Lease Purchase Agreement: Things To Know

JA

Summary:

With a lease purchase agreement, you can rent and live in a property before making the final decision to purchase it outright. However, this arrangement is much less flexible than a lease option agreement and could result in serious financial consequences if you breach the contract. So before signing on the dotted line, make sure you understand what you’re getting yourself into.

Are you an aspiring homeowner considering signing a lease purchase agreement? Though this type of rental contract offers a viable path to homeownership for those who can’t afford the upfront costs associated with purchasing a home outright, there are potential pitfalls with entering into one of these arrangements.

In this article, we’ll go over everything you need to know about lease purchase agreements — such as their pros and cons — so you can make the most informed decision when it comes time to purchase your dream abode.

Compare Home Loans

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

What is a lease purchase agreement?

A lease purchase agreement is a rental contract between a landlord and a tenant that allows the latter to rent the property before purchasing it outright. It offers an alternative path to homeownership and can be great for those who can’t afford a full down payment right away.

To gain exclusive rights to purchase the property at a later date, the tenant typically needs to pay the landlord an option fee at an agreed-upon purchase price. Besides the option fee, tenants must also agree to apply a portion of their monthly rent toward the down payment.

How do lease purchase agreements work?

A lease purchase agreement offers buyers the chance to secure a property before having financing in place. The terms of the agreement typically stipulate an initial period of leasing followed by a final option to purchase the property.

During the lease, the buyer (tenant) pays rent that’s typically higher than the fair market price since the extra portion will go toward the down payment on the home. At the end of the lease period — typically one to three years — the tenant exercises their option to buy the house at the previously agreed-upon price.

This arrangement allows aspiring homeowners to gradually build their credit and save for the down payment and other fees associated with purchasing a home.

Pro Tip

Before signing a lease purchase agreement for your current apartment or buying another house, use this affordability calculator to determine how much house you can afford. Doing so will give you a realistic view of what type of home fits within your budget.

What’s included in a lease purchase agreement?

Lease purchase agreements typically consist of two contracts: the residential lease and the contract for sale.

1. Residential lease

The residential lease outlines the rights and responsibilities between the landlord and the tenant (the lessor and the lessee) — such as the length of the lease, payment structure, restrictions on pets or other behaviors, etc. It may also include a few extra clauses, such as requiring the tenant to pay for property taxes, maintenance costs, and insurance fees.

This portion of the agreement could also include info on the non-refundable option fee. This legally binds the landlord to sell the property to the buyer at the end of the lease.

2. Contract for sale

This portion of the lease agreement outlines the purchase process once the lease ends, and typically covers the following:

- Parties involved in the sale of the property

- The property selling price

- Down payment requirements

- Payment methods

Difference between lease option and lease purchase

Though lease option agreements and lease purchase agreements may sound alike, they’re not. A lease option agreement gives you the option — not the obligation — to buy the home when the lease ends. If you change your mind and decide not to purchase the house, you won’t suffer any financial consequences.

On the other hand, a lease purchase agreement is binding and much less flexible. If you don’t purchase the property after the lease period, besides forfeiting the option fee, you also won’t get the down payment back. Not to mention, the seller could sue you for breaching the contract.

Pros and cons of a lease purchase agreement

Lease purchase agreements come with certain pros and cons for both the sellers and the buyers. So before you enter into any lease purchase agreement, make sure you fully understand your responsibilities within the contract.

For sellers

Lease purchase agreements can be great for sellers in certain situations. For instance, if a seller is in pre-foreclosure on a certain property or is struggling to sell, a lease purchase agreement can offer a temporary or permanent solution. That said, these agreements aren’t without their risks.

For buyers

Though lease purchase agreements offer an alternative way for buyers to own a home, there are downsides to signing this type of rental agreement. Let’s explore the pros and cons.

If time is almost up on your lease purchase agreement, or if you’re looking to buy a different property, you’ll need to get the right mortgage to finance your purchase. Using the comparison tool below, you can make sure you receive the best terms possible.

