IRS Schedule F Tax Form (1040) Profit or Loss From Farming Business

Summary:

As a self-employed person and sole proprietor, you probably know that you need to fill out a special form to report your business income and claim deductions for business expenses. If your business is among those the Internal Revenue Service (IRS) considers farms for tax purposes — such as ranches, plantations, fish hatcheries, and actual farms — the form you need to file, along with your Form 1040, is Schedule F.

So you’ve left the rat race to become a farmer. Simple country living, early to bed and early to rise, and hard but rewarding work. You harvest your own vegetables, butcher your mean, and maybe even make your own soap. And, best of all, there’s no cumbersome paperwork to file with the government!

Uh, not quite. As a farmer — which for tax purposes includes anyone who grows crops or raises livestock as a business — you have to file complex tax paperwork like every other businessperson. If you are a sole proprietor rather than partnership or corporation, this means completing IRS Schedule F: Profit or Loss From Farming Business along with your 1040 tax form.

This article will tell you what you need to know about Schedule F, including when you should use it and what information you need to include when filling it out. It will also direct you to resources, such as tax preparation firms and tools that can make your tax life easier, along the way.

Pro tip — Are you a sole proprietor but not a farmer? In that case, what you’ll need is Schedule C: Profit or Loss From Business. Learn more about this and related matters in these two SuperMoney articles: How to File Self-Employment Taxes Step by Step and How to Avoid a Business Tax Audit.

Compare Tax Preparation Services

Compare multiple vetted providers. Discover your best option.

Federal employees aren’t singling you out

Before you start pulling your hair out because the tax man is disrupting your simple, bucolic lifestyle, realize that the demands of tax compliance disrupt pretty much everyone’s life in modern America.

In 2019, the Bipartisan Policy Center issued a paper entitled Tax Administration: Compliance, Complexity, and Capacity. As the authors of that paper observed,

The cost and time associated with filing returns constitutes a growing burden on taxpayers and on the economy, separate from and independent of the magnitude of the tax payments themselves.”

Or, as the Tax Foundation words its introduction to featured research on the topic,

The full cost of a tax system….includes the cost of tax planning and paperwork….and the IRS estimates Americans spend 6.6 billion hours per year filling out tax forms — including 1.6 billion hours on the 1040 form alone.”

No one who has filed a tax return is likely to disagree with either of these quotations. Though SuperMoney can’t change the tax system for you, it hopes to make the system easier for you to navigate. This article on Schedule F is just one among many SuperMoney articles explaining tax forms and related tax-compliance issues. Here are some examples:

- What Is An 8862 Tax Form?

- Filling out a 1099 Form: Avoid These Common Pitfalls

- IRS Form 1099-C: How to Avoid Taxes on Forgiven or Canceled Debt

When should you use Schedule F?

If you earn an income from farming as a self-employed sole proprietor, you will need to file Schedule F. For tax purposes, “farming” includes a lot more than owning and operating a traditional farm.

Business activities that do and don’t count as farming

If there is a way for you to earn money by growing plants, raising animals, or maintaining land that you own with its flora and fauna, chances are good that it will count as farming for tax purposes. However, not every job that deals with plants, animals, or land counts as farming.

A farming business has to make money

As already noted, you are only a farmer for tax purposes if you engage in your counts-as-farming activity as a for-profit business. To qualify as a for-profit business, your “farm” needs to have brought in revenue in no fewer than three of the last five years. If you breed, train, and show racehorses, you only need to show a profit in at least two years of the last seven.

As with all things bureaucratic, of course, the rules are far from that simple. If it hasn’t brought in money in three of the last five years, your farm might still count as a business.

How to qualify as a business despite insufficient profitability

Here’s what you must do for your farm to have a chance to qualify as a business in spite of not meeting the requirement:

- Run the farm like a business

- Make changes to how you run the farm to make it more profitable

- Have, or have advisors who have, the knowledge needed to profit from farming

- Have profited from similar activities before this new venture

- Profit from farming in some years, even if not the required three out of five

- Reasonably expect to garner future profit from the increased value of the assets you use for farming, such as the land and structures

- Be suffering losses due to normal startup-phase issues or causes beyond your control, such as drought.

