Enterprise Value vs. Market Cap: What’s The Difference?

JD

Summary:

Market capitalization can give a general idea of how risky or aggressive a certain investment might be. However, certain factors are left out of market capitalization, such as a company’s debt and cash reserves. Enterprise value is meant to show the overall value of a company but isn’t the best metric to use when comparing companies across industries. Both of these metrics play a vital role in making savvy investment decisions.

Determining the value of a company plays a vital role in the finance industry. Various valuations help investors make better investment decisions as well as enable investors and analysts to foresee the potential future earnings of a company. Market capitalization and enterprise values are two such valuation metrics used in the industry.

This article gives an in-depth view of what both market capitalization and enterprise value mean, how they are used, and their differences.

Compare Business Loans

Compare rates, terms, and community reviews between multiple lenders.

What is market capitalization?

First, let’s define market cap. Market cap is the overall market value of a company’s total outstanding shares. These outstanding shares include a company’s stock currently held by its shareholders, share blocks held by institutional investors, and restricted shares owned by the company’s officers and insiders. Outstanding shares can be found on a company’s balance sheet under “Capital Stock.”

How is market cap calculated?

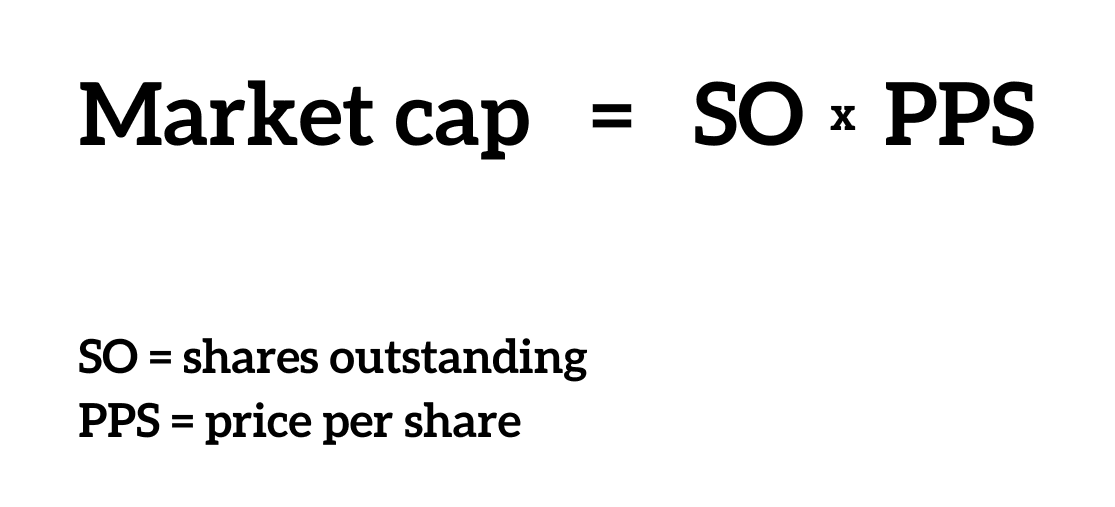

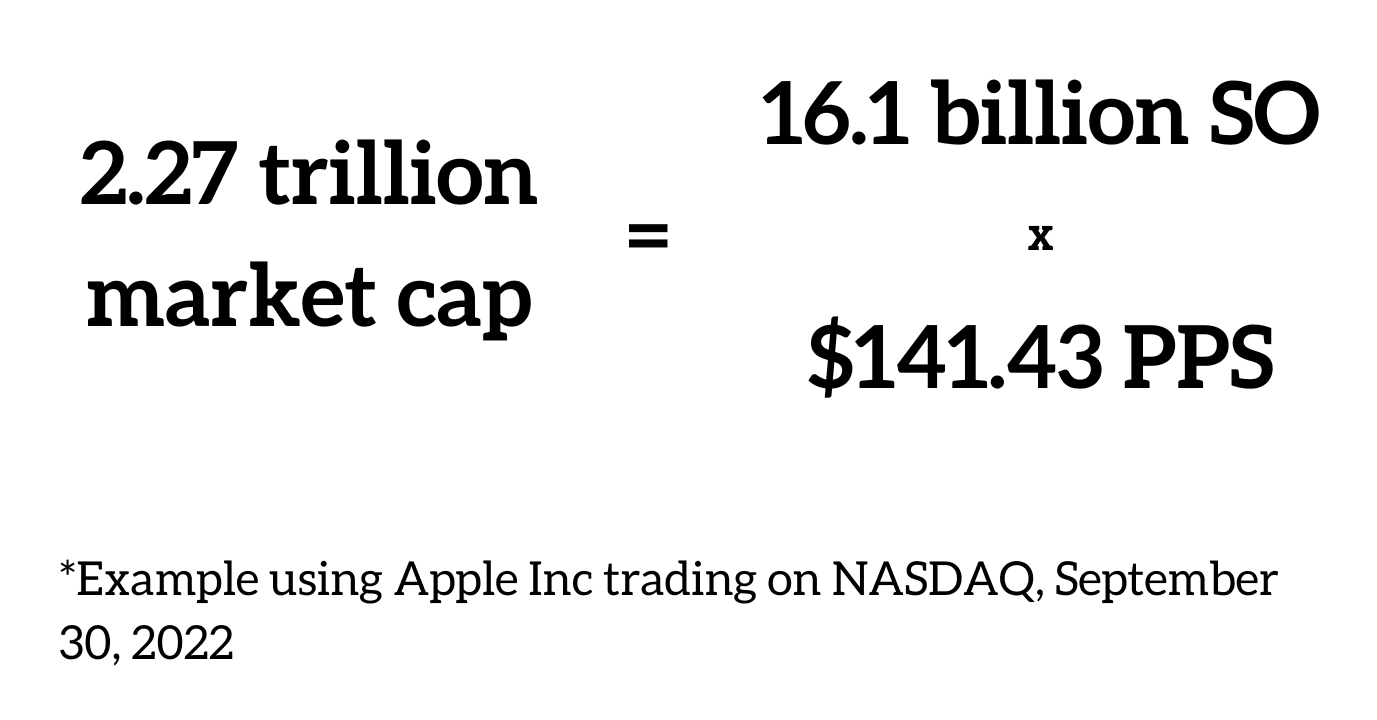

Market cap is calculated by multiplying a company’s current market price (stock’s current share price) by the number of outstanding shares. For example, if a company has 100 million shares outstanding and the current stock price per share is $100, the market cap is $10 billion.

- Share outstanding = the total number of a company’s stocks held by its shareholders, excluding preferred shares.

