What is a Virtual Credit Card? 8 Reasons Why You Need One

Last updated 03/15/2024 by

Lee Huffman

Whether you are shopping online or giving your credit card number over the phone, it can be scary to share your personal information. Criminals are constantly searching for cracks in the system to steal your information.

This is where virtual credit card numbers can protect you. But what is a virtual credit card and why do you need one? Let’s take a look.

What is a virtual credit card?

A virtual credit card is a temporary credit card number that is randomly generated so you can shop online and over the phone without sharing your real credit card information. To further protect yourself, you can limit the amount that can be charged to this virtual credit card number, as well as place an expiration date on the card.

8 reasons you need a virtual credit card number

Credit cards have built-in fraud protection, thanks to the Fair Credit Billing Act.

As a consumer, you are never liable for more than $50 to your credit card as long as you report the unauthorized charges in writing to your credit card company. And it has to be done within 60 days of the statement close date that contained the error.

Many banks have expanded these consumer credit card protections to limit your liability to $0 if you report the unauthorized charges within two billing cycles of when they posted to your credit card statement.

But that protection won’t solve everything. Here are eight reasons you need a virtual credit card number.

1. Replacing credit cards is a hassle

Although credit cards offer protection from fraudulent charges, having to replace your credit card is a hassle. When fraud occurs, you’ll get a new credit card with a new number.

It will take time for the new card to arrive, and you’ll have to update your credit card number with any vendor that you’ve authorized to make recurring charges.

And if you’ve saved your credit card information on any websites to make shopping easy, you’ll have to update those as well.

2. You shop online with a debit card

The fraud risk is even worse for debit card users. With a credit card, if there are fraudulent charges, you can easily dispute the charge and not pay for it while the bank investigates.

However, with a debit card, the money has already left your account. While the bank is researching the fraudulent transaction, you could have payments to your mortgage, car loan, or other bills bounce because criminals drained your account.

According to Regulation E, banks have up to 10 business days to investigate your claim. Those 10 days can feel like an eternity when your bank account balance is $0, and there are bills to pay.

3. Data breaches happen even when you’ve been careful

We’ve all been taught to look for “https” and other safeguards when shopping online. It’s also a good practice to shy away from websites that offer deals that seem too good to be true.

However, even some of the most well-known companies can expose your credit card information through weak website security.

Credit card expert Jon Nickel-D’Andrea of NoMasCoach.com says, “Fraudulent credit card transactions are rare if you stick with the well-established websites like Amazon. But they do happen. Target’s data breach, for example, exposed 41 million credit card numbers.”

According to Kiplinger, several well-known retailers and websites have already been hacked this year with customer credit card information being accessed. Click the links below to see the details of each data breach and the company’s response.

- Orbitz

- Best Buy

- Delta Airlines

The typical retailer response is to provide free credit reporting monitoring for one year, but that assumes that crooks will only try to access your data for one year.

Credit monitoring will alert you when someone tries to open an account in your name, but it won’t stop them from charging fraudulent transactions to your accounts.

4. You have a business credit card

Even though legal protection exists for consumer credit cards, banks do not always provide the same levels of protection for business credit cards.

For example, Visa’s website says, “Visa’s Zero Liability Policy does not apply to Visa corporate or Visa purchasing card or account transactions.” Mastercard has a similar rule, stating that “zero Liability does not apply to the following Mastercard payment cards: commercial cards, or unregistered prepaid cards, such as gift cards.”

If you’re shopping online or over the phone with a business credit card, using a virtual credit card number is an excellent way to limit your risk of fraud.

5. Kids are going to be kids

Children are smarter than ever, and online transactions seem to be part of their DNA. My kids are only three and seven. But I know that they’ll soon be asking for my credit card to purchase something online.

A virtual card allows me to give them a temporary card number that is only good at a single merchant. By doing so, they won’t be able to continue shopping for other goodies or blowing my budget after making the purchase which I approved.

6. Online trial offers that you forget to cancel

We’ve all been enticed to start a trial offer that was free or low-cost. But these companies count on you to forget canceling after the trial period so that they can hit you with an ongoing charge to your card.

John Perri, a credit card expert at JohnTheWanderer.com, says, “I use virtual credit card numbers whenever I do a trial offer. I have peace of mind that they won’t continue to charge me beyond the limits I set on the virtual credit card.”

What John does is smart. He sets a low limit on the single-use virtual credit card so that the recurring charge will get declined and his membership will get canceled.

Before using this strategy, make sure that you read the terms and conditions of the website so that they won’t attempt to bill you or send you to collections for any unpaid charges.

7. You don’t like unexpected charges

With virtual credit card numbers, you can set a specific maximum amount that the charges are approved for. This limits the potential for add-ons to increase the size of the transaction beyond what you are willing to pay.

And when you set the virtual credit number to expire by a certain date, you can be assured that there will not be any additional charges coming down the road.

8. Sticking to a budget is hard

No matter how great you are with your finances, sticking to a budget can be hard.

Set a maximum amount that can be charged with a virtual account number. This can help both you and your spouse stick to your budget by limiting how much you can spend online.

Which banks offer virtual credit cards?

Multiple banks used to offer virtual credit cards, but there are only two banks currently offering them. For example, Discover shut down their program in 2014 when their provider was acquired by Mastercard.

- Bank of America‘s program is called ShopSafe. It is a free service that is available to all credit card customers.

- Citibank offers Virtual Account Numbers, which is also free, but you are required to enroll before using the service.

- Visa and Mastercard offer their own technologies to protect consumers.

- FinTech companies have started offering virtual credit card services that you can use with any bank.

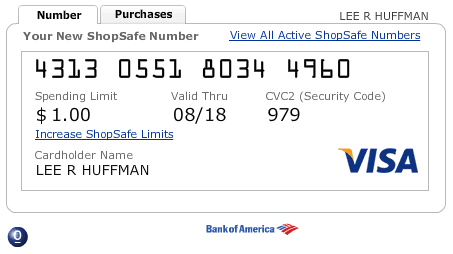

Bank of America’s ShopSafe program

I remember first using ShopSafe with MBNA America to create virtual credit card numbers before Bank of America acquired it in 2005. The experience in creating a new virtual credit card number was just as easy now as it was then.

To show you how secure the system is, I created a Bank of America ShopSafe virtual credit card number and have shared it with you below.

Because I’ve already used this virtual credit card number to purchase something for $1, you won’t be able to use it to buy anything else online.

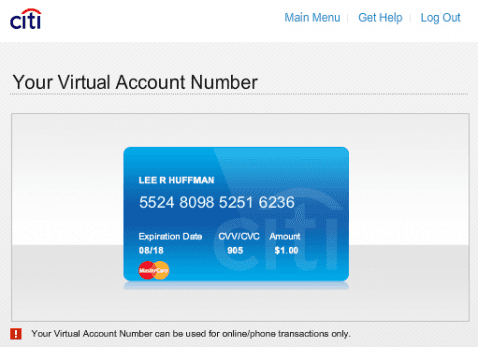

Citibank Virtual Account Numbers program

The Citibank Virtual Account Numbers program is also free. But it requires that you enroll before creating your first virtual credit card number. You only need to register once, after which you can create as many virtual credit card numbers that you need.

Unfortunately, Citibank does not offer their Virtual Account Number service on all of their credit cards. However, a customer service representative informed me that this service is available on 134 of Citibank’s personal and business credit cards.

With that many cards covered, it is likely that you can use the service with your Citibank card.

Visa and Mastercard offer virtual account numbers

Visa and Mastercard offer their own virtual account number platform to help protect your credit card information. If you regularly shop online, you may have seen Visa Checkout or Mastercard Masterpass as a payment option.

Similar to Citibank, you’ll need to register for either of these options, but then you’re all set for future payments. Both Visa and Mastercard also offer apps for your phone or tablet. You can use their programs to pay in-store wherever contactless payments are accepted.

Checkout and Masterpass allow you to register credit cards from Visa, Mastercard, American Express, and Discover instead of limiting your choices only to cards featuring the Visa or Mastercard logos, respectively.

FinTech companies compete for your business

You may not realize it, but you could already be using virtual account numbers when you’re shopping.

Samsung and Apple integrated virtual payment platforms into their phones. This helps protect your credit card information when shopping with your phone. They do so by creating temporary credit card information that is used just for that transaction.

Other FinTechs are also looking out for your sensitive personal data. You’ll need to be proactive to install their apps or go through their website to accomplish this task.

For example, Privacy offers a free virtual credit card number that you can generate directly from your browser. The credit card number closes two minutes after the merchant approves it. Therefore it cannot be used again by the merchant or anyone else who might obtain your information.

Privacy does not charge consumers for this service. Instead, it is paid a fee from the merchants where you use the virtual account number.

Downsides to virtual credit card numbers

There are many benefits to using virtual credit card numbers, but there are some downsides as well.

- When returning items, most merchants want to refund to your original form of payment. If the credit card is closed, that could pose a problem, and you may have to settle for store credit.

- If you use a virtual credit card number to reserve a hotel, airplane ticket, or rental car, they may ask you to show the credit card number at check-in to verify your identity. Because the number was virtual, they may not honor your reservation. At the very least, you could waste time explaining the situation to the desk agent.

- Virtual credit card numbers cannot protect you when buying from a crooked website. If you pay for goods but don’t receive them, you’ll still need to file a claim with your credit card to dispute the transaction and request a refund.

Even though there are some downsides to using virtual account numbers, the positives outweigh the risks. By knowing these potential pitfalls, you can plan to minimize their effect on your shopping.

FAQ on virtual credit card

What is a virtual credit card?

A virtual credit card is a temporary credit card number that is randomly generated so you can shop online and over the phone without sharing your real credit card information. To further protect yourself, you can limit the amount that can be charged to this virtual credit card number, as well as place an expiration date on the card.

Are virtual credit cards legal?

Virtual credit cards are not illegal, however, they are not completely anonymous. Their primary use is intended to secure your information from criminals. If you are trying to purchase illegal goods using Tor or something, your payments can still be tracked by your bank.

How do I get a virtual credit card?

- The first thing you need to do is create a card of the required denomination. For this contact your bank.

- Then the bank will provide you with a 16 digit virtual credit card number.

- Enter this credit card number that is generated.

Which bank offers virtual credit cards?

Multiple banks used to offer virtual credit cards, but there are only two banks currently offering them.

- Bank of America‘s program is called ShopSafe. It is a free service that is available to all credit card customers.

- Citibank offers virtual account numbers, which is also free, but you are required to enroll before using the service.

Are there any downsides to virtual credit cards?

The biggest negative for virtual credit card numbers is that they only work online. You can’t use a virtual credit card in a situation where you’d swipe a physical card. Also, returns can be problematic if the virtual card you used has expired; you might have to take store credit.

Should I use a virtual credit card?

You have several choices to protect your personal information when shopping online or over the phone. Virtual account numbers protect your credit card numbers and reduce the opportunity for fraudulent transactions.

Nothing is foolproof, but adding a layer of security can prevent unwanted purchases. It can also limit the damage if a hacker steals your information.

Enroll your credit cards now so that you’ll be ready to use a virtual credit card the next time you shop online.

Lee Huffman is a former financial planner and corporate finance manager who now writes about early retirement, credit cards, travel, insurance, and other personal finance topics. He enjoys showing people how to travel more, spend less, and live better.

Table of Contents