Is lease purchase a good idea?

Yes, a lease purchase could be a good idea for landlords and tenants alike. Despite some potential downsides, Dustin Singer — real estate agent and owner of DunstinBuyHouses — says, “a lease purchase contract offers stability and security for both parties, clearly outlining the path to eventual homeownership. So, whether you’re a landlord or a tenant, this type of agreement is definitely worth considering.”

For landlords (sellers), a lease purchase agreement can be highly attractive during a competitive housing market since it allows them to lock in a buyer and secure monthly payments. And even if the buyer defaults, the seller could still get to keep the option fee and downpayment since they’re non-refundable.

For tenants (buyers), a lease purchase agreement allows them to “test drive” the home before making a long-term commitment. Plus, if housing prices are likely to increase in the near future, buyers may get a good deal by agreeing to a home sale price in advance and signing a lease purchase agreement.

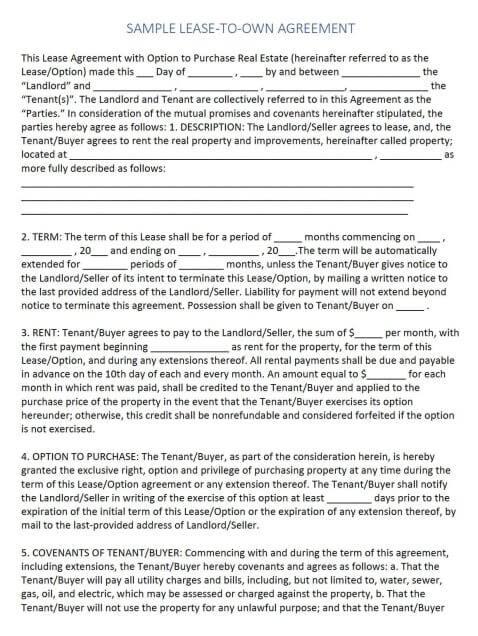

Step-by-step guide to a sample lease-to-purchase agreement

Here is a sample list of contents for a lease-to-purchase agreement and a brief summary of what you are likely to find in that section. Don’t use this to set up an actual lease-purchase agreement. You will want to get the opinion of lawyers and other real estate professionals before entering into a lease-to-purchase agreement.

- Description of the Property: The document describes the real property and improvements to be leased.

- Term: The term of the lease shall be for a specified period of time with an automatic extension unless the Tenant gives notice to the Landlord.

- Rent: The Tenant shall pay rent to the Landlord on a monthly basis, with a portion of the rent being credited towards the

- purchase price.

- Option to Purchase: The Tenant is granted an exclusive

right to purchase the property during the lease or any extension thereof.

right to purchase the property during the lease or any extension thereof. - Covenants of Tenant/Buyer: The Tenant/Buyer agrees to pay all utility charges and bills, not to use the property for any unlawful purpose and to surrender the property in as good condition as it was at the beginning of the lease.

- Covenants of Landlord/Seller: The Landlord/Seller agrees to pay for and maintain fire and extended coverage insurance on the property and to allow the Tenant to use the property without any interference.

- Breach by Tenant/Buyer: In case the Tenant fails to keep and perform any of the covenants or abandons the property, the Landlord/Seller has the right to repossess the property and terminate the agreement.

- Costs of Improvements: If the Tenant exercises the option to purchase and the Landlord fails to convey the property, the Tenant will be reimbursed for the cost of all repairs, maintenance, and improvements.

