Contribution Margin Ratio: What Is It, and How Do You Calculate It?

Summary:

The contribution margin ratio (or contribution margin) is an effective measure of a company’s profitability and a tool for comparing multiple companies. It shows the marginal benefit of producing or selling one more unit. With the contribution margin, an investor or analyst could determine how efficiently a company makes its products and how well that efficiency translates to the bottom line. They could then compare the contribution margin to different companies to help influence investment or management decisions.

Suppose you want to help identify how a company generates its profits or compare two businesses in the same industry. You may have difficulty using measures like gross revenue or net income if they are vastly different sizes. The larger company will likely have higher revenues and net incomes, but the smaller company may run much more efficiently.

There are several ways you can get around this problem, including common-size financial statements and metrics like gross and net margin. Another measure you can use is the contribution margin ratio, or contribution margin. It is a relatively simple metric that helps show how efficiently a company produces its products and can give, in percentage terms, the remaining revenue to cover fixed costs.

Compare Business Loans

Compare rates, terms, and community reviews between multiple lenders.

What is “contribution?”

Contribution is the amount of sales revenue left to cover a company’s fixed costs. It is calculated by subtracting variable costs from gross revenue. Variable expenses include the cost of goods sold (COGS), marketing expenses, shipping and delivery fees, credit card expenses, sales commissions, and any cost that can rise or fall with the level of sales.

“Contribution” shows the amount of revenue left to cover fixed expenses in a business, like building rent. The greater the contribution, the easier it is for the business to cover its fixed costs.

For example, if XYZ Company has $10,000,000 in annual gross revenue and $4,000,000 in annual variable costs. Its annual contribution is $6,000,000. Thus, XYZ Company has $6,000,000 to cover its annual fixed expenses. It is possible to have a negative contribution margin if the variable costs are higher than the revenue.

If you need additional funds to cover your business’s fixed expenses, you may want to consider applying for one of the business loans below.

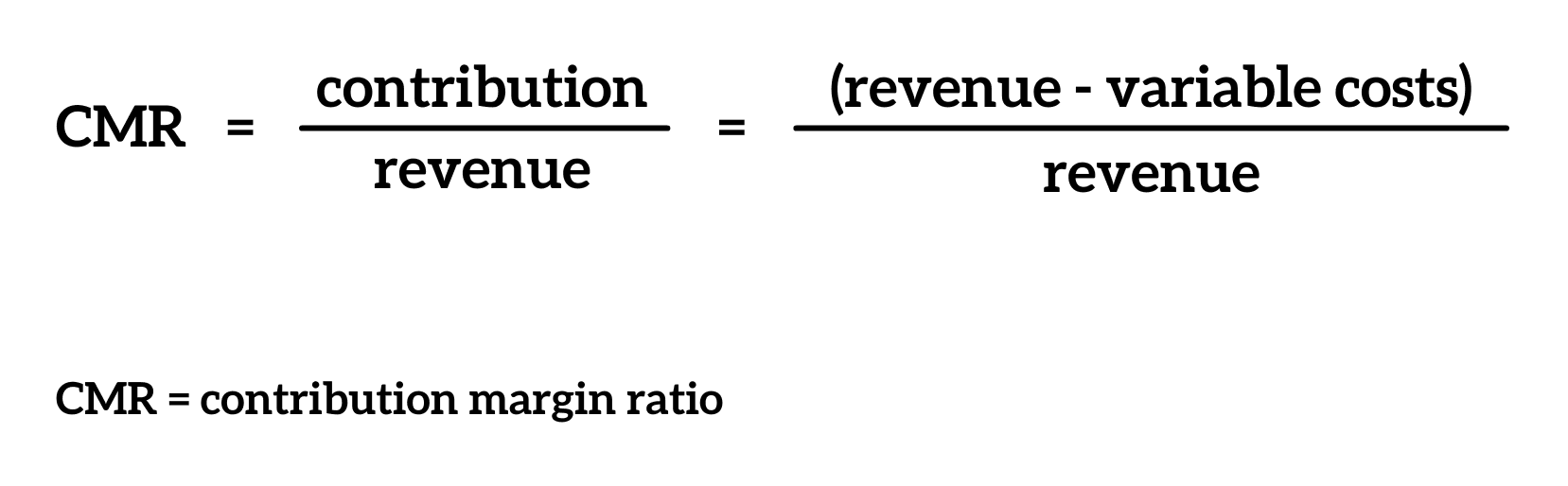

What is the contribution margin ratio?

Let’s say we wanted to compare company XYZ Company’s contribution to ABC Company, which has a contribution of $60,000,000 and gross revenues of $600,000,000. It may seem reasonable to assume that since ABC has a higher contribution, it is a financially healthier company.

However, ABC’s revenue is 60 times higher than XYZ’s. To help compare the two differently sized companies, we need to use the contribution margin ratio. To calculate it, we take the contribution and divide it by the revenue, as seen in the contribution margin ratio formula below:

Applying this formula to XYZ and ABC, we find that XYZ has a contribution margin ratio of 0.60 or 60%, and ABC has one of 0.10 or 10%. From here, we can compare how efficiently each company produces its goods and services. XYZ has 60% of its gross revenues to cover fixed costs, while ABC only has 10% of its gross revenue left for fixed costs.

You can also calculate the contribution margin ratio on a per-unit basis. If XYZ sells an item for $100 with a variable cost of $40, then the contribution would be $60, and the contribution margin would be 60%.

Uses in business

Contribution margin analysis is used in business to help identify how easily and efficiently a business uses its revenue to cover fixed costs. It can also be a great comparison between different-sized companies. The examples above with XYZ and ABC Company show how that comparison can play out.

However, it’s essential to exercise caution in using the contribution ratio to compare companies. After all, different companies have different business models, whether they’re within the same industry or exist in different industries.

For example, ABC Company could produce a product with high variable production costs (like raw materials) but limited fixed costs, while XYZ may have low variable costs but high fixed costs. So, by only using the contribution margin, your comparison may make a false conclusion about which company is producing its goods and services more efficiently.

When used with other metrics like gross margin and net margin, the contribution margin ratio can help identify where a company is more efficient at generating profit. So it can take a picture of a profitable company, break down why it is profitable, and shine a light on the management decisions to lead the company to profit.

Break-even analysis

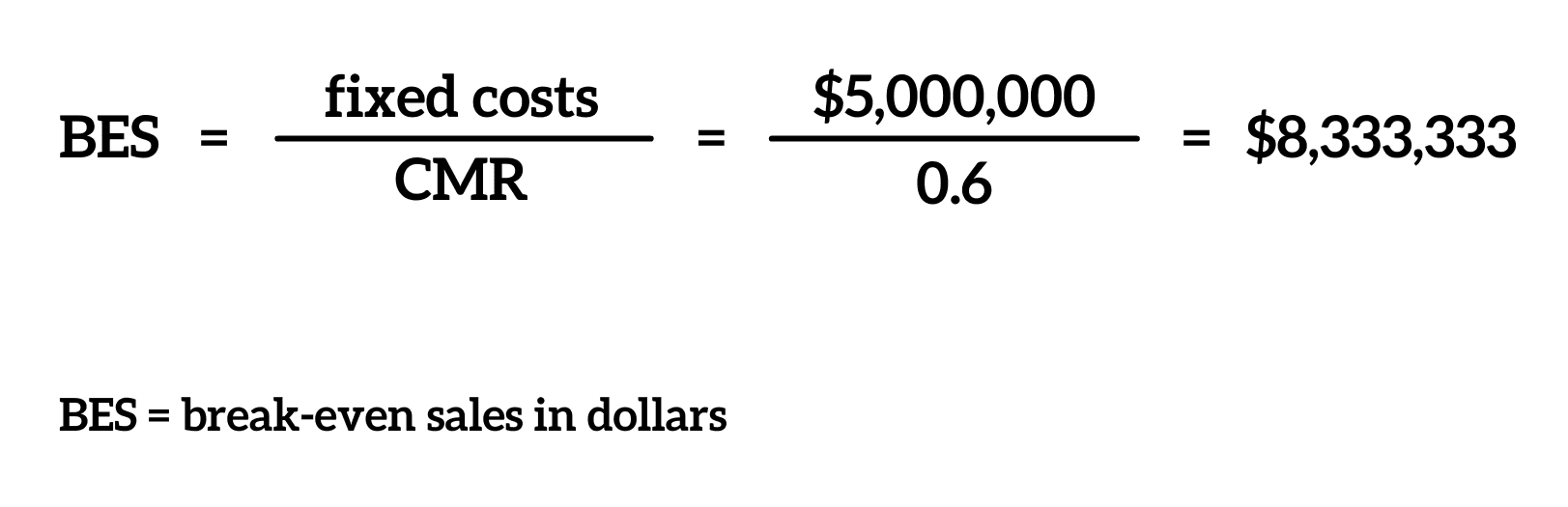

Another good use of the contribution margin ratio is in break-even analysis. Say you knew XYZ Company had a contribution margin ratio of 60% and fixed costs of $5,000,000. To find the dollar amount of sales needed to break even, you would divide the fixed costs by the contribution margin ratio:

To convert that to a unit break-even quantity, divide the $8,333,333 by the unit’s selling price. So if XYZ sold each unit for $100, they would need to sell roughly 83,000 units to break even.

What is a good contribution margin ratio?

As with most margin ratios (gross, net, and contribution margin), a high contribution margin is preferred over a low contribution margin. The best contribution margin is 100%, which indicates there are no variable costs in the business, so you want to be as close to 100% as possible.

However, different industries and companies in the same industry will have different contribution margin ratios that they define as “good.” Instead of trying to achieve a specific target, increase the ratio as much as possible without sacrificing quality and employee morale.

Pro Tip

You’ll likely see low contribution margins in labor-intensive businesses, where a product or service may require more manpower or personal attention. High contribution margins, on the other hand, are common in large corporations that mass-produce products using expensive machinery.

Why is contribution margin ratio important?

A company’s contribution margin indicates how much money per sale or unit goes toward the company’s overall profit. Using this knowledge, a business can understand how much money they need to make in order to break even, or whether the price of a product must increase or decrease based on fixed and variable costs.

Contribution margin can also identify when a company is spending too much on variable costs. If your business has a low contribution margin ratio, then your variable costs are likely too high compared to the profit made per unit sold. In that case, you can either raise the price of the product or cut variable costs.

FAQs

What does the PV ratio indicate?

PV ratio stands for the profit-volume ratio, which is another name for the contribution ratio. A high PV ratio would indicate a higher profit margin, while a low PV ratio would indicate a lower profit margin.

What is contribution margin vs. gross margin?

While both the gross and contribution margins examine a company’s efficiency, they differ slightly in how they’re calculated. Gross margin is calculated by subtracting the cost of goods sold (COGS) from your total revenue to get your gross profit. You would then divide gross profit by gross revenue to get the gross margin.

Contribution margin differs slightly from gross margin as it includes all variable costs. Instead of focusing on just COGS, contribution margin looks at other variable overhead costs as well as marketing and commission costs, which may not be included in COGS. The gross and contribution margin differences can be significant depending on the company.

Key Takeaways

- The contribution margin ratio is a measure of profitability that gives the marginal benefit of making or selling one additional unit.

- To calculate the contribution margin ratio, divide the company’s contribution (sales revenue minus variable expenses) by the gross revenue.

- The higher the contribution margin, the better.

- This ratio can be used to compare the efficiencies of multiple companies, which could influence investment or management decisions.

Chip Stapleton is a Series 7 and Series 66 license holder, CFA Level II candidate, and holds a Life, Accident, and Health Insurance License in Indiana. Chip received his Bachelor's in Saxophone and Physics from the Indiana University Jacobs School of Music in 2008. During his time there, he honed his mathematical and analytical skills. He received his Master's in Music Technology from Indiana University Purdue University—Indianapolis in 2010, where he was a Graduate Assistant. He is a financial advisor who enjoys the opportunity to train, develop, and support new advisors to build their own practices and help their clients achieve their goals. This included helping with case design, product knowledge, investment analysis, investment recommendation, portfolio construction, asset management, financial statement analysis, business planning, and business exit strategies.

Table of Contents