6 Credit Trends from 2024: Why They Matter and What They Teach Us for a Smarter 2025

Last updated 12/31/2024 by

SuperMoney Team

Edited by

Andrew Latham

Summary:

Credit products are essential financial tools, but what Americans choose and how they use them vary widely based on income and necessity. From credit cards to mortgages and alternative financing like buy now, pay later (BNPL), this article explores the most popular credit products, their usage trends, and what consumers need to know to maximize their benefits while avoiding pitfalls.

Credit products form a cornerstone of the U.S. financial ecosystem, enabling consumers to manage spending, fund major purchases, and navigate emergencies. But not all credit products are created equal, and access often reflects deeper economic trends. Here’s a look at five key insights about what Americans use and how they can make smarter financial decisions.

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

1. Credit cards dominate the market

68% of Americans have at least one active credit card and 52% are interested in a new credit account, according to a 2024 study by PYMNTS, making it the most common credit product.

Why it matters: Credit cards offer unparalleled convenience and rewards but can lead to financial strain if not managed properly.

What to do:

- Use credit cards strategically for rewards or building credit, but limit spending to avoid debt traps.

- SuperMoney’s app helps you create a budget, provides personalized insights, and helps you compare credit options.

2. The number of credit card accounts is increasing, but so is the percentage of credit card debt that is delinquent

The number of new credit card accounts increased by nearly 11 million from 2023Q3 to 2024Q3. This trend is nothing new. Credit card usage has been growing since 2010, with a brief pause during COVID-19.

However, the percentage of credit card debt that is 90+ days delinquent is also climbing — right into 2008 territory.

Why It Matters: While a growing number of credit card accounts can indicate consumer confidence and spending power, the simultaneous rise in 90+ day delinquencies suggests many people are struggling to keep up with their payments. This trend can quickly snowball into a larger financial crisis for individuals dealing with mounting debt—and potentially impact the broader economy if delinquencies continue climbing.

What to Do:

- Set a realistic budget: Prioritize essential expenses and allocate funds for paying down card balances monthly to minimize high-interest debt. SuperMoney uses AI-powered budgeting to help you do this just by synching your accounts.

- Utilize financial tools: Consider budgeting apps or credit counseling services for personalized guidance on managing debt.

- Explore consolidation options: If you have multiple balances, consider personal loans or balance transfer cards with lower interest rates to simplify repayment. Try SuperMoney’s Refi Robot.

- Pay on time, every time: Consistently making on-time payments can help avoid delinquency and build a stronger credit score over the long term.

3. High-income consumers hold more credit products

High-income consumers (earning $100,000+) hold nearly twice as many active credit products as those earning under $50,000 a year.

Why it matters: This disparity highlights financial inequities and the advantage high-income households have in accessing diverse and lower-cost credit products, like mortgages and auto loans.

What to do:

- Lower-income consumers should explore credit-builder products to improve their creditworthiness and access better rates.

- Consider using money management apps or credit counseling services for tailored financial advice.

4. Higher-income consumers are more likely to have a mortgage

High-income consumers are 3.3x more likely to have an active mortgage than low-income consumers.

Why it matters: Mortgages are a key path to homeownership, equity building, and long-term financial security. However, access remains a challenge for lower-income households.

What to do:

- For aspiring homeowners, focus on improving credit scores and saving for a down payment to access better mortgage terms.

- Research first-time homebuyer programs that offer reduced down payments and favorable rates.

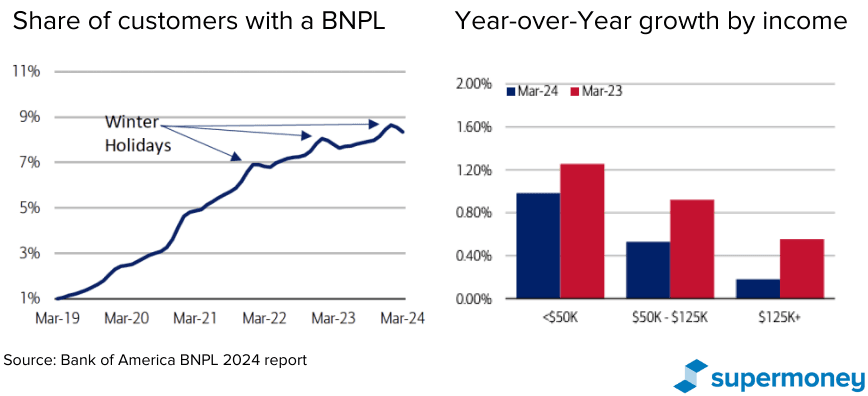

5. Buy now, pay later is popular but its growth is slowing down

14.4% of Americans use buy now, pay later (BNPL) services, which makes it one of the most popular credit products around.

However, BNPL adoption is slowing. Bank of America’s internal data shows a year-over-year growth in BNPL usage of just 0.5 percentage points as of March 2024, compared to 1 percentage point in 2023 and 2.5 percentage points in 2021. This deceleration signals a shift as consumers become more cautious about their spending habits.

Why it matters: While BNPL remains a lifeline for many, particularly Millennials and households earning under $50,000 annually, its heavy usage correlates with financial vulnerabilities. These include higher-than-average credit card balances and lower savings deposits, creating risks for those relying on it excessively. The trend suggests consumers are starting to reassess its practicality.

What to do:

- Assess your BNPL usage to ensure it aligns with your financial goals, prioritizing essential or planned purchases.

- Monitor your overall debt levels and avoid relying on BNPL as a primary financing method.

- Explore other financing options, like credit cards with 0% APR promotional periods, to balance flexibility and cost.

The slowing growth of BNPL usage could indicate a shift toward more responsible spending habits or concerns about debt accumulation. By using BNPL wisely and understanding its limits, consumers can avoid the financial pitfalls associated with this payment method.

6. Store cards vs. personal loans: The cost of easy credit

14.9% of Americans have personal loans, while 24.6% use store cards.

Why it matters: Store cards may promise perks but carry hefty interest rates; personal loans can be a cost-effective alternative for consolidating debt or funding large purchases. Personal loans typically have lower interest rates (the average is around 12% APR) and can consolidate debt or fund large expenses. Store cards offer perks but the average APR is above 33% (compared to 24% for regular credit cards).

What to do:

- Compare personal loan offers to find the best interest rates and repayment terms for debt consolidation.

- Use store cards sparingly, prioritizing cards with broader utility and better rates.

Key takeaways

- Credit cards remain the most popular financial tool but require careful management to avoid debt.

- High-income consumers enjoy better access to diverse credit products, emphasizing the need for financial equity.

- Mortgages are essential for wealth-building, but affordability and access are significant challenges for low-income groups.

- Alternative financing like BNPL is growing rapidly but can lead to financial strain if misused.

- Niche products like personal loans and store cards serve specific needs but require careful consideration to maximize benefits.

Share this post:

Table of Contents