- Price per share = the company’s current market stock price as listed in an individual stock market such as NSE, BSE, NYSE, NASDAQ, etc.

The free-float method

One method of calculating market cap is called the free-float method. This method excludes locked-in shares such as those held by company executives and governments. The free-float method is the most commonly used method to calculate market cap by the majority of the world’s major indexes, including the Dow Jones Industrial Average and the S&P 500.

Investment strategies using market cap to create a diversified investment portfolio

Why should you consider market cap when deciding on an investment strategy? Understanding market cap allows investors to comprehend the relative size of one company compared to another. Market cap not only measures what a company’s worth is on the market but also gives an idea of the market’s perception of its prospects based on what investors are willing to pay for the company’s stock.

If you’re investment strategy primarily targets pursuing long-term financial goals, comprehending the connection between company size, return potential, and risk is crucial. Knowing these factors will help you to build a balanced stock portfolio that comprises a mix of “market caps.”

Companies are typically classified into the following three categories based on their market cap:

| Small-cap | $300 million – $2 billion |

| Mid-cap | $2 billion – $10 billion |

| Large-cap | $10 billion and up |

Small-cap

Small-cap companies are generally businesses with a market cap value between $300 million to $2 billion. These lower market cap companies are typically newer and often a part of emerging industries or markets.

Of the three categories, small-cap stocks tend to be the most aggressive and risky. However, they also have the greatest potential for significant growth for investors who can tolerate stock price volatility.

Mid-cap

Mid-cap companies are generally businesses with a market cap value between $2 billion and $10 billion. These companies are typically established in industries experiencing or expected to experience rapid growth.

Mid-cap stocks are generally less risky than small-cap stocks. Although mid-caps often offer more growth potential than large-caps, they also tend to be riskier than large-caps.

Large-cap

Large-cap companies are generally businesses with a market cap value of $10 billion or more. These firms are often within established industries, generally more familiar to the national consumer audience, and have a reputation for providing quality goods or services.

Therefore, large-cap companies are associated with more consistent dividend payments and steady growth. That said, they’re also considered more conservative than small-cap or mid-cap stocks since there is less overall growth potential.

Why market cap is important

Market cap is one of the most commonly used metrics for determining the value of a company and a good starting point to analyze companies. A company’s market cap size (small, mid, or large) can give insight into the risk potential of the company.

Keep in mind that there are limitations to the market cap metric. Market cap does not take into account a company’s debt or cash. A company with a high market cap can potentially be less valuable after considering its debt. This is where enterprise value comes in handy.

Pro Tip

Although equity value and market capitalization are somewhat similar, and even at times used interchangeably, there is a key difference between the two. Equity value adds enterprise value with redundant assets (non-operating assets) and then subtracts the debt net of cash available. On the other hand, market capitalization only considers the value of the company’s common shares.

What is a company’s enterprise value (EV)?

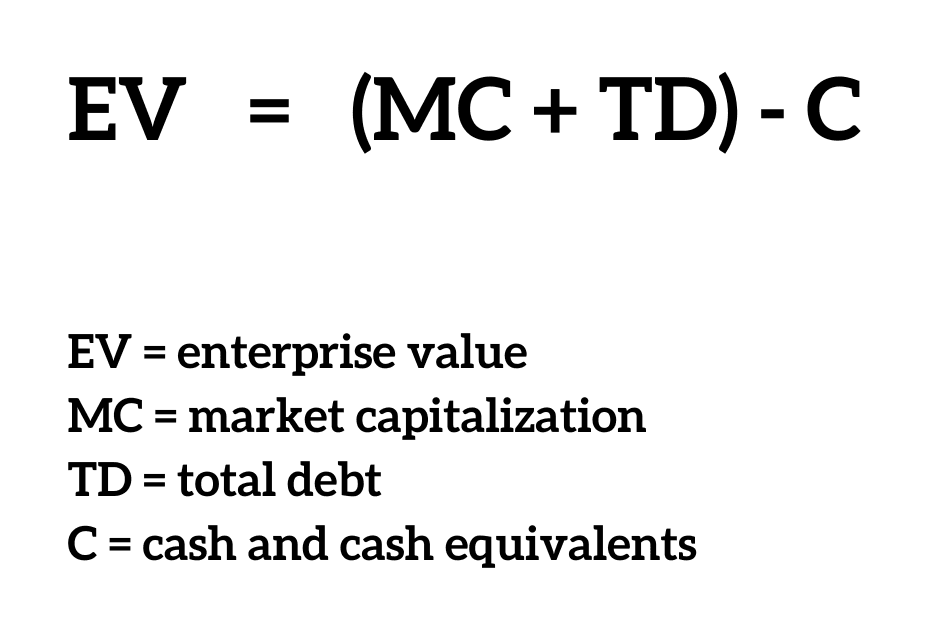

To calculate enterprise value, take a company’s market capitalization value and factor in the short-term and long-term debt, as well as its cash and cash equivalents. This figure represents the entire value of the company.

Main components of enterprise value

- Market capitalization. As mentioned earlier in this article, this is the overall market value of a company’s outstanding shares. Market cap is calculated by multiplying shares outstanding by the share price.

- Total debt. This is the sum of a company’s liabilities and is identified on the company balance sheet. Liabilities can be broken down into short-term debts (current) and long-term debts (non-current). Short-term obligations are expected to be fulfilled within 12 months, whereas long-term obligations involve payments exceeding 12 months. Debt can give a company a tax shield advantage and can be used to lower the cost of capital. However, rising debt conditions in an organization should be analyzed carefully to determine the risk of bankruptcy.