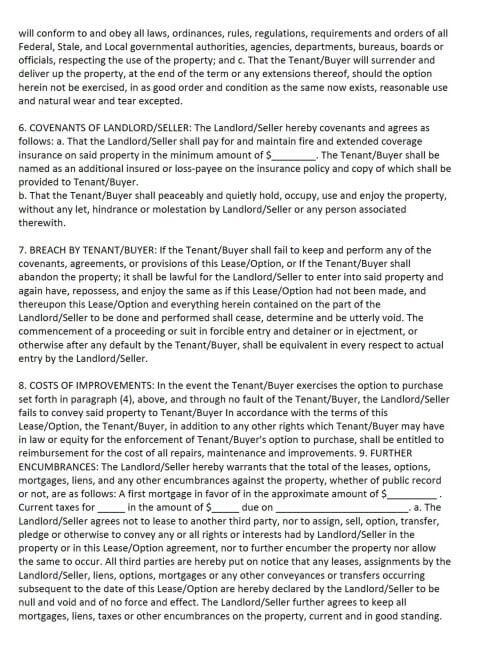

- Further Encumbrances: The Landlord agrees not to lease or assign to another third party, sell, transfer or further encumber the property during the term of the lease.

- Right of Assignment: The Tenant has the right to sublet the property, and/or to assign, sell, transfer, pledge or otherwise convey any or all rights or interests which the Tenant may have in the property or in this Lease/Option Agreement.

- Maintenance and Repairs: The Tenant is responsible for all maintenance and repair on the property, except for any repairs exceeding a certain amount or at the commencement of the lease or within a specified period.

- Binding Agreements: The parties agree that this Lease/Option comprises the entire agreement of the parties and that no other representation or agreements have been made or relied upon.

- Special Provisions: The document includes some special provisions that need to be fulfilled by the Landlord before the Lease/Option becomes valid.

- Price and Terms: The Tenant agrees to pay for the property the sum of money specified in the document.

- Included in the Purchase: The property shall include all land, improvements, and other items specified in the document.

- Title: The Landlord shall convey marketable title to the property with the inclusions specified in the document.

- Closing: The deed shall be delivered and the purchase money shall be paid at the lending institution of Tenant’s choice.

- Costs and Prorations: The prorated items shall be split between the Landlord and Tenant.

- Insurance: The Landlord shall maintain fire and extended coverage insurance until the Tenant buys the property.

- Attorney’s Fees: The prevailing party shall be entitled to recover court costs and attorney fees in case this agreement is placed in the hands of an attorney for enforcement.

- Required Disclosures: Federal Law requires landlords to give tenants a copy of an EPA-approved pamphlet onidentifying and controlling lead-based paint dangers.

- Additional Disclosures: The document includes any additional disclosures required by law or agreed upon by the parties.

FAQs

What is the downside to a lease-to-own contract?

For buyers, the main downside of a rent-to-own agreement is the risk of losing their down payment and upfront fee if they don’t purchase the property at the end of the lease. If they’ve lived at the property for a few years already, this could translate to thousands of dollars in losses.

For sellers, lease purchase agreements don’t guarantee that the buyer will purchase the house at the end of the lease. This could be a major headache for sellers since they’ve already invested time and energy into this agreement.

What is the length of a lease period?

The lease period of a lease purchase agreement is the amount of time you could live in the property before exercising your right to purchase it outright. Generally, a lease period could be anywhere from one to three years.

Key Takeaways

- A lease purchase agreement is a rental contract between a landlord and tenant that allows the latter to rent the property before buying it.

- A lease purchase agreement consists of two contracts. First, the residential lease portion outlines the rights and responsibilities between the landlord and the tenant. Second, the contract for sale portion details the selling price, down payment requirements, and more.

- Lease option agreements give tenants an option — not an obligation — to purchase the property when the lease ends. On the other hand, a leasing purchase agreement is less flexible and could result in financial consequences if the buyer breaches the contract.

Find the right lender to purchase your leased property

A lease purchase contract is similar to leasing a car. You get to “test drive” the property before making a long-term commitment. However, it’s important to remember that a lease purchase agreement differs from a lease option agreement. If you don’t buy the house at the end of the lease period, you’ll suffer significant financial and legal consequences. So, before signing on the dotted line, make sure you’re seriously considering becoming a homeowner.

If you’re ready to start applying for mortgages, check out our list of the top mortgage lenders. Be sure to perform your due diligence and compare each lender thoroughly to find the one that best fits your needs.

Share this post: