with some background.

The Truth In Lending Act mandate of APR disclosure

In 1968, Congress passed the Federal Truth in Lending Act. The law introduced the concept of the APR, a game-changer for the credit industry.

Before this act was passed, lenders used a variety of misleading and inconsistent methods to calculate interest. Now, most lenders must disclose the total cost of loans by providing potential borrowers with an APR.

However, some lenders prefer not to disclose the APR of their products and instead advertise the cost as a flat fee or monthly interest. This article will teach you how to calculate the APR of the main loan products available.

What is the Difference Between APR and Interest Rate?

The Annual Percentage Rate (APR) is the cost you pay each year to borrow money, including additional fees, expressed as a percentage. The higher the APR, the more you’ll pay over the life of the loan term.

The interest rate of a loan also describes the yearly cost of borrowing money, but it does not include additional lender fees. For that reason, your APR is usually higher than your interest rate.

In other words, an annual percentage rate (APR) is a broader measure of the cost of borrowing money that includes the interest rate and additional closing costs. These fees vary depending on the type of loan but can include origination fees, broker fees, points, and any other charge you’ll pay that is required to pay to get the loan.

APR Vs. Interest Rate – An example

Let’s illustrate the difference between an interest rate and APR with a home loan. Imagine you apply for a $162K mortgage with a 30-year loan term. The interest rate is 3.87%, but the lender charges you $1,802 in closing costs. The APR of the mortgage would be 4.27%.

Confusing APR and interest rate here could cause you to underestimate the cost of the mortgage by 0.4% when comparing it to other mortgages. A 0.4% difference in this loan represents just over $13,500 in total interest paid, which also increases your monthly payment. As you can see, confusing interest rate with APR when comparing loans can be an expensive mistake.

| Loan Amount | Interest Rate | Loan Costs | APR |

|---|---|---|---|

| $162,000 (30-year term) | 3.87% | $1,802 | 4.27% |

Why an Annual Percentage Rate Can be Misleading

Many lenders feel that requiring APR disclosure is unfair because it makes short-term loans look more expensive than they are, and long-term loans feel cheaper.

Payday loans, for instance, only have a loan term of 14 to 30 days. As such, lenders say, it’s misleading to convert a fixed fee for a short-term loan into a hypothetical annualized rate.

An example that illustrates this view is the taxi and airplane analogy. A 500-mile flight on an airplane might cost $500, or $2/mile, while a one-mile taxi ride in Los Angeles will cost about $10, or $10/mile. Does this mean that taxis are overpriced? No, most would argue — it’s just a different type of service. To require both of these services to report their costs in the same way (dollars per mile) would overstate the cost of the taxi ride. Similarly, lenders argue, it’s unfair to require payday lenders to report an annualized rate.

Why APRs are Useful

But there’s a problem with the taxi argument. Taxi drivers do provide customers with a mile rate, and people still ride cabs. Similarly, mortgage loans don’t quote their interest rates over 30 or 15 years, and auto loans don’t give 5-year interest rates. They both use the annual rate. Customers realize they are different types of loans and terms. But having a benchmark rate to compare all loans makes it easier to compare the cost of the options available.

For example, if you qualify for a credit card with a 20% APR and a payday loan with a $15 fee for every $100, you may wonder which is the best deal. But if you compare their APRs (20% and 391%, respectively), it becomes clear that credit cards are a much cheaper form of credit. That is useful information for borrowers.

However, APRs don’t always make them look bad. Compare the APR of a $100 payday loan to the late fee on a credit card or utility bill for a similar amount. Suddenly, they don’t seem so expensive.

| DESCRIPTION | APR | FEE |

|---|---|---|

| Credit Card Late Fee | 965% | $37 |

| Power Bill Late Fee | 1,203% | $46 |

| Bounced Check | 2,336% | $32 |

| Payday Loan Fee | 391% | $15 |

A Note On Loan Calculators

In the following sections, we’ll explain how to figure out the APR and total interest paid on several different types of loans. Of course, you can always use an APR calculator online, which can have your apr calculated in a matter of seconds. However, there is also value in knowing how to complete the work yourself. This allows you to know for sure that the APR calculator is giving you the correct information and that you inputted your numbers correctly. In other words, the following explanations will help you check the work of an APR calculator.

How to Calculate the APR of a Term Loan

Calculating the APR of a loan is simple. You need three numbers: the amount borrowed, the total finance charge, and the term length of the loan.

To illustrate, let’s calculate the APR on a $1,000 loan with a $400 finance charge and a 90-day term.

