Jars Money Management System 2.0 – How to Put Your Budget on Autopilot

Last updated 08/07/2024 by

Sponsored Content

Summary:

Using the jar budgeting method is a great way to reduce debt and increase your savings. However, it can be hard to follow if, like most people, you don’t use cash for all your purchases. Fintech companies, such as Douugh, make it easy to set up digital jare budgets.

Budgeting is hard. The hardest part about budgeting isn’t that you don’t know how to do it or you’re unsure if it’s the right thing for your life. It’s that once you start, it sucks all of the joy out of spending money on things you enjoy.

It doesn’t have to be that way. As T. Harv Eker explains in Secrets of the Millionaire Mind, “one of the biggest secrets to managing money is balance” and “the habit of managing your money is more important than the amount.”

How can you find balance and create good habits when managing money? Eker recommends taking the guesswork out of budgeting and using the jar budgeting system.

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

How does the jar system work?

You may also have heard of this method called the envelope budget system.

Before everyone used credit cards and digital wallets, and budgeting apps were not widely available, people would divvy up their money into actual jars or envelopes that were labeled to identify their purpose (e.g., rent, college-fund, fun, savings, etc.). The system requires you to immediately put a set amount of every paycheck in each jar.

There are several versions of the jar budgeting method, but this is how Eker’s version works.

1. Set up your jars (or accounts) and label them

Eker recommends using the following labels: Financial Freedom jar, play jar, long-term savings jar, education jar, necessities jar, and give jar.

2. Put 10% of your income into a Financial Freedom jar

Never spend this money. This money is exclusively for investing in passive income streams to fund your retirement. From now on, you are an angel investor, and this is your seed money account.

3. Set aside 10% in your play jar

This is money you are supposed to blow away every month without a second thought. Enjoy!

4. Place 10% in a long-term savings jar

This jar is designed to pay for large purchases, such as a new car, a vacation, college tuition for your kids, etc. If you have debts with high interest rates, use this jar to pay off your debt.

5. Invest 10% into your education jar

It can be a challenge to spend money on books, seminars, or coaching when you’re focusing on getting out of debt or trying to save for retirement. This jar permits you to invest a chunk of your income in creating the best possible version of yourself.

6. Put 55% into your necessities jar

This is the boring jar. Keeping your living expenses, such as housing, food, utilities, and transportation, to 50% of your income is the main challenge of this budget.

One of the most common questions people have with the jar budgeting method is, “what do I do if my living expenses are more than 55% of my income? Remember that the habit is more important than the amount! If you are not able to follow the recommended percentages perfectly, don’t worry. You may have to increase the percentage of your income you dedicate to living expenses at the beginning.

As long as you follow the system and make it a habit to manage your money following this method, you can succeed.

7. Give away 5% of your income

Choose charities or organizations that matter to you and donate to them every month. You will help make the world a slightly better place and benefit from the law of giving, which states that the more you give the more you get.

The problem with the jar budgeting method

If you consistently manage your money following this simple method, you can become financially independent on a modest income.

The problem is that although the jar budgeting method is simple, it requires a lot of effort to make it a habit. Using a jar system can also be impractical for people who use credit cards and digital wallets for most purchases.

The good news is that several financial technology companies, such as Douugh, Wealthfront, and Stash, can help you create a jar budgeting system and stick to it. These apps make jar budgeting, saving, and investing easy — even fun.

Jar budgeting method 2.0

Budgeting apps have taken the jar budgeting concept and made it work in a digital world. We will use Douugh as an example to illustrate how tech companies can simplify the process, but there are other ways to create a similar system.

Instead of wasting time and energy only using cash or transferring your paycheck to multiple accounts, let the AI of Douugh’s personal finance app do all the heavy lifting.

The first step is to set up your virtual Jars according to your circumstances. You can create as many Jars as your want, but here are the basic ones you should consider.

Bills Jar

The purpose of this jar is to make sure all your bills and subscriptions are paid every time. Set your bill on autopilot whenever possible and use an app to track your due dates and make sure you have enough to pay them. Practically all bills, such as your mortgage, student loans, utilities, subscriptions, and even rent, can be put on autopilot.

“Bills jar is created to easily manage all your fixed expenses. It helps you keep track of your upcoming and paid bills. So use this jar to keep track of all your bill payments,” says Alex Williams, a CFP and CFO of FindThisBest LLC.

Douugh sets aside money from each paycheck to cover your bills. You will get notified when a bill is due, and if there is enough to cover it, it will get paid. No more late fees and dings on your credit score due to missed payments.

“Bills Jars help you to spend smarter,” says Tom Fogarty, Digital Marketing Manager of Douugh.

“No longer do you bundle your savings, spending, and bills in the one place. The Bills Jar allows our members to set aside money in an account solely for their bills so they don’t accidentally dig into it. They go into each month knowing that their bills are covered, and there’s nothing to worry about. It’s also a great way of tracking all of your bills, to avoid those sneaky subscriptions that you no longer use but are still paying for,” explains Fogarty.

Spending Jar

Here is where the Jar illustration breaks down a bit. This Jar tracks everything you spend and sends alerts and reminders to make sure you don’t miss anything important. “Seeing where your money actually goes is the first and most important ongoing step in any budget,” says Nate Tsang, founder & CEO of WallStreetZen. “Spending tracking is critical in our age of subscription services, free trials that turn into subscriptions, and set-and-forget payments.”

With Douugh, you can filter spending by category and limit how much you allow yourself to spend on each one. Then, if you are close to your spending limit, you will get an alert that reminds you to rein in spending.

“Spending Tracker is my favorite tool because it helps me keep track of my monthly budget,” says Williams. “It discourages me from spending money impulsively, therefore, encouraging savings.”

Rainy Day Jar

The Rainy Day Jar is designed to hold your emergency fund. It’s a safety net that has your back when life throws you a curveball.

Douugh creates a default goal of $1,000 for this fund, but that may not be enough for many households.

Stash Jars

Stash Jars make it easy to save for short-term goals, such as going on vacation or buying a new phone. This Jar is separate from your main checking account, helping elevate friction by taking away the temptation to dig into your savings.

“Stash Jars enable faster saving,” explains Tom Fogarty. “Create as many Stash Jars as you want, for short-term goals like a weekend away or shopping. You can set a goal and visualize yourself edging closer to it each payday. Your money is stashed away safely, as there is no debit card linked to it so you won’t be tempted to dig into it.

Portfolio Jars

Consider stashing your savings in investment funds instead of putting your savings in accounts that pay less than 1% in interest.

Douugh allows you to create as many Portfolio Jars as you want and doesn’t charge brokerage or management fees. This feature alone will more than pay for Douugh’s $4.99 Financial Fitness Membership Fee.

You can choose between core and sustainable portfolios. Both core and sustainable options provide fully diversified funds and allow you to choose between conservative, moderate, and aggressive investment strategies. Sustainable portfolios avoid industries such as fossil fuels, tobacco, fur, military, and weapons manufacturing. Interestingly, Douugh’s sustainable portfolios have historically performed better than the core portfolios.

“Portfolio Jars are the smartest way to grow your money for long-term goals,” according to Tom Forgarty. He explains, “There’s no point having money sitting in a bank account earning a measly interest rate over a long term, which is why Portfolio Jars are so powerful. Like the other Jars, each payday, you can immediately invest your money – responsible money management. Our experts manage the diversified portfolios, so unlike other investing platforms, we leave the trading up to the experts.”

Set up payments and investments

Once you create all the Jars you need, put the stashing of them on autopilot. Every time your paycheck comes in your money should get split into your Jars according to your budget.

“With oversight, an automated budget saves you time. And since time is money, you’ll be able to gain more of it by focusing your productivity on profitable ventures, like a new side hustle or an investment strategy,” explains Tsang.

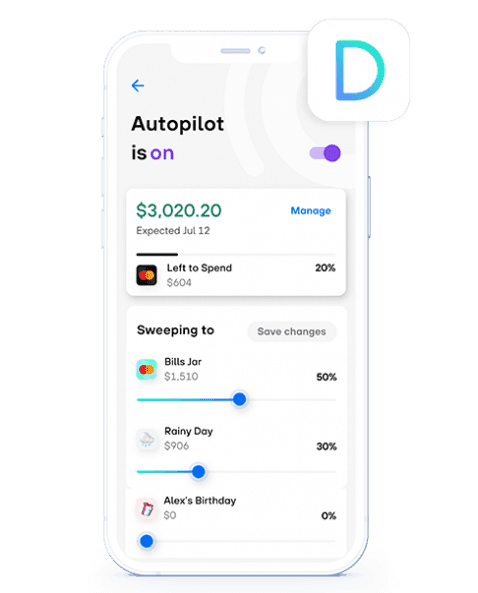

Douugh has a feature called Salary Sweeper that, when switched on, will transfer funds to your Bills, Stash Jars, and Portfolio Jars according to your budget. What is left remains in your Spending Jar (checking account).

Automating your budget provides multiple benefits besides saving you time. As Christopher Morgan, CEO of Credit Help Info, explains, “It eradicates the likelihood of human errors, forces you to be frugal, and saves you money because you avoid late fee fines and bounced check fees.”

Here are a few pointers to remember to help you prioritize your Jars.

Pay yourself first

Paying yourself first sounds like the easiest advice ever given. However, many households struggle to build savings and don’t have an investment strategy. So as soon as your paycheck hits your account, transfer a percentage of it to your rainy-day fund, retirement savings, and any Portfolio Jars.

Setting up recurring deposits to your Portfolio Jars at predetermined times is a strategy called dollar-cost averaging. This strategy will help you buy more shares when prices are low and fewer when prices rise. As a bonus, you will also avoid the temptation of timing the market, which is very hard to do unless you are an experienced and gifted investor.

Increase your savings over time

Budgets are not set in stone. Instead, they are meant to adapt to your financial situation. Smart budgets will assign more money to savings and investments as your income increases.

Personal finances can get complicated fast if you don’t have a budget. Remembering to follow and update a budget is extremely challenging for many of us. Putting your spending, bills, savings, and investments on autopilot can simplify things and increase your chances of financial success.

Key takeaways

- Budgeting is hard. Learning how to put your budget on autopilot with a smart bank account can help simplify things.

- The jar budgeting method can help you become attain financial freedom on a modest income.

- Don’t rely on willpower. Instead, create processes that promote smart financial decisions.

- Create a simple jar budget system. Plan how much money you will assign to each category.

- Set up payments and investments. Add friction to your budget and take the guesswork out of payments and investments.

- Pay yourself first by prioritizing your savings and investments accounts.

- Increase investments as your income grows.

- Although using actual cash and physical Jars is no longer practical for most people, it is easy to put into practice with the help of some financial technology wizardry.

These articles are brought to you by SuperMoney sponsors. Learn more about content sponsorship opportunities with SuperMoney.

Share this post:

Table of Contents