Fixed vs. Variable Student Loan Rates: 4 Key Factors to Help You Choose

Last updated 03/19/2024 by

Jessica Walrack

When applying for student loans, many lenders give you the option between a fixed and variable interest rate. But what’s the difference and which one will be better for you?

If you aren’t sure which one to choose, read on. We’ll cover the way both rates work, their pros and cons, and four factors you should consider when making your decision.

Fixed rate loans

Fixed rate loans have an interest rate that doesn’t change over the course of the loan. You apply, lock in the rate, and pay it for the entire term.

The interest rate you’ll get is determined by the market conditions when you apply, your creditworthiness, and the length of the loan.

The pros? “For planning and repayment purposes, fixed rate loans tend to work better than variable rate loans since they allow the borrower to eliminate a potentially unknown variable that could affect their repayment and other financial plans,” says Ross Riskin, CPA/PFS and Founder of the American Institute of Certified College Financial Consultants.

You can plan your budget knowing that your student loan payment is always going to remain the same. The downside is that fixed rates are often higher than introductory variable rates and may end up costing more over the life of the loan.

You take the risk of paying more for the security of knowing that your rate will always be the same.

Variable rate loans

Like fixed interest rates, variable interest rates are also determined by the market conditions, loan length, and your creditworthiness. The difference is that a variable rate will not remain the same over the entire term of your loan.

Choosing a rate really depends on your individual needs. Variable rates offer a lower starting rate but can fluctuate from month to month based on the market. Fixed rates offer one rate for the life of the loan regardless of market movements.”

Instead, they fluctuate (usually at fixed intervals) depending on the index they are tied to– most commonly the London Interbank Offered Rate (LIBOR) for student loans. Caps are usually placed on how much your rate can change to provide some sense of security.

Riskin says, “Student loans with variable interest rates tend to look more attractive on the surface, as they are often advertised as being more affordable than fixed rate loans. But the rate also has the ability to change every year (or month) and may eventually move higher than the stated fixed rate.”

So, how do you decide which one will be best for you?

4 factors to consider when choosing a fixed or variable interest rate

You may be a bit confused about whether a fixed or variable interest rate will be better for you. To help you figure it out, here are four main factors you should consider when making your decision.

1. Loan length

The longer the period of a loan, the more likely it is to be impacted by changing interest rates. More time means the possibility of more changes, which can cause interest rates to rise or fall significantly.

That being said, you can limit your risk by opting for a shorter term loan (under 60 months) when choosing a variable interest rate, and getting a fixed rate with a longer term loan.

2. Current interest rate environment

In addition to loan length, the current interest rate environment should also play a role in your decision. If rates are expected to remain stable or drop, a variable interest rate will be more beneficial.

However, if it looks like they’re going to rise, a fixed rate will likely end up being cheaper.

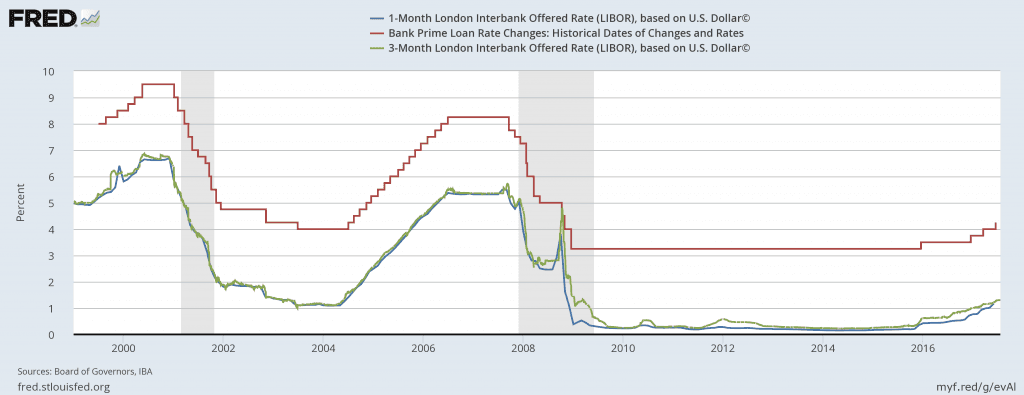

For example, look at the change in the LIBOR since 1999.

If you were to sign up for a five-year loan with a variable interest rate in 2004, your interest rate would have steadily increased and remained high for the following three to four years. In this case, a fixed rate would have been better because it would have locked you in at the lower rate.

Now fast-forward four years to 2008, and it’s a whole new situation. If you got a variable interest rate loan in the beginning of 2008, your rate would’ve steadily dropped, helping to save you money, while the fixed rate would’ve remained much higher.

While the rates have been more stable over the past seven years, it’s wise to research current trends and interest rate increases by the Federal Reserve to help you predict which direction it will go in.

3. Your Budget

CommonBond CEO David Klein says, “Choosing a rate really depends on your individual needs. Variable rates offer a lower starting rate but can fluctuate from month to month based on the market. Fixed rates offer one rate for the life of the loan regardless of market movements.”

You’ll need to analyze your budget to determine what payments you can afford. While variable rates might save you money in the beginning and over the long run, there may be months when your payment goes up. You need to figure out if you’ll be able to afford those increases.

Also, to reiterate the point above, your loan length is a key factor in which type of interest you should choose. The shorter your loan, the higher the payments. You’ll need to decide which loan length and interest rate combination creates the best balance between overall value and affordability.

4. Importance of predictability

To help make the right decision, you need to ask yourself how important predictability is to you.

“Remember that interest rates could rise higher than the previous highs. If you’re comfortable assuming a little more risk in your payment amount, a variable rate loan does have the potential to offer more savings,” says Vince Passione, CEO of Student Loan Financing Company LendKey.

That’s a question only you can answer. If you like the stability of knowing exactly what to expect, a fixed rate is the way to go. If you have researched the market environment and would like to take the risk with a variable rate, it will lack the security but may earn you some extra savings.

By taking these four factors into consideration, you can figure out which loan type will best suit your needs.

Get the best deal on your student loans

Now that you have a better understanding of how to choose between fixed and variable interest rates, it’s time to find the lender that can offer you the best deal.

By shopping around, getting pre qualified, and comparing offers from various companies, you’ll be able to find the most affordable loan solution.

A helpful bonus is that most lenders allow you to apply online without hurting your credit score. To get started, head over to the Student Loans Review Page and compare a list of top lenders.

Jessica Walrack is a personal finance writer at SuperMoney, The Simple Dollar, Interest.com, Commonbond, Bankrate, NextAdvisor, Guardian, Personalloans.org and many others. She specializes in taking personal finance topics like loans, credit cards, and budgeting, and making them accessible and fun.

Share this post:

AddTable of Contents