What is Purchase APR?

Summary:

Credit card companies use your credit card’s purchase APR to calculate the interest added to your remaining balance. You may have a fixed APR, which stays the same from month to month, or a variable APR, which may vary between months, depending on your card’s terms.

If you’re like most people, you probably have a love-hate relationship with your credit card. On one hand, it’s great to have a source of emergency funds when you need it. But on the other hand, those pesky interest charges can add up quickly if you’re not careful. So what exactly is an annual percentage rate (APR), how does it factor into your interest rates, and what can you do to keep your costs down?

If you carry a balance on your credit card from month to month, you’ll be charged interest on that balance at the APR specified in your cardholder agreement. These interest charges can add up quickly, so it’s important to understand how APR works and how it can impact your bottom line.

Understanding purchase APR

Purchase APR stands for purchase annual percentage rate, which is used to calculate how much interest you’ll pay each month on your credit card. This number is usually determined by your credit card issuer based on your credit score when you apply. Typically, the better your credit, the lower the APR you’ll receive.

According to Federal Reserve data, the average purchase APR on credit cards was around 16% in the first quarter of 2022. If you’re unsure what your purchase APR is, you can check out the fine print on your monthly credit card statement or ask your credit card company directly over the phone.

Keep in mind that if you pay back your entire credit card balance in full each month (not just the minimum payment), you won’t have to worry about your APR. However, if you decide to carry over a remaining balance from one month to the next, then your APR can directly affect how much interest charges you’ll incur.

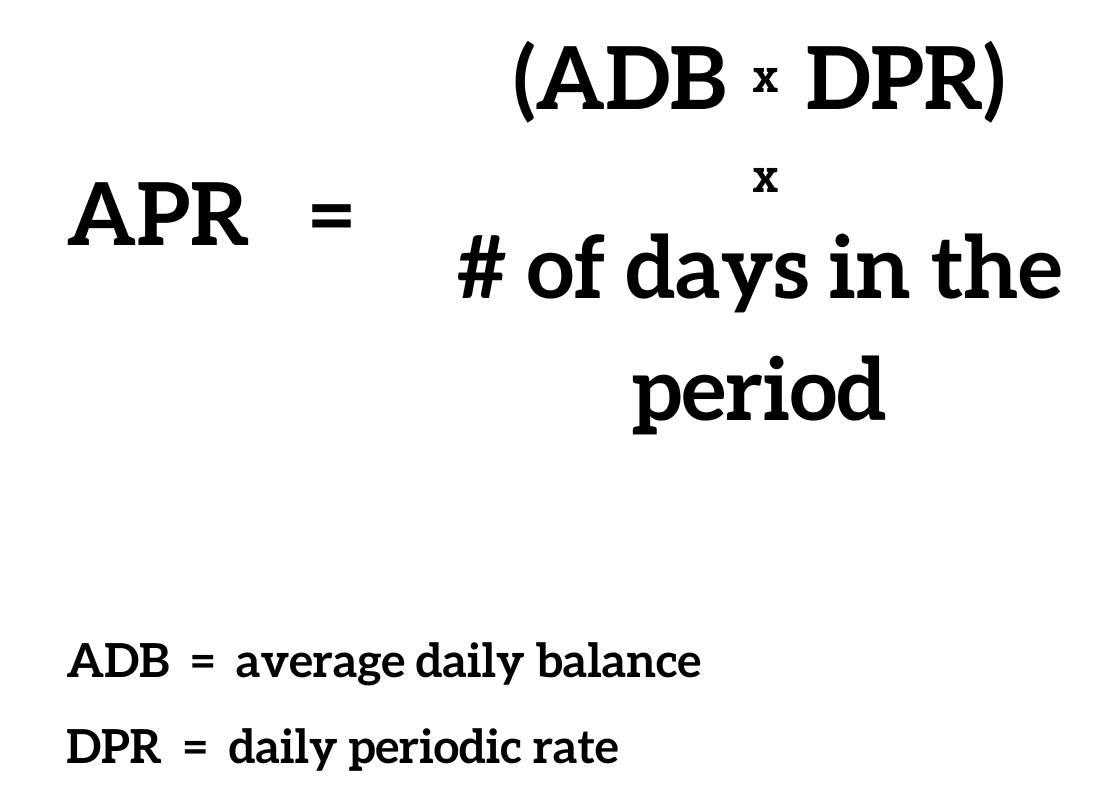

So how is your interest payment calculated? Here’s the formula:

Formula explained

- Average daily balance. Calculated by adding up each day’s balance for the billing cycle, then dividing the total by the number of days in the period.

- Daily periodic rate. Purchase APR divided by the number of days in the year (365).

- The number of days in the period. Depending on the credit card issuer, the number of days in a billing cycle can be anywhere from 28 to 31 days.

How does a purchase APR work?

When you carry a balance on your credit card from month to month, you’ll incur interest charges. The APR is the percentage of the outstanding balance that you’ll pay in interest each year.

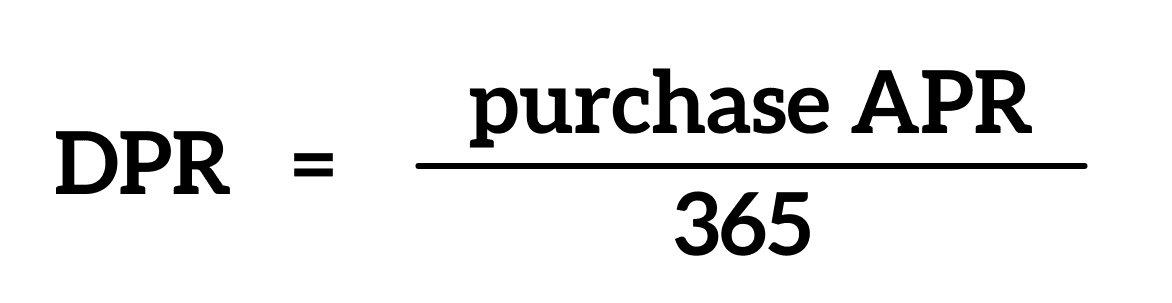

However, your credit card issuer will actually charge you interest based on a daily periodic rate, which is a fraction (1/365) of the APR. To calculate your interest charges for a given period, you’ll need to multiply your average daily balance by the daily periodic rate and by the number of days in the period.

Pro Tip

Before applying for a credit card, it’s always a good idea to check your credit score. This will give you an idea of where you stand in terms of your creditworthiness and can help you determine which cards you’re likely to be approved for. You can get a copy of your free credit report at AnnualCreditReport.com.

Fixed vs. variable APR

APRs can be fixed or variable, and the type of APR you have can affect your monthly interest payments.

- Fixed APR. A fixed APR stays the same no matter what the prime rate (a guiding interest rate that lenders reference) is. This means that your monthly payments won’t change, provided that all other factors remain the same.

- Variable APR. With a variable APR, the credit card’s interest rate can go up or down depending on the prime rate. This means that your monthly payments could change from month to month even if all other factors stay the same. Note that most credit cards have variable APRs.

Introductory vs. regular purchase APR

While many credit cards offer variable APR that may change only slightly, you may also see credit cards with introductory and regular APRs that drastically differ.

- Introductory APR. An introductory APR acts as an incentive to attract new customers to use the particular credit card. For instance, you may see “0% introductory rate for 18 months” as one of the terms of a new credit card. While this sounds like a good deal, it’s important to remember that this rate won’t last.

- Regular purchase APR. Your “regular” purchase APR is the APR your credit card will have once the promotional period ends. This APR may be variable or fixed — and may be a lot higher than you expected — so be sure to review the card issuer’s terms before you get hooked by an introductory rate.

Other kinds of APR

In addition to fixed, variable, regular, and introductory APR, you may come across a few other types of APR depending on the card you search for.

- Penalty APR. If you miss a payment or make a late payment, you may see a temporary increase in your credit card’s interest rate. This is a penalty APR, which a credit card company may enforce if your payment is late by 60 days or more. This increase will typically last for six months, provided you consistently make on-time and full payments for this time.

