Crypto’s Coming of Age: IRS Secures First Tax Evasion Conviction

Last updated 12/11/2024 by

SuperMoney TeamEdited by

Andrew LathamSummary:

Cryptocurrency’s coming-of-age moment has arrived, with the IRS securing its first guilty plea for crypto tax evasion.

Once considered a fringe financial experiment, cryptocurrency is now firmly in the spotlight—this time under the watchful eye of the IRS. The agency’s first successful prosecution for cryptocurrency tax evasion and a record-breaking settlement with Binance sends a clear message: the IRS is watching. As the industry matures, it faces growing pains that other sectors, like e-commerce and gig work, have experienced during their evolution.

End Your IRS Tax Problems

Get a free consultation from a leading tax expert.

It's quick, easy and will not cost you anything.

IRS makes history with first crypto tax evasion conviction

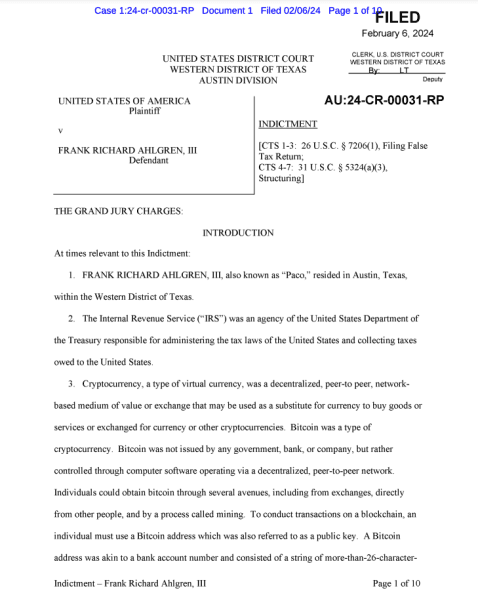

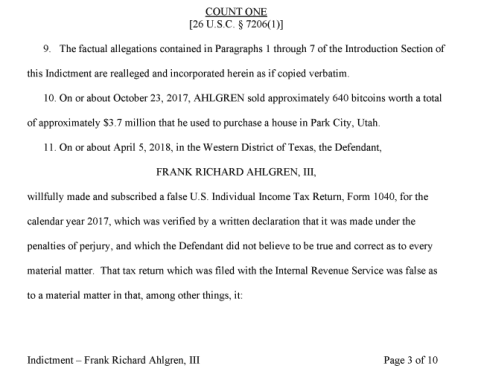

Frank Richard Ahlgren III, an early Bitcoin investor from Austin, Texas, became the first individual to plead guilty to crypto tax evasion—a milestone in the IRS’s efforts to regulate the digital asset world. Ahlgren admitted to underreporting significant capital gains from the sale of Bitcoin between 2017 and 2019, causing a tax loss of more than $550,000. His conviction highlights the IRS’s readiness to pursue cases involving digital assets aggressively.

According to court documents, Ahlgren purchased approximately 1,366 bitcoins in 2015, when the cryptocurrency was valued at no more than $500 each.

In 2017, as Bitcoin’s value surged, Ahlgren sold 640 bitcoins for approximately $5,807.53 each, netting $3.7 million. Rather than accurately reporting these transactions, Ahlgren filed a false tax return for 2017, inflating the cost basis of his bitcoins to reduce his reported gains. He used the proceeds to purchase a luxury home in Park City, Utah.

In addition to the 2017 misreporting, Ahlgren sold over $650,000 worth of bitcoins in 2018 and 2019 but failed to report those transactions altogether. These deliberate omissions violated federal tax law, which requires taxpayers to report any sale proceeds and gains or losses from the sale of cryptocurrency on their tax returns.

— Did you know? The IRS reported identifying $4.2 billion in tax fraud in 2023, with cryptocurrency accounting for a growing share of these cases. —

The IRS Criminal Investigation Division’s work on this case demonstrates its commitment to addressing cryptocurrency-related tax fraud. With a conviction rate exceeding 90%, the agency uses advanced blockchain analytics and global data-sharing partnerships to trace unreported crypto transactions. Ahlgren’s conviction is expected to serve as a deterrent, encouraging more voluntary compliance from cryptocurrency investors who face an increasing risk of detection.

Ahlgren’s sentencing is pending, and he faces up to three years in prison, supervised release, restitution, and monetary penalties. This case sets a clear precedent that tax evasion involving digital assets will not be overlooked as the IRS ramps up its enforcement efforts.

How does the IRS use blockchain analytics to track crypto?

The IRS employs blockchain analytics to uncover cryptocurrency transactions and ensure tax compliance. Blockchain analytics tools, developed by companies like Chainalysis and CipherTrace, analyze blockchain data to trace transactions and link them to real-world identities. Here’s how these tools work:

- Transaction tracking: Blockchain analytics map the flow of funds by analyzing transaction histories. This helps trace the origins and destinations of cryptocurrency, even across multiple wallets.

- Wallet clustering: These tools group wallets based on shared characteristics, such as recurring transaction patterns, to identify connections between wallets potentially controlled by the same individual or entity.

- KYC data integration: Many exchanges require Know-Your-Customer (KYC) verification, linking user data to specific wallet addresses. The IRS uses this data to connect wallets to individuals.

- Cross-chain analysis: By examining activity across multiple blockchains, analytics tools can track funds that users attempt to obscure by transferring them between networks.

These advanced tools give the IRS a powerful edge in detecting unreported crypto transactions, making anonymity in cryptocurrency increasingly difficult to maintain. For investors, compliance with tax laws is essential to avoid penalties or legal consequences.

Why crypto is under the IRS microscope

Like other industries that started as disruptive forces, cryptocurrency is now seeing increased scrutiny as it integrates into mainstream finance. In its 2024 annual report, the IRS highlighted the growing use of cryptocurrencies for both legitimate and illicit purposes, including tax evasion, money laundering, and fraud. The report noted that the agency has tripled its enforcement efforts related to digital assets in the past year, with plans to expand its capabilities globally.

Why it’s better to file crypto gains and not pay than to not file

Filing your crypto gains, even if you can’t pay the taxes owed, is crucial for minimizing consequences. The penalty for failing to file is significantly higher—up to 5% of your unpaid taxes per month—compared to the 0.5% monthly penalty for failing to pay. Filing on time also helps you avoid legal trouble, as not filing can be seen as tax evasion, a criminal offense.

Additionally, filing makes you eligible for IRS payment plans or offers in compromise, allowing you to settle your tax debt over time. Skipping the filing step can escalate the situation and lead to harsher penalties or audits. Always prioritize filing, even if full payment isn’t immediately possible.

Binance settlement sets the tone

The IRS isn’t just focusing on individuals. Binance’s $4 billion settlement for anti-money laundering violations represents a turning point. In the settlement, the exchange and its CEO, Changpeng Zhao, admitted to knowingly facilitating illicit transactions. This resolution not only sets a precedent for enforcement but also puts crypto companies on notice that the stakes have never been higher.

What’s ahead: Billy Long and the Crypto Crackdown

With the appointment of Billy Long as IRS commissioner under the Trump administration, the crypto world could face an even stricter regulatory environment. Long’s track record suggests he is unafraid to implement sweeping changes, including new guidelines for digital asset reporting. While this may streamline compliance, it could also create challenges for crypto enthusiasts who are unprepared for the level of scrutiny ahead.

Key takeaways

- The IRS has secured its first guilty plea for cryptocurrency tax evasion, marking a milestone in enforcement.

- Binance agreed to a record $4 billion settlement for anti-money laundering violations, setting a new enforcement benchmark.

- Billy Long’s appointment as IRS commissioner signals a potential crackdown on crypto under the Trump administration.

Share this post:

Table of Contents