- Divide the finance charge ($400) by the loan balance ($1,000)

- Multiply the result (0.4) by the number of days in the year (365)

- Divide the total (146) by the term of the loan in days (90)

- Multiply the result (1.622) by 100 and add a percentage sign

The result:

$400 / $1,000 x 365 /90 x 100 = 162.2%.

Easy. However, calculating the finance charge of a loan can get a little more complicated.

This calculator will give you an idea of what interest rate and monthly payment you can expect based on your credit score, loan amount, and term.

[the_ad id=”62695″] The method to calculate the finance charge varies depending on the type of loan. Let’s move on to the easiest to calculate: payday loans.

How to Find the APR of a Payday Loan

Although most lenders disclose the APRs of their loans, they often bury them in the small print. Payday lenders prefer to present the cost as a fixed fee for every $100 you borrow.

How do you find the APR using this information? Just add these two steps:

- Divide the total loan by 100

- Multiply the result by the fixed fee for every $100.

The result is the loan’s total finance charge. You can now calculate the APR using the method explained above.

As an example, let’s calculate the APR on a $1,000 payday loan with a 14-day term that charges $20 for every $100 you borrow.

- Divide the total loan ($1,000) by 100.

- Multiply the result (10) by the fixed fee ($20) for every $100. This is your finance charge.

- Divide the finance charge ($200) by the loan amount ($1,000)

- Multiply the result (0.2) by the number of days in the year (365)

- Divide the total (73) by the term of the loan (14)

- Multiply the result by 100 and add a percentage sign

The result:

$200 / $1,000 x 365 /14 x 100 = 521.42%.

How to Find the APR of a Line of Credit (LOC)

The problem with lines of credit is they are an open form of credit, so you don’t know how much it will cost until you repay it. With open lines of credit, you can borrow as much or as little as you want as long as you don’t exceed the credit available. You can then repay the minimum amount (more on that later) or the total amount after just a few days. All this could drastically change the APR of the line of credit (also known as LOC). Be sure to fully understand the terms and conditions of the line of credit before you decide to borrow money.

For the purposes of this exercise, we will assume the loan is for $1,000, and you only make minimum payments on a line of credit that charges:

- a one-time withdrawal fee of 10% of the amount,

- a monthly minimum principal payment of 5% of the outstanding loan amount with a minimum of $50,

- and an outstanding balance fee of $10 for every $100 unpaid.

To clarify, with this loan, you would get $900 ($100 is deducted for the withdrawal fee). Take this into consideration when deciding how much you need to withdraw from your line of credit. The first month you would pay $50 ($50=$1,000 x 0.05) for the minimum principal payment and $100 for the outstanding balance fee ($1,000/100 x $10). The fees would change the following months as the outstanding amount gets smaller. So how would you figure out the overall finance charge of a line of credit?

The first step is to plug in the dollar amount of each fee and how long it will take to repay it

- Multiply the loan amount by 0.1 and deduct it from the loan amount you receive. If you borrow $1,000 you will only get $900 ($1,000- x 0.1) in your account. Include the fee (in this case, $100) into the financing fee.

- Create a spreadsheet that calculates the 5% of outstanding balance every month with a minimum payment of $50 and adds a $10 fee for every $100 on loan. So $1,000 would give you $1,000/100 = $10. Multiply the result by $10. So your first month would have an outstanding balance fee of $10 x $10 = $100.

- Work out how the monthly payments will change as your principal drops. I created this table using a simple Excel spreadsheet.

| Balance | Withdrawal Fee | Principal | Outstanding Balance Fee | Monthly Fee |

|---|---|---|---|---|

| Month 1= $1,000 | $100 | $50 | $100 | $250.00 |

| Month 2= $950 | $50 | $95 | $145.00 | |

| Month 3= $900 | $50 | $90 | $140.00 | |

| Month 4= $850 | $50 | $85 | $135.00 | |

| Month 5= $800 | $50 | $80 | $130.00 | |

| Month 6= $750 | $50 | $75 | $125.00 | |

| Month 7= $700 | $50 | $70 | $120.00 | |

| Month 8= $650 | $50 | $65 | $115.00 | |

| Month 9= $600 | $50 | $60 | $110.00 | |

| Month 10= $550 | $50 | $55 | $105.00 | |

| Month 11= $500 | $50 | $50 | $100.00 | |

| Month 12= $450 | $50 | $45 | $95.00 | |

| Month 13= $400 | $50 | $40 | $90.00 | |

| Month 14= $350 | $50 | $35 | $85.00 | |

| Month 15= $300 | $50 | $30 | $80.00 | |

| Month 16= $250 | $50 | $25 | $75.00 | |

| Month 17= $200 | $50 | $20 | $70.00 | |

| Month 18= $150 | $50 | $15 | $65.00 | |

| Month 19= $100 | $50 | $10 | $60.00 | |

| Month 20= $50 | $50 | $5 | $55.00 | |

| Term = 600 days | Total Finance Charge: | $2,150.00 |

Now you know the finance charge ($2,150 in our example), you can follow our standard APR formula.

- Divide the finance charge ($2,150) by the total borrowed ($1,000)

- Multiply the result (2.15) by the number of days in the year (365)

- Divide the total (784.75) by the term of the loan (600=20 months x 30 days)

- Multiply the result (1.308) by 100 and add a percentage sign

The result:

The total APR of the line of credit in this example would be 130.8% ($2,150 / $1,000 x 365 /600 x 100 = 130.8%)

How to Find the APR of a Credit Card

As a credit card user, chances are you will have to take on some credit card debt at some point in your life. Credit card providers in the United States are required by law to disclose the interest rate of their credit cards to customers. The annual rate you’ll pay depends on the credit card you choose and your credit score. Those with high credit scores will receive offers with lower interest rates, while those with lower credit scores will receive offers for credit cards with a higher interest rate. When shopping for credit cards, be sure to note the interest rate of the card being offered and compare its APR vs. that of other cards.

Here are some helpful tips from SuperMoney on how to improve your credit score and get better loan offers, credit card offers, and lower interest rates.

How to calculate the APR of a mortgage

Just like with a credit card, mortgage lenders are required by law to provide an APR to borrowers, so you won’t need to figure it out for yourself. If your lender will not give you an APR, walk away and find other loan offers even if the products appear to be a good deal. That is not the kind of lender you want to trust with your mortgage.

The APR of a mortgage includes the loan amount, interest rate, discount points, and other costs of financing a home. You will need to include all these expenses when calculating your APR and finding out how much you’ll pay over the full loan term.

However, if you want to learn how to calculate the APR, here is a step-by-step guide on how to calculate the APR of a fixed-rate mortgage. For this example, let’s say you have a $330K mortgage with a 10-year-term, a monthly payment of $1,500, and that you paid $2,000 in points and $2,000 in origination fees.

Be aware that these steps are for mortgages with fixed rates. It is different for mortgages with variable APR rates. A variable APR means the rate can change depending on various factors and will stay the same for one year. Therefore it is much more difficult to predict total interest charges that will accrue over the life of the loan.

Mortgage APR formula

- If your mortgage has points (lump-sum payments that lower your interest rate), add their total cost (e.g., $2,000 for two points).

- Multiply your monthly payments (e.g., $1,500) by the number of months in your mortgage’s term (e.g., 360 months).

- Add the cost of the points, loan origination fees (e.g., $2,000), the monthly payments, and any other expenses related to financing the purchase of the property. This is the adjusted principal of your mortgage. In our example $334,000 ($330000 + $2,000 + $2,000).

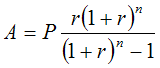

- Find what interest rate would amortize your adjusted balance for that number of monthly payments (e.g., 120 months). The formula below is used to calculate the amortization of a mortgage.

A stands for the monthly payments, P is the principal (in our example, the adjusted balance), r is the monthly interest rate (in our case, the APR divided by 12), and n is the number of months. Now you “just” need to solve this polynomial for “r” instead of “A.”

Amortization of a Mortgage Depends on the APR and Loan Amount

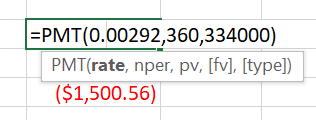

There are several ways to solve this equation. If you are a bit rusty with polynomial equations, you can just guess until you get close enough using Excel’s built-in formula: PMT. Enter this formula “=PMT(r/12,n,P)” in a cell and play around with the “r” variable until you get the right monthly payment.

Notice Excel uses the monthly interest rate, so you need to divide the APR by 12. For example, a 3% APR would be 0.03/12 or 0.0025. Using our example the cell would include “=r, 120, 244000” with “r” being the APR we are trying to find. I started with 4%. A little too high. I tried with 3.5%. Close but too low. After a couple of tries, I found that an APR of 3.54% gives you a monthly payment of $1.500.56. Close enough.

What’s Next?

Knowing how to calculate the APR of a loan is important, but it’s only the first step. There are other things to consider, such as loan origination fees, prepayment penalty fees, and late fees. It’s also important to see what other borrowers have to say about the customer service of a lender. SuperMoney’s loan comparison tools offer an easy and transparent way of comparing major lenders without having to waste time and money with multiple loan applications.

If you’re looking for a personal loan, an auto loan, a mortgage, a HELOC, credit card, balance transfer, personal line of credit, or any other type of credit or offer, check the rates and terms you qualify for multiple lenders before you commit.

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

Share this post:

AddTable of Contents