How To Pay Off Credit Card Debt: Ultimate Guide

AL

Last updated 03/19/2024 by

Andrew LathamFact checked by

Credit card debt interest payments can get expensive fast. If you’re not careful, credit cards can claim a significant portion of your monthly income and create a boatload of stress.

While it’s possible to use credit cards and stay out of debt, this isn’t the reality for many Americans. When credit card debt becomes unmanageable, it affects your credit score and your peace of mind. In fact, studies have shown that worries over mounting debt can cause depression and other serious health issues. By utilizing some of the best strategies outlined below, you can beat any outstanding credit card debt.

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

What is credit card debt?

Credit card debt is a type of debt accrued by failing to pay off your credit card. Most consumer credit cards have a grace period wherein there is no interest charged on the debt if the balance is paid in full. This is an incentive that credit card issuers use to get consumers to sign up. However, if you don’t pay off your balance in full, it will begin to bear interest. High interest rates on credit card accounts make this one of the worst types of debt to incur.

Users are often enticed to sign up for credit accounts with promises of high balances or rewards and then encouraged to make only small minimum monthly payments. Over time, your credit card account can build a growing balance of debt, and the interest owed will skyrocket. This is the downside that the credit card issuer doesn’t explain. Paying down the debt can be difficult due to climbing balances, compounding interest, and growing monthly payments.

Credit card debt and your credit score

The balance you carry on your credit cards doesn’t only affect your spending ability. Your credit card balance plays an important role in determining your credit score. In fact, your credit utilization ratio, which is your outstanding credit card debt divided by your credit limit, is responsible for 30 percent of your credit score. Keeping your credit limits in mind is one of the most important things you can do when you sign up for credit cards since keeping your credit card balances low can keep your credit score high.

How prevalent is credit card debt in the United States?

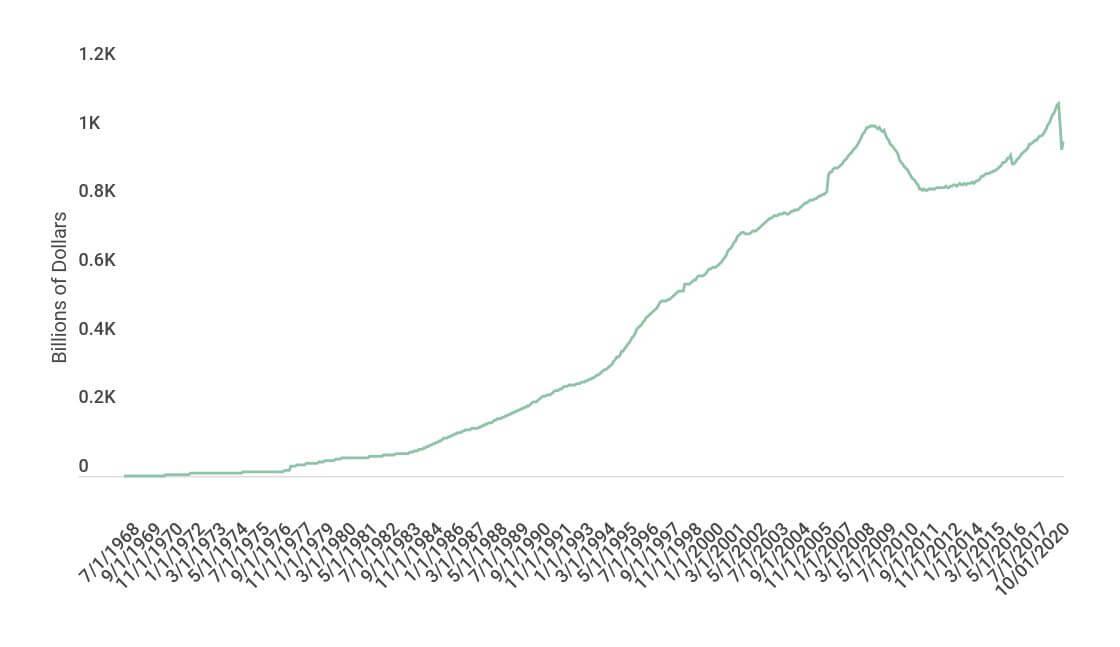

If you think that you’re the only person who is drowning in credit card debt, think again. According to figures from the U.S. Census Bureau and the U.S. Federal Reserve, the total outstanding revolving debt in the United States was $1.045 trillion in January 2019. That’s even higher than the credit debt carried during the 2008 Recession.

