How to Become a Landlord: 6 Steps to Successfully Rent Your Property

Summary:

You can become a landlord by choosing and fixing up a rental property, creating a lease agreement, and advertising your property’s availability. However, being a profitable landlord comes with major undertakings like managing finances, handling repairs, and staying on top of your tenants.

Rental real estate is an incredibly lucrative source of passive income, and everyone wants a piece of it. Individual landlords made over $300 billion in rental income in 2018, according to the Pew Research Center.

Having investment properties and collecting rent is one of the most reliable ways to build wealth. However, a first-time landlord may find the entire rental process daunting and need help knowing where to begin. To help, we’ve outlined six crucial steps to take to become a successful landlord.

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

What is a landlord?

A landlord is a property owner (an individual, business, or other entity) who rents or leases their rental property for income to a “tenant.” And though becoming a landlord has the potential to be a financially rewarding endeavor, David Bitton — co-founder and CMO of DoorLoop a property management software service — points out that it requires upfront costs, time, and energy.

Being a successful landlord requires organization, excellent communication, and commitment. It’s no easy feat, but if you’re ready to profit from your investment properties, we’re here to give you the rundown on how to become a landlord.

1. Find a rental property

To become a landlord, you’ll first need a suitable property. “Landlords should begin by identifying a property that is in a desirable location, has the potential to generate positive cash flow, and is in good condition,” says Matthew Martinez, real estate broker and CEO at Diamond Real Estate Group.

Pick a property type

There are three types of rental properties you can choose from: a single-family home, a condo, or a multifamily home. If you’re a first-time landlord, a single-family home is a good place to start.

Choose the right location

Choose a rental property in a livable community with nearby amenities. Also, consider researching areas with projected growth in employment rates and development plans for more considerable home appreciation. This may help attract renters to your location.

Since finding tenants may be challenging if you purchase a rental property in areas with high vacancy rates, natural disasters, or crime, make sure to research those statistics in any potential area.

Finance your rental property

Be aware that underwriting may be stricter for those purchasing an investment property. Lenders may have higher standers regarding credit scores and debt-to-income ratios. Also, you may have to shell out more for your interest rates and down payment.

You can use two loan programs to finance your rental property: conventional loans or second mortgages. While not backed by the government, a conventional loan is a great and flexible way to finance your rental property. You’ll need about a 620 credit score to qualify for this loan program.

On the other hand, a home equity loan or home equity line of credit (HELOC) allows you to use your primary home as collateral to take out a second mortgage. If you have a lot of equity built up in your primary residence, you may find that a HELOC or home equity loan (like those below) is better than a conventional mortgage.

Pro Tip

Federal Housing Administration (FHA) and VA loans help homebuyers purchase primary residential properties, not investment properties. However, you may qualify for one of these mortgage programs if you buy a multi-family home (like a duplex) and live in one of the units.

2. Establish a budget

You want to ensure your chosen rental property fits your budget and delivers positive cash flow. Keep in mind that there are expenses outside of your mortgage payments. You want to ensure that every cost is accounted for so your business generates profit.

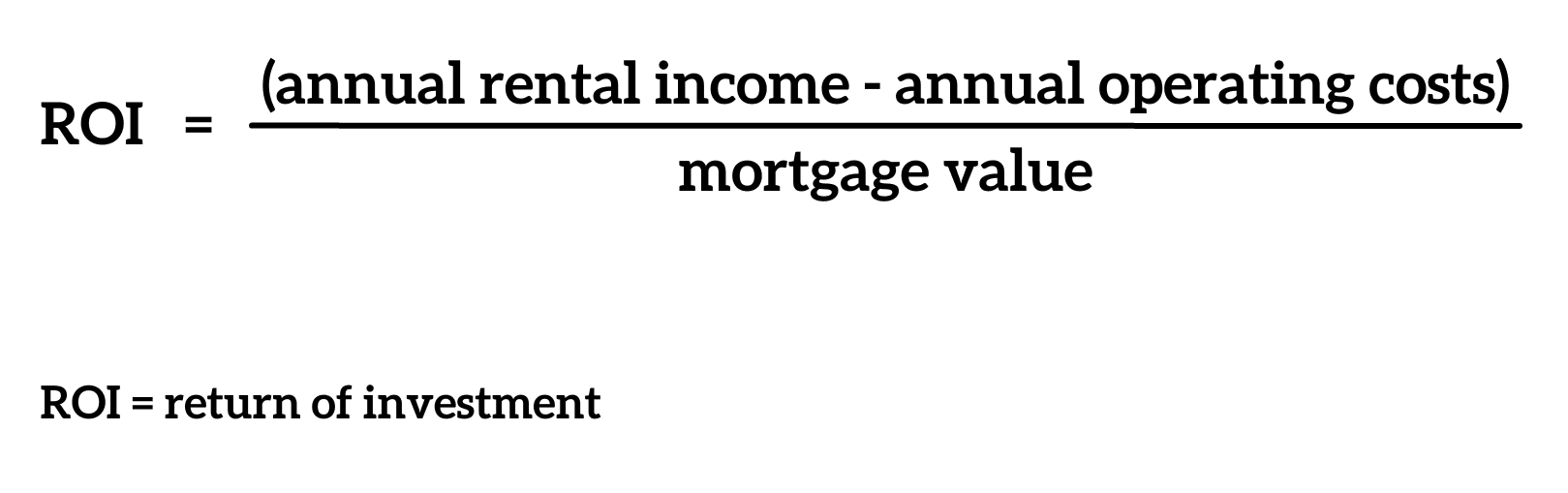

Calculate your return on investment

Use a return on investment (ROI) calculator to determine your profit margins. Or, if you prefer to do your own calculations, use the template below to get a better idea of what your ROI might be.

Determine what you’re going to charge for your rental property

Use the 2% rule to set your monthly rent for an investment property as a general rule of thumb. The 2% rule states that the rent cost should be no less than 2% of the purchase price. For example, if you buy a property for $200,000, you should set the monthly rent at no less than $4,000.

You can use rent estimator sites like Rentometer and Redfin to gauge the rental market and estimate rent in your area.

Operating cost

Operating costs are the expenses incurred to manage your rental business. For instance, like a primary home, you’ll have to pay for the mortgage, utilities, taxes, maintenance, repairs, homeowners insurance, and HOA fees.

There are also operating costs exclusive to landlords, including but not limited to the following:

- Landlord insurance. Landlord insurance covers the structure and foundation of your rental properties and any liability if someone gets hurt or injured on your property. If you purchase landlord insurance, it may cost 25% more than homeowners insurance at an average of $1,590 per year.

- Tenant screening. A standard criminal background and credit check can cost between $45 to $135 per applicant. This could rack up depending on how many applicants you choose to screen.

- Marketing. Marketing can cost virtually zero to thousands of dollars for professional property marketing.

- Potential litigation. Knowing your local landlord-tenant laws can help avoid legal conflicts. However, in preparation for the worst-case scenario, storing several hundred dollars in an emergency fund doesn’t hurt.

- Bookkeeping and accounting. For DIY bookkeeping, accounting software can run anywhere from $9 to $1,000 per month. You can also hire an accounting professional, which may charge you an average of $175 per hour for their services.

- Property manager fees. Property managers generally charge 6% to 12% of the property’s monthly rental income. However, having a good property manager can help reduce tenant turnover, decreasing income loss from vacancies and evictions.

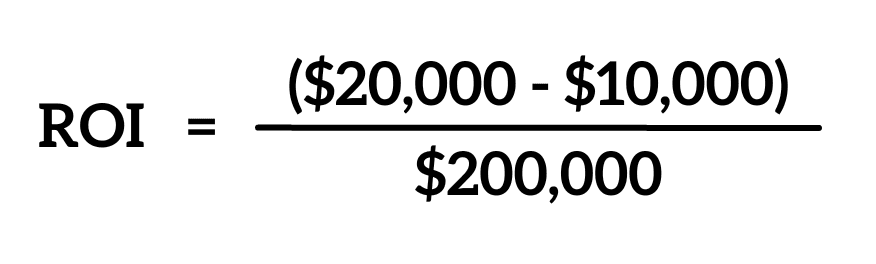

Return on investment example

Let’s say your annual rental income is $20,000, your annual operating cost is $10,000, and the mortgage value is $200,000. Your calculations will look something like this:

The ROI on your investment property would be 5%, meaning that you’ll make 5% of your investment in profit or $10,000.

Pro Tip

Perform an ROI regularly to see where you stand regarding the profit and loss ratio. Inflation can shift maintenance costs dramatically, so it’s essential to know how rising costs affect your profit margins.

Set money aside for maintenance costs

Experts recommend saving up to 1% to 4% of your rental property’s value for a home maintenance fund. For a more exact estimate, create a list of home systems and appliances that may need upkeep and how much it would cost to maintain them.