- Cash and cash equivalents. Cash and cash equivalents are the total value of cash on hand, including items that are similar to cash, and must be current assets. A company’s combined cash or cash equivalents is at the top line of the company’s balance sheet and are the most liquid assets.

Factoring in minority interest

When a company owns more than 50% of a subsidiary (but less than 100%), the company will record all of the subsidiary’s revenue, income statement items, and costs, even though the company does not own 100% of the subsidiary. Therefore, to determine a company’s enterprise value, minority interest (the value of the subsidiary not owned by the parent) must be factored in.

Why enterprise value is beneficial

Enterprise value is a comprehensive metric that takes into account a company’s debt and cash to help investors find the fair value for a company. This metric also helps to analyze data to determine the value of a merger, trade, or acquisition.

However, there are limitations to enterprise value. As stated earlier, enterprise value includes total debt, but not all debt is the same. How a company manages and is utilizing its debt is a key factor.

One example of this is capital-intensive companies such as ones in the oil and gas industry. These companies typically carry a significant amount of debt that can be vital for growth. The debt may have been used to purchase plants or equipment. Enterprise value can therefore give a skewed view when comparing companies across industries.

Market cap vs. enterprise value

The key difference between market cap and enterprise value is that market cap does not include a company’s debt and cash. Therefore, enterprise value is more comprehensive than market capitalization.

Differences in practical terms

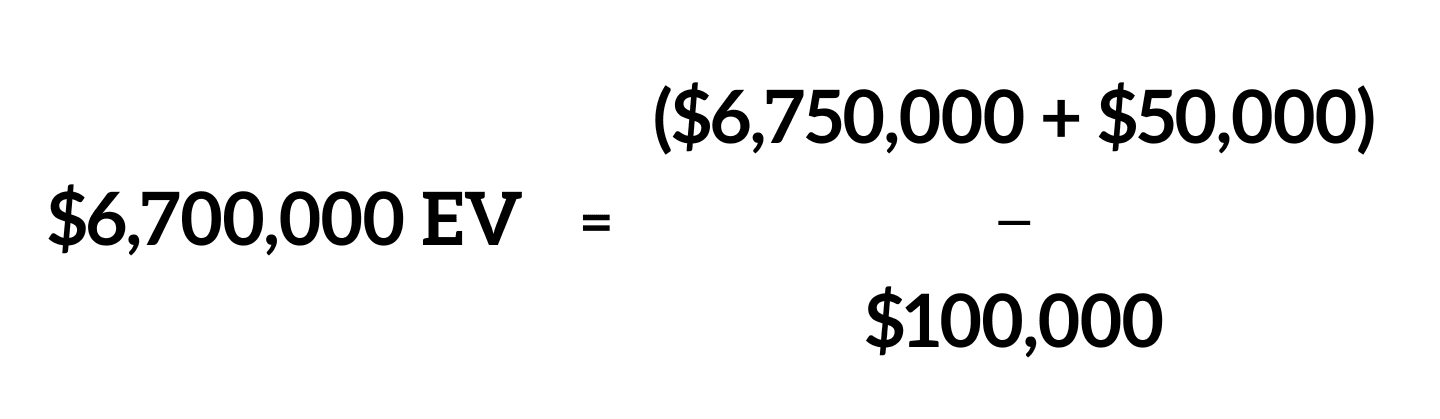

Let’s say there are two manufacturers, Company A and Company B, who have the same stock price of $2.25 per share. Each company has 3 million outstanding shares. This would bring the market cap of both companies to $6.75 million.

Let’s say Company A has $100,000 in cash and cash equivalents and $50,000 in total debt. Therefore it’s enterprise value would be calculated as follows:

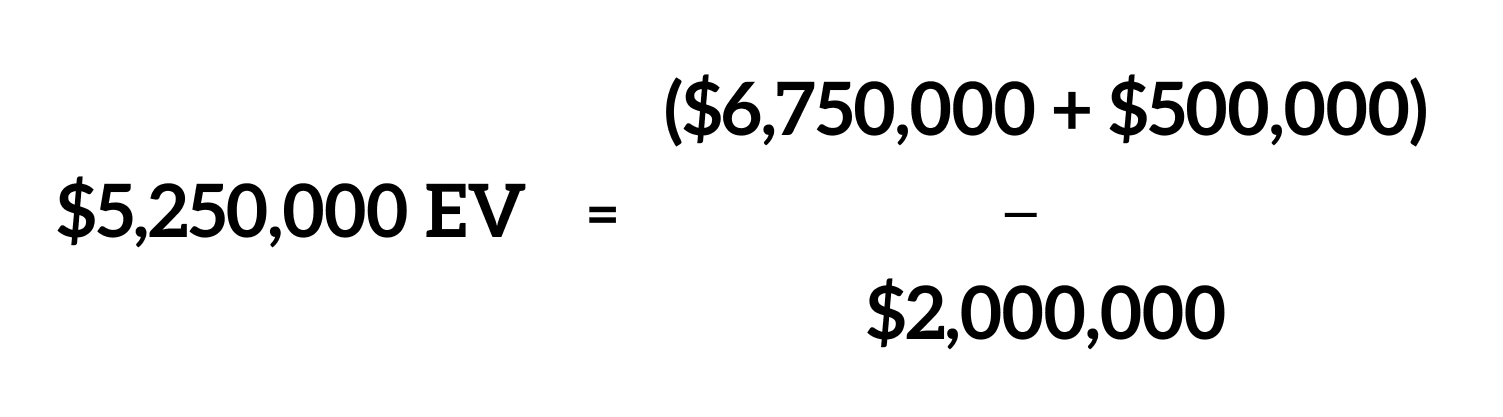

Now let’s say Company B has $2 million in cash and cash equivalents and $500,000 in total debt. Therefore it’s enterprise value would be calculated as follows:

The companies looked identical using market cap, but a different picture appears when each company’s enterprise value was calculated.

Which is a better metric?

The answer to this question depends predominantly on your investment goals. If you’re primarily interested in growth potential, market cap may be a better metric to use. On the other hand, if you’re looking for companies that are potentially undervalued, enterprise value can be a better metric since it takes into account a company’s debt and cash.

For a deeper conversation about your investment opportunities, try speaking with one of the investment advisors below.

FAQs

Is enterprise value usually higher than market cap?

A company’s enterprise value will be higher if it has a positive debt situation (debt levels higher than cash and cash equivalents). However, in the case of a net cash position (debt ratio lower than cash and cash equivalents), the market cap will be higher than the enterprise value.

What is a good enterprise value?

Good enterprise values can vary by industry. Put frankly, enterprise value is not always the most helpful metric when deciding whether to buy stock in a company. A more helpful metric can come from comparing enterprise value to a company’s cash flow or the earnings before interest and taxes (EBIT).

That being said, enterprise value works better than market cap for evaluating companies with different capital structures (i.e., debt and cash levels).

What is enterprise value to market cap ratio?

Enterprise value to market cap ratio helps to identify a company’s capital structure. Dividing the enterprise value by market capitalization also can give a glimpse of what the enterprise value is comprised of.

A higher enterprise value to market cap ratio is generally not preferred. It would indicate that the firm has high levels of debt and preference shares. These types of firms are generally a more risky investment. When the enterprise value to market cap ratio is lower, this reflects a lower debt level and is considered a relatively safe investment.

Keep in mind though, there are a few limitations to using the EV/market cap ratio.

- This ratio doesn’t factor in the growth rates of the company.

- A low EV/market cap ratio will not always indicate a company’s financial health. You cannot tell if the company’s free cash flow is shrinking and making it incapable of repaying its debt.

Key Takeaways

- Enterprise value and market cap are two metrics used to assess a company’s value and investment risk.

- Market cap provides the estimated overall value of a company based on that company’s outstanding shares. While market cap is helpful when comparing company size and value, this metric ignores a business’s cash and debts.

- Enterprise value, on the other hand, examines the entire value of a company by examining its market capitalization, cash and cash equivalents, and total debt. However, this metric can be misleading when comparing companies across industries.

- Be sure to recognize the pitfalls these calculations contain and use both metrics when deciding which company to invest in.

Share this post: