How to Get Approved for Store Credit Cards

Last updated 03/19/2024 by

Ben Luthi

Store credit cards don’t offer the same caliber of rewards and perks as some of the best credit cards on the market. But if you have bad credit, they might be a solid choice.

To get approved for a store card, you’ll need to check your credit score, compare different credit cards, and apply for one that fits your spending habits and creditworthiness.

We’ll discuss what to look for in a credit card, the advantages and disadvantages of a store card, and soFAQsFAQ. Let’s get started!

Compare Credit Cards

Compare the rates, fees, and rewards of leading credit cards.

Steps to get approved for store credit cards

Have you been denied a credit card in the past because of your credit? Or are you not sure if you should apply? If so, here are some tips to help you learn how to get approved for store credit cards. Following these steps will give you the best chance for approval.

Take a look at your credit score

The first thing you need to do is figure out where you stand with your credit score. If you’ve never had a credit card or loan in the past, you may not have a credit score yet. But it’s wise to check anyway.

Your credit score is like your all-time financial report card. The three major credit bureaus analyze your financial history and give you a score. It tells banks how responsible you are as a borrower and tells credit card issuers how likely you are to pay back the money they lend you. In other words, your credit score represents your ability to make payments on time and pay back your credit card balance on time each month. The higher your score, the more likely you are to get approved for credit.

Where can I find my credit score?

Here are a few places where you can get access to your credit score, either for a small fee or for free.

Click here for a comprehensive list of the best credit monitoring tools.

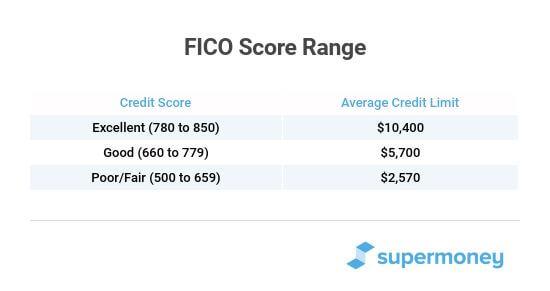

Here are the different ranges for a FICO credit score to give you an idea of what to expect.

What is the minimum credit score for approval?

If your credit score is fair or better, you should have a good chance of getting approved. If you have a low credit score, you should still have a chance. Store credit cards are known for having lower approval requirements than rewards credit cards offered through most banks. So, if you have been rejected for a bank credit card in the past, you might be in luck with a store credit card.

Pay down outstanding debt

Improving your credit score can take time. It may help if you throw some extra cash at your debt. The higher your income and the less debt you have, the better you look to the people issuing credit cards.

What debt should I pay down first?

Start with your credit card debt. Next, focus on other consumer debt like auto loans, student loans, and personal loans. Banks are a little more understanding if you have mortgage debt, so that shouldn’t be a deal-breaker.

As you pay down debt and lower your debt-to-income ratio — your monthly debt payments divided by your monthly gross income — you’ll have a better chance of getting approved for credit cards. This will also increase your credit score.

Maximize your income

While it’s not a good idea to lie about your income on your credit card application — it’s actually considered credit card fraud — it’s important to know what counts as income and what doesn’t so you can provide accurate information.

Here’s a quick summary of things to consider based on your age:

Ages 18 – 20

- Personal income

- Regular allowances

- Scholarships and grants

Ages 21 and up

- Personal income

- Regular allowances

- Scholarships and grants

- Income from a spouse or partner

- Trust fund distributions

- Retirement fund distributions

- Social Security income

Note that debt such as student or personal loans doesn’t count as income. But if you’re a student with no earned income or a stay-at-home parent, you still have options.

Decide on an open-loop or closed-loop credit card

You’ll need to decide whether you want to apply for an open-loop or closed-loop card. This is an important distinction to make because it affects how and where you can use the card.

Open-loop cards can be used anywhere

Open-loop cards function much like traditional rewards credit cards. You can use open-loop cards at the retail store that issued them and anywhere credit cards are accepted. For example, if your card is issued by American Express and it’s an open-loop store card, you can use it anywhere that accepts American Express.

Closed-loop cards can only be used at one retail store

Closed-loop cards are different. You can only use this type of store card at the store that issued it to you. If you use these credit cards anywhere else, the card will either get denied, or you will get hit with an additional fee, depending on the terms and conditions.

When applying for a store credit card, be sure to read the terms and conditions carefully to determine whether the card is open-loop or closed-loop. Make sure the card you are applying for aligns with your spending needs and expectations.

Visit a store or apply online

Once you have completed all of the steps above, you should be ready to decide which store’s credit card to apply for. There are a few key factors you’ll want to consider as you make that choice.

Choose a store where you shop frequently

The first thing you’ll want to consider is where you shop most and where you tend to spend the most money. Just about every store offers some kind of credit card, but it wouldn’t make much sense to open a department store card if you only shop there every few months.

You’ll want to consider stores where you shop several times a month, for example, and spend money consistently. This will help ensure that you are not being taken advantage of or going out of your way to spend on the card to receive card rewards.

What type of store should I choose?

It doesn’t really matter what kind of store you choose as long as you shop there regularly and will put the rewards to good use. A good place to start might be your favorite clothing store, electronics store, or gas station. You can look back through previous purchase records or bank statements to see where most of your money is being spent. If a store shows up consistently, it may be worth applying for their store card.

Examine the card’s APR

Once you have chosen a few stores to compare, look at each card’s APR or annual percentage rate. This refers to the amount of interest you will pay on a month-to-month basis on any unpaid balance on the card.

Of course, if you pay your balance in full and on time every month, you’ll never have to worry about paying high interest rates. However, most people do end up paying interest on their credit cards at one time or another throughout their lives. You’ll want to be sure that the card you are using has a reasonable APR before applying.

Evaluate the card’s rewards program

In addition to reading about the card’s APR, take a look at the card’s rewards program. Some rewards programs are much more lucrative than others. They may offer incentives such as cashback rewards, major discounts on in-store purchases, or exclusive product releases depending on the number of purchases made on the card.

Unfortunately, not all rewards card programs are worth it. Some offer relatively unimpressive rewards. Be sure to stop and really consider whether these rewards and perks are something you will use on a regular basis and actually benefit from when you redeem them. It is easy to read about a bonus, perk or rewards and think you will use them, but find it ends up being meaningless to you in practice.

These rewards programs change from time to time, so for the most accurate information on a card’s rewards program, check their website and card details.

Find out if the card has an annual fee

Some store credit cards come with an annual fee. You can think of this as a cover charge. As the name suggests, the cardholder must pay this fee yearly regardless of how much they spend on the card. Think of it as a fee that pays for the privilege of having the card at all. Some retailers will call their annual fee something like a “membership fee” or a “membership charge.” These terms are mostly interchangeable and essentially the same as an annual fee.

How much does the typical annual fee cost?

The most common annual fee on store credit cards is $95. In some cases, though, the annual fee on a store card can be $195, or even up to $500. Cards with a high annual fee like this are generally not very easy to get and are reserved for customers with the highest credit scores.

Consider all possible credit card offers

If you have a good credit score or better, you may have many possible credit cards to choose from. There is no need to rush into something you don’t actually want. After all, this is the card you may be using for the majority of your purchases for the foreseeable future. Take your time in deciding which credit card offers are right for you.

You can easily access credit card information on a store’s website by calling the customer service department or by visiting the retail store in person.

Store credit cards vs. traditional rewards credit cards

Store credit cards tend to have looser credit requirements than most rewards credit cards. While a traditional credit card requires a credit score of 680 to get approved, store cards typically have a much lower threshold.

Why is there a difference between store credit cards and rewards credit cards?

The main reason for that is because retailers benefit from people signing up for their cards. Having a store card encourages people to purchase items more often to earn rewards and discounts. Some stores have been known to offer their shoppers extra discounts of over 20% or more if they use a store card. This encourages people to spend more money at that store over the long term.

Generally, customers can also accumulate points at the store by using the store credit card, and those points can be redeemed for even more rewards. Again, all of this is to encourage spending in the store and on the store credit card. The more you spend, the more rewards you earn, and the more discounts you are offered. When you spend more, the store brings in more profits and revenue.

Store cards help pad the bottom line

This is all done to help the retailer’s bottom line. All of those purchases at the store on the store credit card add up over time. If you also end up paying interest on your card, even better for them. The store also collects revenue on those interest payments.

All of this is to say that the more retail cards a store signs people up for, the more it will help their revenue and profits in the end. So they have little reason to deny anyone who wishes to sign up for one of their credit cards. Because of all of this, card issuers are willing to extend credit card offers even to customers with bad credit.

Other essential questions related to store credit cards

To help you determine whether a store card is right for you, here’s a quick FAQ with some top relevant questions:

Do store cards hurt your credit?

Every time you apply for a credit card, the card issuer runs a hard inquiry on your credit report. The major credit bureaus let the card issuer know how trustworthy you are, but this information comes at a cost to you. Each hard inquiry — every time you apply — can knock a few points off your credit score. However, although your credit score may go down a few points, as long as you don’t apply for multiple cards in a short period, the negative impact is negligible.

Other factors, such as making late payments and maxing out your credit limit, will have a far greater negative impact on your credit score. So don’t worry too much about losing a couple of points over applying for new credit cards. Your credit score will start to rise once you begin to use the card and pay it off on time consistently.

Can store credit cards help you build credit?

If the card’s issuer reports your activity to all three credit bureaus, your positive account activity can help you establish a good credit history and improve your score over time. The progress will be slow but steady, so don’t expect anything drastic to happen quickly. This isn’t a “quick fix,” and there isn’t a way to “game the system.” Just be sure to use the card responsibly by avoiding the temptation to purchase something you don’t and make your payments on time each month. This will help you build your credit score over time.

Can you get a credit card with a 550 credit score?

It’s definitely possible to get a store card with a 550 credit score. As we mentioned earlier, someone with bad credit may still qualify for a rewards card because stores are very willing to give them out. Whereas someone with a low credit score around 550 might get denied a bank credit card, they would be much more likely to get accepted for a credit card. If you have any questions on what credit scores are required for a specific credit card, we recommend contacting the card’s customer service department.

Are there any instant-approval department store credit cards?

There are, in the sense that it typically takes less than a minute to get an approval. But most credit card issuers will run a credit check before approving your application.

What happens if I am not approved for a store credit card?

If you are not approved for a store credit card, you still have a few options. You can apply for other credit cards and keep trying elsewhere until you get accepted.

Additionally, you can try to decrease your credit utilization and pay down some debt, as mentioned earlier. This can help you build credit and make you more likely to be accepted in the future. If you choose this path, be patient. It can take a long time to build credit.

Are there any drawbacks to a store credit card?

As with any credit card, there are risks to be aware of when applying for and using a store credit card. These include:

- High APR

- The temptation to spend more money

- Lower rewards than other credit cards

- The annual fee for membership

Before applying for a new store credit card, we recommend you take the time to research and familiarize yourself with the risks of using a retail credit card.

Applying for a store credit card

Now that you know how to get approved for store credit cards, it’s time to decide if you should get one or not. Store credit cards may be a big step forward in your personal finance journey. If your credit score needs some help and you often shop at a specific retailer, it can be a good idea to get a credit card from that retailer.

However, if you’re concerned about overspending, or you’ve had trouble with overspending on credit cards in the past, a store credit card could make it worse. You don’t want to encourage yourself to make one unnecessary purchase after another.

If you decide that a store credit card is right for you to use, check out the ones we’ve listed and other top options before you apply.

It’s also a good idea to compare other types of credit cards as well to make sure you’re not missing anything. The more you know, the more confident you’ll be in choosing the right credit card for you so you can start to build credit over time.

Ben Luthi is a personal finance writer and a credit cards expert who loves helping consumers and business owners make better financial decisions. His work has been featured in Time, MarketWatch, Yahoo! Finance, U.S. News & World Report, CNBC, Success Magazine, USA Today, The Huffington Post and many more.

Share this post:

AddTable of Contents