An alarming Pew study found that 54 percent of Americans spend more than they earn every month. It’s no surprise that 48 percent of credit card users make only the minimum payment on their credit cards every month. The result? The average American household has a whopping $6,354 in credit card debt (source).

In the past decade alone, the average American amount of credit card debt has increased by over 50 percent. As people in this country become more heavily indebted, many reach a breaking point and seek answers on how to pay off credit card debt.

How soon should you pay off your credit card debt?

Unless you’re sitting on other debt with higher interest rates, paying off credit card debt should be your top priority.

If you carry a high revolving balance of consumer debt, you’re spending an incredible amount of your disposable income each month on interest charges alone. This is far beyond the value of the goods and services that you originally used the credit cards to purchase. If you aren’t paying your bills on time, you’ll also incur late charges.

Credit card debt also hurts your credit score. Your credit utilization — how much of your credit limit you’re using at a given time — accounts for 30 percent of your credit score. The more debt you accumulate, the more you’ll hurt your credit. If your credit score drops enough, it will affect the interest rates that you qualify for. That means the debt you’ve accumulated will hurt your pocketbook even more.

How can you get out of credit card debt fast?

Need to pay off your credit card debt and fast? Here’s how to get started.

First, decide how soon you’d like to have your debt fully paid off and figure out how much you’d have to pay each month to reach that goal. Minimum monthly payments will never get you to this milestone. Online calculators can help determine the payment on your balance and current interest rate over the course of twelve months.

Strategies for eliminating credit card debt

If you want to know how to pay off credit card debt in the most efficient manner, you have options. The method(s) that will work best for you will depend on your circumstances and individual preferences.

Use the snowball method

Make a list of all of your credit card accounts, their balances, and their interest rates. If you can transfer balances from cards with higher rates to those with lower rates, do this. Then, make minimum monthly payments on all of your cards except for the one with the highest interest rate. On that card, pay as much as you can afford every month until the card is paid off. Once this is done, repeat the process with the cards that you have left.

Why is this called the snowball method? When you tackle your debt with the highest interest rates first, the amount of money that you have to pay off debt will continue to increase — or snowball.

Transfer your balance

If your current interest rates are high, you should consider a balance transfer credit card that offers a zero percent interest introductory period. If you’re able to pay off the debt in full within that grace period, you can eliminate your credit card balances altogether. However, you’ll have to pay a balance transfer fee (3-5 percent of the total incoming balance) to transfer your debt. Make sure that the fee will cost you less than what you would have paid in interest. Just make sure to look for an advertiser disclosure before transferring your balance.

Dig into your savings

If you have a good amount saved in your bank account, this might be a good time to tap into some of that money. The average return on investment in the stock market is 7 percent, and your credit card interest rate is likely closer to 18 percent (or even higher). As such, the fastest way you can reduce losses is to allocate all available money, excluding your emergency fund, for your debt.

Consolidate your debt

An installment loan with a low APR can be a great way to consolidate high-interest credit card debt. Simply borrow enough to pay off all your credit accounts in one fell swoop, and trade your debts for a single easy monthly payment. These debt consolidation loans are a very popular way to reduce interest expenses and establish a structured plan to get out of debt. Also, different debt consolidation loans come with different rates, fees, and requirements, so check out the best personal loans to ensure that you choose the best option for you.

Utilize a home equity line of credit (HELOC)

If you’re a homeowner with equity in your home, you can leverage it to secure a loan or line of credit with very favorable rates and terms from different lender partners. These are called Home Equity Loans (HELs) or Home Equity Lines of Credit (HELOCs). However, you should only go this route if you’re certain that you’ll be able to pay off your HEL or HELOC on time. If you default on your payments, you risk losing your home.

Also, read the fine print and investigate the loan’s closing costs. If the closing costs will cost you more than the interest on your credit account, steer clear of this method.

Should you declare bankruptcy?

When you’re deeply in debt and struggling to pay your monthly bills, you may be tempted to declare bankruptcy. It can get the creditors off of your back, provide some breathing room, and give you a fresh financial start. However, bankruptcy also brings some serious downsides.