- Cash advance APR. When you get a cash advance on your credit card, you’re borrowing money from the card issuer. The APR for a cash advance is the annual percentage rate of interest you have to pay for this short-term loan. It’s typically higher than the APR for regular credit card purchases, and you also have to pay additional fees when you get a cash advance. For example, your card issuer might charge a transaction fee of anywhere from 3% to 5% of the withdrawn amount. Keep in mind that cash advances don’t have grace periods. This means you’ll incur interest as soon as you withdraw a cash advance.

- Balance transfer APR. Balance transfers refer to the action of moving your credit card debt from one card to a new one. Some cards may charge additional fees for a balance transfer (usually between 3% and 5%), but others have introductory offers that waive this fee as an incentive.

Pro Tip

If you’re struggling to make payments on high-interest credit cards, you might want to consider taking out a debt consolidation loan or using a balance transfer credit card with a low APR. This can be a good way to reduce your monthly payments and pay off your debt more quickly.

How do you lower your APR?

If you often carry a balance on your credit card and pay interest, you might be wondering how to lower your APR. One way to do this is to simply call your credit card issuer and ask. It doesn’t hurt to negotiate, and you might be surprised at how willing they are to work with you. If they aren’t willing to budge on the APR, you can always shop around for a new credit card with a lower rate. Just make sure you understand the terms of the new card before you make the switch.

Another way to lower your APR on a credit card is by improving your credit score before applying. A good credit score shows creditors that you’re a responsible borrower, which can lead to a lower interest rate. There are a few things you can do to improve your credit score, such as paying your bills on time, maintaining a good credit history, and keeping your balance below 30% of your credit limit.

Pro Tip

Many credit cards offer 0% introductory APR on balance transfers and purchases for anywhere from 12 to 21 months. So, if you have a good credit score, consider applying to these credit cards to lower your interest payments.

FAQs

What’s a good purchase APR?

According to Experian, one of the three major credit bureaus, a good purchase APR is anything that’s below the current average interest rate. In short, there’s no exact number that’s considered “good,” but anything lower than the average is generally seen as favorable.

What is 24% APR on a credit card?

What does the 24% APR on a credit card mean? In short, it’s the amount of interest that you’ll be charged on your outstanding balance if you don’t pay it off before the grace period ends. But as mentioned above, credit card companies calculate your interest payment using the daily periodic rates (APR/365).

So if your APR is 24%, your daily periodic rate would be 0.065%. This means that for every $100 you owe on your credit card, you’ll accrue 6.5 cents in interest each day. Of course, the actual amount of interest you’ll owe will depend on your balance and how long it takes you to pay it off. However, knowing your daily periodic rate can help you budget for your monthly payments and avoid costly surprises down the road.

Do you pay APR if you pay on time?

No. If you pay off your balance in full and on time each month, you don’t have to worry about your APR. But it’s important to note that if you only pay the minimum amount due on your credit card bill, you’ll rack up interest charges since you’re carrying a balance from month to month. So make sure to not only pay off your balance on time but also in full (if you can).

Key Takeaways

- APR, or annual percentage rate, is the interest rate charged on a credit card balance.

- If you carry a balance on your credit card, you’ll be charged interest at the daily periodic rate (purchase APR/365). This rate is applied to your average daily balance and is billed to your account monthly.

- There are two types of APR for credit cards: fixed and variable. Fixed APR means the interest rate won’t change over time. Variable APR means the interest rate could go up or down based on the prime rate.

- Many credit cards offer a 0% APR introductory period. This means you won’t be charged any interest on your balance for a set period of time, usually 12 to 21 months. After the intro period ends, your APR will go up to the regular rate.

- You may also see different APRs for balance transfers, penalties, and cash advances.

Compare credit card APRs

Owning a credit card with a low APR can help you save a good chunk of change in the long run. So if you’re looking for a new credit card, be sure to shop around and consider those that offer 0% introductory rates.

By taking some time to do your research, you can find a credit card that best suits your needs and helps you save money on interest charges.

Table of Contents