- Depend on the farm as your primary source of income

- Put a lot of your time and effort into farming

If you do all this, the IRS may decide to recognize your claim to be a business. That the agency will agree with you is not guaranteed.

Professional tip — Sole proprietors who need to amend the tax return for a previous year may need to find a prior year’s Schedule F to report their profits, losses, and expenses properly. If that’s your situation, you can find all the prior-year Schedule Fs you need here on the IRS website.

Farming business good, farming hobby not so good

Why does this matter? As a farming business, you can deduct farming expenses and, when business goes badly, report a loss. This can reduce your tax liability. Prior to the 2018 Tax Cut and Jobs Act, some expenses for not-for-profit “hobby” farms and ranches could be deducted, but that is no longer the case. The only way to deduct these expenses now is to have your farm or ranch qualify as a business.

If you operate a farm for profit, you can deduct all the ordinary and necessary expenses of carrying on the business…on Schedule F. However, if you don’t carry on your…activity…to make a profit, you report the income from the activity on Schedule 1…, line 8i. You can no longer deduct expenses of carrying on the activity, even if you itemize your deductions on Schedule A….Activities you do as a hobby, or mainly for sport or recreation [cannot] be deducted.” — IRS Farmer’s Tax Guide, 2021 tax year

Using Schedule F when married

Married couples who own and operate farms together will not always qualify to use Schedule F. To use Schedule F, you and your spouse must do one of two things, or sets of things:

- Own the farm as community property, in which case your farm can be treated as a sole proprietorship when doing your taxes. In this case, you will only have to file one Schedule F. Availability of this option will depend on the laws in your state. Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin have community property laws that may make this a viable option for you if you live in one of these states. State laws, of course, do change, so consult with a tax or legal professional in your state if your status remains unclear after you do your own research. See IRS Publication 555: Community Property for more information.

- Be the sole owners of a farm that you operate jointly, file a joint tax return, and choose to have your business treated as a “qualified joint venture” when doing so. In this case, you and your spouse will each have to file a Schedule F along with your joint return.

What if neither of these methods works for you? In that case, the IRS will consider your farm a partnership and require you to file Form 1065: U.S. Return of Partnership Income.

Schedule F is not for special legal entities

Even if your business qualifies as a farm in the eyes of the IRS, there are cases where you won’t use Schedule F. As you just learned, one such case is when you’re married and fail to meet certain standards. Failing to meet those standards makes your business a partnership rather than sole proprietorship.

The other case is when you set up your business as one of the legal entities allowed by law, such as a corporation or limited liability company (LLC). People often decide to set their businesses up as such legal entities to take advantage of liability protections and tax benefits. If you’ve done this with your farm, you cannot use Schedule F. Instead, you’ll have to use Form 1120: U.S. Corporation Income Tax Return.

Seem too complex?

If any of this seems too complex to you, or just too much hassle to deal with, you should consider consulting a tax professional or purchasing a tax-filing tool designed in consultation with such professionals. To help you choose wisely from the available options, SuperMoney has prepared objective profiles of many of these resources and brought together numerous reviews by real-life customers.

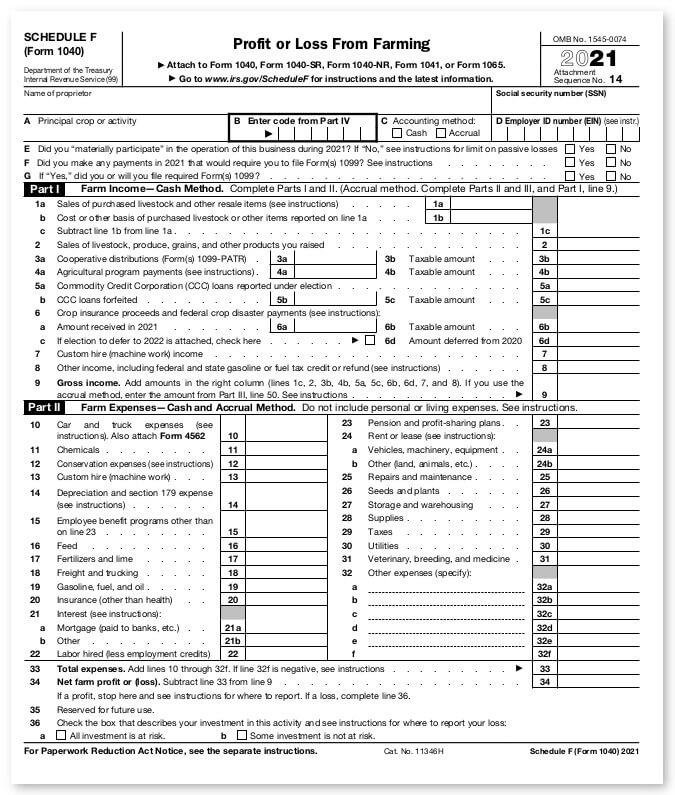

How to use Schedule F

Schedule F allows sole proprietor farmers to report the taxable income they earn from their farming or farming-for-tax-purposes activities. It also allows them to claim credits and deductions related to those activities.

Report farm income

To complete Schedule F correctly, you will need to provide all of the following information:

Key information needed for Schedule F

- Main activity, crop, or product of your business

- Income earned from sales of whatever you sell, whether it be fruits, vegetables, grains, legumes, beef, pork, thoroughbred horses, or something else

- Income received from other sources, such as Commodity Credit Corporation loans, agriculture program payments, crop insurance, federal crop disaster payments, and distributions from a cooperative

Depending on whether you use the cash or accrual method to track your business finances, how you complete the appropriate Schedule F entries will differ. As a farmer, you also have — with IRS approval — a third way you can report income: the crop method.

How to report farming income (and expenses)

As a farming business, you can use one of three business accounting methods. Which you use will determine how you report your income and expenses.

- Cash method: report income in the year you receive it and expenses in the year you pay them. This is the easiest method to keep track of and the go-to default of most sole proprietors, including farmers.

- Accrual method: report income in the year you earn it and expenses in the year you incur them.

- Crop method: report income in the year you sell what you grow and expenses when you sell the crop the expenses paid to produce. You must get IRS permission to use this method.

Reduce taxable income by claiming deductions

To complete Schedule F correctly, you’ll also need to report any deductions you are eligible for and wish to claim. The farming-related deductions you can claim on Schedule F are too numerous and variable to list exhaustively here. As a rule of thumb, the best thing to do is check the eligibility of any expense you think should be deductible and see if it actually is deductible during for that tax year.

Key farming business deductions

Just to get you started, here are some deductions you may be able to claim:

- Business expenses such as employee benefits, employee pensions, hired laborers, loan interest, profit-sharing programs, and taxes

- Facilities and freight expenses like insurance costs, purchase or lease of land, shipping or freight charges, storage or warehouse costs, and utilities

- Farming supply expenses such as the cost of chemicals, such as herbicides and pesticides, of fertilizer, and of plants and seeds

- Livestock expenses like the cost of new livestock, feed for the livestock you already have, and veterinary services

- Vehicles and equipment expenses, including depreciation of purchased vehicles and equipment, fuels such as gasoline, purchase or lease of business vehicles and farm equipment, including tools and machinery, and repair and maintenance costs

Take income types into account

As you might have guessed, plain income is too simple and straightforward a category to work for our federal tax authority. You’ll need to think with greater complexity to navigate your farming business taxes.

Income types for farming taxes

To complete your Schedule F without making mistakes, or possible to qualify to use it in the first place, you’ll need to think in terms of four categories of income, two forms of cash income and two forms of farm income:

- Two categories of cash income:

- Gross cash income is the total of any direct government payments you receive (such as for subsidies) and all the money you get from sale of whatever you sell, be it goods such as livestock or crops, or services such as allowing ranchers to graze their cattle on grasslands you own and maintain.

- Net cash income is gross cash income minus cash expenses. These expenses include feed for livestock, fertilizer and seeds for planting, rent or lease payments to landlords who are not themselves involved in the farming, and tax and labor costs.

- Two categories of farm income:

- Gross farm income is gross cash income plus income received as something other than currency. An example is the value of food produced by the farm that you consume yourself.

- Net farm income is the gross farm income minus cash expenses and expenses that don’t directly involve currency. Examples include the household expenses of living on a farm and property depreciation.

The income types serve separate purposes. In the words of the Congressional Research Service,

Net farm income is a longer term measure of the ability of the farm to survive as a viable income-earning business, while net cash income is a shorter term measure of cash flow.”

Given that it indicates longer-term viability of a farming business, knowing your net farm income could prove important if you need to persuade Internal Revenue operatives that your farm should qualify as a business, not a hobby.

Pay attention to your payments to third parties

Got independent contractors? If so, you may need to file Form 1099 for some of them. Whether you need to file this form or not depends on how much money you had to pay each contractor. As of this writing, the amount is $600, but like all hard dollar amounts in tax law, this one could change. If you paid more than the limit to any contractor during the tax year, you’ll need to file the appropriate Form 1099 for that contractor.

Fun fact — Though this writer can’t imagine why, the Charles Bronson classic Mr. Majestyk omitted any mention of this topic. If you want to know more about Form 1099 and how to avoid common pitfalls when filing one, you’ll just have to read the SuperMoney article recommended earlier.

Use additional forms when necessary

Schedule F covers a lot, but it doesn’t cover everything. For instance, if you sell some of your farm assets, you may need to use Form 4797: Sale of Business Property. This form lets you report your capital gain or loss from such sales.

Don’t forget your estimated tax payments

As a self-employed farming sole proprietor, you share other self-employed people’s obligation to make estimated tax payments if you expect to owe enough in taxes — but with a twist. Instead of having to make an estimated payment every quarter to avoid penalties, you may only have to make one. And, if you can reliably pay your taxes early every year, you can skip the estimated payment altogether.

Here are the specifics. If you receive more than two-thirds of your total income from farming, and if you are a calendar-year taxpayer, you can make a single estimated tax payment on or before January 18thof the following year. So, for example, you could have gone through the entire year of 2021 without making any estimated payments and, so long as you did some preliminary calculations and sent in an estimated payment by January 18th of 2022, you would not have incurred any penalties. Even better, if you miss the January 18 deadline, you can still avoid penalties by preparing and paying your taxes on or before March 1st.

There’s no guarantee that these dates will never be tweaked. A lot of deadlines changed during the, well, interesting 2019–2021 time period, as you might recall. You should always verify current dates from the most recent documents the IRS has posted.

Take advantages of helpful resources

Consulting a qualified professional is seldom a bad idea when dealing with a complex tax issue. Making use of a good tax-preparation tool when doing your taxes will also rarely prove to have been a mistake.

“But both tax professional and tax-preparation tools are resources I’d have to pay for,” you say. “I prefer free resources.”

You are a reader after the writer’s own heart. And you are in luck. The same federal agency that is making you do all this work also provides two excellent resources that you can draw upon while preparing your income tax return as a farmer.

- Publication 225: Farmer’s Tax Guide. This is a comprehensive guide to the tax code affecting farmers. It’s version for the 2021 tax year is not far shy of 100 pages.

- Publication 51: (Circular A), Agricultural Employer’s Tax Guide. If you hire employees for your farming business, you’ll want to peruse this guide. Though its 2022 version is only 30 pages, these are 30 pages you won’t want to put off reading until tax time.

Key takeaways

- If you are a sole proprietor and your business counts as farming for tax purposes, you need to file Schedule F along with Form 1040.

- For tax purposes, most businesses that involve growing crops, raising animals, or maintaining land with its flora and fauna count as farming.

- If you breed fish or fine horses, even you may be a farmer for tax purposes.

- If you own a kennel, are a veterinarian, do landscaping, or own a winery that produces fine wines that people rave about (or detest), you are not a farmer for tax purposes.

- Depending on the setup and complexity of your businesses, you may have to file different or additional tax forms.

- Consulting a tax professional, or at least using a good tax-preparation tool, is an excellent idea in most cases. If your farming business is complex rather than simple, professional help may be essential.

David loves learning, doing research, analyzing data, and assessing arguments. Though he has two advanced degrees and some background in psychology, and though he's learned a great deal in his work with SuperMoney, he considers himself an interpreter of experts, not an expert himself. He enjoys using what he's learned, and what he's still learning, to help readers make better saving, spending, and investing decisions.

Share this post:

AddTable of Contents