For example, here’s a list of common household repairs you may encounter:

- Roof (asphalt): $5,443 – $11,206

- Deck (wood/composite): $15 – $30 per square foot

- Furnace: $2,150 – $5,900

- Central air conditioner: $3,811 – $7,480

- Water heater (gas/electric): $812 – $1,575

- Garage door opener: $218 – $511

- Windows: $200 – $1,800 each

IMPORTANT! Be sure to account for vacancies or if the renter can’t make a payment and set aside funds to cover this cost.

3. Get your investment property move-in ready

“Landlords will need to prepare the property for rental, which may include making repairs, painting, and landscaping,” says Martinez.

Preventative care

Part of maximizing your profit is minimizing your maintenance costs. You can protect your investments by tenant-proofing your property.

- Walls. Minimize damage to your walls by opting for paint with a glossy finish instead of matte. In addition to this, installing a door stopper prevents your door from chipping your wall’s paint. Finally, you can include a clause in the lease agreement prohibiting your tenants from puncturing your walls.

- Floors. Protect your floors by avoiding carpet and hardwood floors and opting for durable bamboo, vinyl, or laminate flooring.

- Doors. Use plexiglass for your doors instead of having a screen or storm doors.

- Tenant-proof your lease agreements. Make sure you include a detailed description of how you want your tenants to care for your property. For example, you may require your tenants to have felt pads under the furniture to prevent scratches to the floor.

Maintenance and safety check

At least once a year, go through this checklist to ensure the property is in good shape before you send it off to your tenants.

- Ensure no pest issues are building up.

- Walk through your property and inspect any water leakages or drips in faucets or toilets.

- Refresh shower caulk and grout.

- Patch cracks in ceiling or drywall.

- Replace filters in AC and furnace.

- Flush the water heater.

- Check smoke and carbon monoxide detectors.

4. Find prospective tenants

“Landlords should advertise the property and screen potential tenants to ensure that they are reliable and able to pay the rent,” says Martinez.

Market your property

Marketing your rental unit makes prospective renters aware of your property, which draws potential tenants to apply. Key information to have in your listing includes the:

- Price of the rental unit

- Price of the security deposit

- Number of bathrooms and bedrooms

- Type of property

To ensure your listing stands out, highlight your unit’s unique features and amenities. Along with this, make sure to include good pictures of the property and amenities, which can make or break your listing. Consider hiring a professional to take the photos. Finally, you’ll want to disclose the minimum criteria for tenant screening, like credit scores and monthly income requirements.

You can list your rental property online, such as Zillow, Craigslist, or Facebook Marketplace. If you prefer to start small, ask around your neighborhood and find a tenant through word of mouth.

Screening tenants

Having minimum requirements for tenant screening can weed out potentially troublesome tenants. Credit scores, income, and criminal history are just a few criteria to vet a prospective tenant.

Many landlords identify responsible tenants by running a credit score check, which may provide a better idea of how trustworthy prospective tenants may be. Similarly, running criminal background checks will identify applicants with misdemeanors and felonies. A background check will also reveal registered sex offenders and those with eviction records, which may put your rental property at risk.

Finally, you’ll want to guarantee your new tenant can make rent payments as it affects your bottom line. You may ask for proof of income, like the renter’s last two paystubs or a W-2 from the renter. Many landlords require a tenant’s income to be 2.5 to 3 times the rent and ask for security deposits to ensure prospective renters keep the property in good condition.

Pro Tip

Landlord-tenant laws and fair housing laws protect prospective tenants from discrimination. Familiarize yourself with local tenant laws to ensure you screen each applicant fairly.

5. Create a lease agreement

Lease agreements protect landlords and tenants by ensuring both parties uphold their end of the contract.

Build your lease agreement

A lease agreement allows you to set the terms for renting your property. So, it’s necessary for your contract to be as specific as possible to protect your property. These are some details all landlords should include in their leases:

- Names of all tenants

- Occupancy limits

- Tenancy terms

- Specifics related to paying rent (how much, due date, method of payment, etc.)

- Specifics related to the security deposit and fees

- Restrictions and responsibilities of tenants regarding repairs and maintenance

- Entry to rental property

- Restrictions on illicit activity

- Rules on pets

- Other restrictions

Pro Tip

Sites like Zillow Rental Manager can help you build a lease agreement, so you don’t have to do it from scratch.