First, filing for bankruptcy costs money. The filing fees cost hundreds of dollars, and this is before you factor in attorney’s fees. While Chapter 7 bankruptcy will erase most credit card debt, it’s not as simple to qualify for Chapter 7 as it was in the past.

Just over ten years ago, Congress overhauled the bankruptcy law, and there is now a means test required for Chapter 7 filers. If you have enough disposable income to pay the debt on a Chapter 13 plan, you won’t be permitted to file for Chapter 7. Instead, you’ll have to enter a debt repayment plan through Chapter 13. A Chapter 13 bankruptcy comes with a 3 -5 year repayment plan for debt, which is then discharged after the plan.

Keep in mind that either type of bankruptcy will hurt your credit report for a full decade. This could affect your ability to get a loan, insurance, apartment, or even a job.

How can you negotiate credit card debt with banks?

In some cases, you can negotiate directly with your credit card company to set up a different payment plan or to settle your debt. This process can be complicated, but with patience and fortitude, you can get through it.

Your first step is to understand your debt and your budget. Ask each bank for a breakdown of your bill that shows the principal, interest, and other charges. Once you have it, create a monthly budget that illustrates your income and expenses. Don’t forget to include things like food, gas, and contingencies in your budget. This will let you know how much you can afford to pay each month. And being able to prove this figure gives you leverage in your negotiation.

Next, take some time to get to know your options. Several different arrangements may be available to you, depending on the particular bank and your circumstances. Here’s a quick rundown of your options:

Lump-sum settlement

Let’s assume that you have access to a sum of money from a family member or other source. You may be able to contact the bank and negotiate a reduced lump sum settlement of your credit balance to close out the entire account. This could also be accomplished in up to three payments.

If you reach a settlement agreement, get it in writing. You should also understand that debt settlements will affect both your credit score and your tax liability. All tax law considers most forgiven debt as income, so the amount forgiven will need to be reported on a 1099-C form.

Why will this work? If you’re late on your payments, a credit company may worry that you’ll default on your debt altogether. Accepting a lower settlement is a way for them to recover as much of the money you owe them as they can get.

Forbearance program

If your financial difficulties are due to temporary circumstances, consider a forbearance program. Under a forbearance program, the bank will temporarily lower or eliminate your interest rate and will put a stop to late fee charges. The bank may also allow you to stop making payments for a certain period of time. There is no forgiveness of any debt with this program, only a short reprieve.

Debt management or settlement program

While they sound similar, there’s a subtle difference between debt management and debt settlement programs. With a debt management program, you’ll meet with a counselor to restructure your debt to pay the entire amount owed until the program is complete. On the other hand, a debt settlement program will work on your behalf to negotiate lower payments or a lower settlement of your debt.

Negotiating

Now that you know what you can afford to pay and have an idea of which settlement or payment plans appeal to you, you’re ready to negotiate. Don’t expect this process to be quick or easy. You’ll likely tell the same story to a long line of people until you get to someone who has the power to help.

If you are having difficulty reaching the right person, ask for the credit manager and be sure to write down their name and telephone number before you hang up. Keep detailed notes of your conversations, and always be sure to get any agreements in writing.

If the bank is playing hardball and you’re unable to make a deal for better terms or a settlement, you might need help. Consider working with a debt settlement company. These experts are trained to help reduce and eliminate your credit card debt.

Should you use a debt settlement company to pay off your credit cards?

If you fail to pay your debts for long enough, creditors can make your life very difficult. If you have bad credit, it will be practically impossible to consolidate or refinance your debts. Debt collectors will be knocking at your door. They can even take you to court for it. As such, it is in your best interests to make a deal to reduce your settle your credit card debt as soon as you’re able.

This is what a settlement company can accomplish on your behalf. These companies will do the tough work of haggling and negotiating reduced payments to your credit card companies. Whether you’re currently paying on the account or have been sent to collections, a debt settlement company will usually be able to help you to secure terms.

Debt settlement companies can end up saving you a lot of money in the long run, sometimes as much as 50 percent or more. Interested in investigating a settlement company? Compare your options side by side, along with real user reviews, in this comprehensive list of the best debt settlement companies on the market.

AL

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

Share this post: