CAN Capital: a Pioneer in Small Business Loans

Last updated 04/30/2024 by

Andrew Latham

Small business owners are expected to fail. An accepted rule of thumb is that 8 out of 10 startups fail within the first 18 months, which may explain why small business loans are so hard to find, and why 38 percent of all startups rely on loans from family and friends. It is a catch 22 situation. A lack of access to loans with reasonable rates does not exactly help small businesses’ success rate either. CAN Capital is a leader in alternative small business finance that is, along with other small business lenders, trying to change that.

How Does CAN Capital Compare To Traditional Lenders?

CAN Capital cannot compete with traditional lenders when it comes to interest rates, but it makes up for it with speed, flexibility, and customer service. The interest rate difference with prime traditional lenders is a moot point. In any case, most of CAN Capital’s borrowers would not qualify for a business loan with a traditional lender.

Eligibility

Large traditional banks only approve one in five business loan requests, according to a report by the Birmingham Business Journal. Successful borrowers are usually required to have a credit score of 680 or higher.

CAN Capital does not require borrowers to have a stellar credit history. Even applicants with poor credit scores have a chance. Around 70% of people that complete an application are approved, according to CAN Capital CEO, Dan DeMeo. This is because CAN Capital uses proprietary underwriting algorithms that consider a wide variety of data points when assessing eligibility. For instance, CAN Capital looks at a business’ frequency of sales, not just total sales. It also takes into account unorthodox risk indicators, such as a company’s customer rating.

Loan Application Process

If you have ever applied for a loan with a traditional bank, you know how easy it can be to waste hours collecting the necessary documents. Just waiting for a loan officer to pull your credit can take 10 business days. Most major banks just don’t seem to understand how important cash flow is for small businesses and don’t have the technology in place to process loans faster.

The entire loan application takes 10 minutes or less with CAN Captial. Once approved, companies can receive their money in as little as two days.

Repayment

Traditional business lenders require borrowers to make regular and fixed monthly payments, usually every month. These amounts do not change, regardless of how well or how badly a business does. CAN Capital also offers a similar option for those borrowers who prefer a fixed payment amount. Their small business loans offer a maturity date and fixed daily payment amounts that the borrower can rely upon.

CAN Capital borrowers may alternatively opt for a merchant cash advance which gives them flexible daily payments that vary depending on the sales. On days when sales are soaring, payments are higher. On slow days when sales are not as great, the payments are then lower.

What Are CAN Capital’s Interest Rates, Fees, And Terms?

CAN Capital provides customers with two products: installment loans and merchant cash advances. Rates vary with time and depending on the credit product you choose, your credit score, business type, and annual revenue. These interest rates and examples are valid as of March 2016. Visit CAN Capital’s profile for the latest rates and terms.

Installment loans have:

– Interest rates that start as low as 12.9% (does not include the 2.99% origination fee).

– Loan amounts range from $50,000 to $150,000.

– Borrowers can choose repayment terms of 2 to 4 years.

CAN Capital’s installment loans are only for select companies whose owners have good personal credit, have been in business for a minimum of 7 years, and have at least $350,000 in annual sales.

Merchant Cash Advances have:

– APR varies depending on the loan amount and term (approx. 60% to 70% APR).

– Loan amounts range from $5,000 to $150,000 depending on your monthly gross sales.

– Borrowers can choose repayment terms of 4 to 12 months.

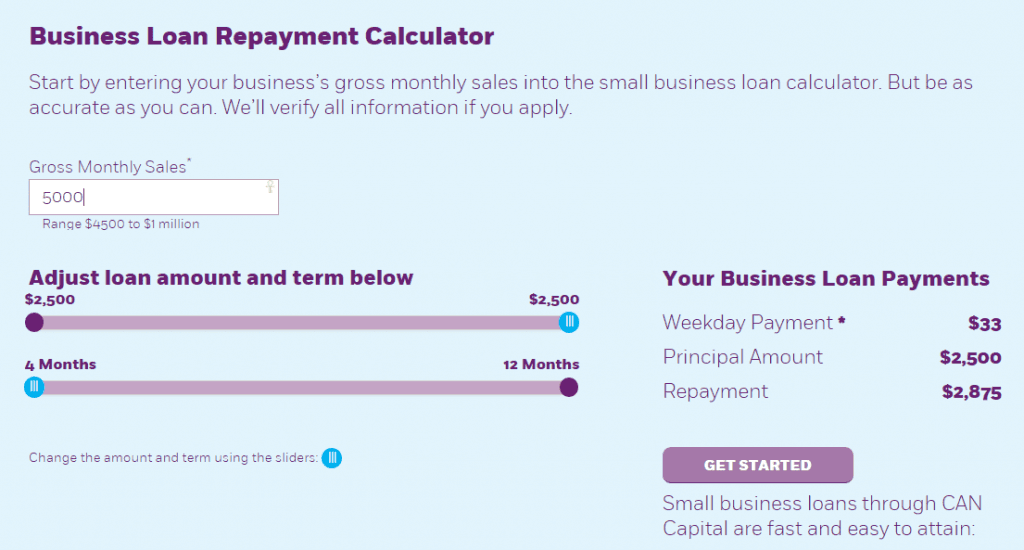

CAN Capital does not publish its interest rates or even the average rate of their loans. However, it does provide a business loan repayment calculator that allows you to estimate your APR.

Interest rates vary depending on the length of the loan’s term. For example, a $150,000 loan with a 12-month term will have daily payments of $768: a total of $52,500 in interest payments, which is the equivalent of a 59.4% APR. The same loan with a 4-month term would have an APR of 70.0%.

How Does CAN Capital Work?

CAN Capital’s loans are issued by WebBank, a Utah-based industrial bank and through CAN Capital’s subsidiaries: CAN Capital Merchant Services and CAN Capital Asset Servicing.

CAN Capital’s Merchant Cash Advances

Merchant cash advances are technically not a loan, but are rather a purchase of a business’ future sales at a discounted rate. Instead of paying a fixed monthly amount, companies send a percentage of their daily revenue until the debt is repaid. Merchant cash advances have relatively high interest rates, but they typically don’t have origination fees.

The advantages are:

- Funding is fast

- Smaller loan amounts are available

- Easy approval process

- An option for borrowers with bad credit

- No monthly payments – payments vary depending on daily sales

The disadvantages are:

- Higher fees than installment loans (up to 70% APR)

- Daily payments can restrict cash flow

CAN Capital’s Installment Loans

Installment loans are the most common form of a business loan. Companies borrow a fixed amount and repay it over a fixed term for an agreed interest rate, which is usually fixed for the duration of the loan.

The advantages are:

- Larger loan amounts

- Lower interest rates

- Longer terms

- Fast funding

The disadvantages are:

- Fixed monthly payments

- Strict credit criteria

- Smaller loan amounts are not always available

What Is CAN Capital’s Application Process Like?

CAN Capital’s application process varies depending on the credit product you choose. This review will focus on CAN Capital’s installment loan application process.

To qualify for a CAN Capital installment loan, a business must:

- Have at least 7 years in business. Merchant cash advances are an option for newer businesses.

- Have at least $350,000 in annual sales.

- The business owner (or owners) must have good personal credit.

If you meet those qualifications, complete CAN Capital’s one-page application form.

1. Submit the business owner’s full name, business phone, business name, and email.

That’s it. CAN Capital’s business consultants will call you and walk you through the application process.

The backstory of CAN Capital

CAN Capital is a veteran in alternative small business finance. It was founded in 1998 and is based in New York City. The company has provided access to working capital to over 139,000 companies. Since 2011, CAN Capital has secured $740 million in funding. In the latest series of financing (April 2015), twelve banks (including Wells Fargo, Morgan Stanley, Barclays, J.P. Morgan and UBS) provided CAN Capital with $650 million toward debt financing.

CAN Capital brought an important innovation to small business finance: daily remittance. Daily remittance is the ability, which not all lenders have, of accepting payments daily instead of larger payments once a month. CAN Capital has also been a pioneer in using sophisticated risk assessment models that include data points that traditional lenders ignore.

How Does CAN Capital Compare To Other Lenders?

The struggle to find a small business loan with reasonable terms and rates is particularly brutal for small companies that lack the collateral, credit history, and revenue to meet the credit criteria of traditional lenders. Even successful small businesses with profitable business models often don’t qualify. Those that do, must face a painfully slow application process.

CAN Capital is a market leader in alternative small business financing. The rates for its loans, particularly its prime installment loans, are competitive. Its merchant cash advances do have high interest rates, but they have flexible payment schedules and provide access to credit for business owners with less than stellar credit. CAN Capital has similar rates and terms to Kabbage, another online lender that is changing the way small businesses access financing.

CAN Capital is not a lender for business owners with excellent credit or for established businesses with plenty of collateral. Those businesses can find business loans with prime lenders, such as LendingClub or Prosper. However, if you value flexibility and speed and your business doesn’t meet the credit requirements of prime borrowers, you should consider CAN Capital.

CAN Capital’s Key Benefits Include:

- Flexible payment schedule

- Simple application process

- Accessible credit criteria

- Fast funding

- Selection of credit products

- Over 18 years experience in small business finance

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

Share this post:

AddTable of Contents