Run the lease by a legal professional

Hire a real estate attorney to review your lease to see if it’s foolproof and doesn’t breach a landlord-tenant law. Despite the high cost of legal fees upfront, having an attorney review your agreement can prevent further legal fees later if your renter decides to take you to court.

Review the lease with your tenant

Schedule an appointment with your new tenant to review the lease. Consider sending over a copy of the lease agreement before conducting the meeting, so your renter knows what you will discuss.

Discuss every line of your contract, and explain any complicated or unique terms. After you review the lease agreement, invite your renter to ask questions. Being as thorough as possible can save you the hassle and headache of potential contract violations.

Finally, have all your tenants or tenant sign the lease, give them a copy, and store your copy securely.

6. Decide if you want to hire a property manager

Becoming a landlord can be financially rewarding but requires time and effort. And taking a do-it-yourself approach may not be practical if you plan to rent out multiple properties. That’s where a property manager can come in to save the day.

A good property management company will assist you with setting accurate rates, advertising, finding tenants, managing vendor relationships for maintenance, and ensuring your property is up to code. Property managers can also ensure tenants are making rent payments, manage tenant conflicts, and handle emergency and routine maintenance.

A reliable property management company can cost 6% to 12% of your monthly rent payments. However, property managers can help you maximize profits while minimizing time, so you can focus on expanding your business and growing your income.

Pro Tip

Consider purchasing property management software as an affordable alternative to a property manager. Property management software can help you with “listing your rental, accepting and sorting tenant applications, screening applicants, signing lease agreements online, setting rent reminders, collecting rent, and scheduling maintenance,” says Bitton.

Pros and cons of being a landlord

Becoming a landlord is an excellent way to earn passive rental income and build equity in your property. However, if it were simple, everyone would be owning rental properties. Before becoming a landlord, weigh the benefits against the risks to determine if this is a responsibility you can take on.

Is becoming a landlord worth it?

With countless success stories of double-digit returns, becoming a landlord can be a profitable endeavor. However, the job is not a get-rich-quick scheme.

Even if you hire a property manager to handle your property, you’ll need to find a rental that generates positive cash flow. And even with a property manager, you’ll likely experience dry months with vacancies and evictions.

If you forgo property management assistance, your work will significantly increase. As a landlord, you’ll have to stay on top of your game to ensure your property generates profit and you keep your tenants happy. On top of that, you have to get intimately familiar with local landlord-tenant laws in your area to avoid costs associated with legal issues.

So, if you’re financially savvy, organized, and committed to learning the rental process, becoming a landlord might be up your alley.

FAQs

Do you have to register as a landlord?

Landlord registration will vary by municipality. However, many major cities will require a rental registry to collect data on rentals in the area and enforce rent regulations.

Why being a landlord is hard?

As a landlord, you’re essentially running a business. Your core responsibilities include completing routine repairs, paying the bills, managing tenants, and other tasks. While a property manager can reduce the workload, you’ll still have to shoulder the start-up costs and ensure you’re getting a positive return on your investment.

Do landlords get rich?

Yes, you can build wealth and profit substantially by being a landlord. However, you can lose a considerable amount as well. Profitability is contingent on your rental income being greater than your operating expenses.

Do I need a license to rent my property?

Depending on your city and state, you’ll likely need a license to rent your property. To obtain a permit, you may have to undergo an inspection to ensure the rental meets your city’s safety regulations.

Do you get taxed as a landlord?

The Internal Revenue Service (IRS) typically requires you to report all amounts you receive for rent in your gross income. This income includes advance rent, security deposits (used as final payments), and fees for lease cancellation.

If you receive property or services from your tenant (e.g., your tenant paints the property regularly instead of paying two months of rent), you must include the increase in property value or services in the equivalent of two months on your tax return.

Key Takeaways

- A landlord is a property owner who rents out their unit to a tenant.

- Though being a landlord can be financially rewarding, it comes with start-up costs and time commitments. Additionally, there’s no guarantee you’ll get a return on your investment with evictions and vacancies.

- Profitable landlords will buy property in a lucrative area, minimize operating costs, and set a competitive monthly rent rate.

- A successful landlord will also prepare for the worst by having funds set aside for maintenance and cost related to legal issues.

- Finding responsible tenants will ensure your property remains in the best shape and reduce costs associated with evictions.

- Hiring a property manager can help you reduce your time finding potential tenants, conducting routine and emergency maintenance, collecting rent, and more.

Share this post:

AddTable of Contents